Well over half way into 2024, What now?

Well over half way into 2024, What now?

Macro Analysis 30/07

Introduction

Hi friends, welcome to a new macro analysis!

Now that we are well through the halfway point of 2024, we can reflect on financial markets that have been a rollercoaster of volatility. Among the standout performers, the SMH has shone the brightest, leading the pack with impressive gains.

The semiconductor sector SOXX 0.00%↑ has outpaced all other major indices, which may not come as a surprise for a lot of people, given Nvidia's NVDA 0.00%↑ dominance. Interestingly, both $QQQ and $IWM, despite their different focuses, have shown surprisingly similar performance patterns this year.

Now is also a good time to review the latest news that has hit the markets and how it can potentially affect the course of action for the rest of the year.

We will review some of the latest economic data and what they signal about the US economy, highlight economic policy changes overseas in China, and discuss the latest on the crypto markets.

Where Does The Market Stand

Let's take a look back at some key events from the past few weeks. On July 21, 2024, President Joe Biden announced that he wouldn't be running for reelection and endorsed Vice President Kamala Harris as the Democratic candidate.

This decision was influenced by concerns about his age and the political landscape, with increasing pressure from party members and supporters.

While we don't yet know the full extent of the policies Harris might pursue if elected, it's too soon to say how this change will impact the financial markets significantly.

For a snapshot of the market's immediate reaction, we can examine the BTC/USD trading pair, which was tradeable over the weekend following the announcement.

Interestingly, the market didn't show a strong reaction, likely because rumors about Biden's decision had been circulating beforehand, meaning the news was somewhat anticipated and already factored into prices.

You might be wondering why the S&P 500 had a few rough days after a week of relatively stable trading - if not Biden’s announcement, what then?

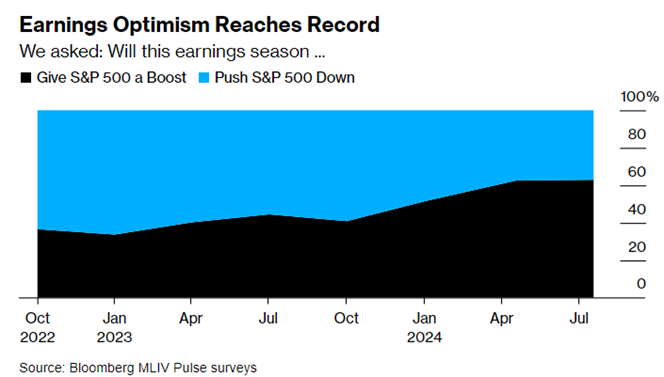

One possible reason, as reported by Bloomberg, is that earnings optimism has been at record highs recently. Many investors have been expecting strong financial results from major companies, which has fueled a lot of positive sentiment in the market.

However, the reality doesn't always match expectations. For instance, recent earnings reports from big names like Tesla and Microsoft didn't meet these high expectations, which contributed to a downturn in the market as investors adjusted their outlook.

For Tesla's TSLA 0.00%↑ Q2 2024 performance, the company reported a revenue of $24.93 B, which marked a 47% year-over-year increase, slightly exceeding the estimated $24.48 B.

However, despite this revenue beat, Tesla's gross profit margins dropped to 18.2%, down from 25% a year prior. This decline was largely due to price cuts across several models to boost sales, which ultimately squeezed profit margins.

Their net income was $2.27B and an EPS of $0.91, above the analyst expectations of $0.82 per share. Concerns about the sustainability of these high-profit margins, especially with the ongoing price reductions, were key issues highlighted by analysts.

Similarly, Microsoft's MSFT 0.00%↑ Q2 2024 results were strong, with the company achieving revenue of $62 B, an 18% increase from the previous year, surpassing the anticipated $61 B.

The net income for the quarter was $21.9 B, resulting in an EPS of $2.93, which also exceeded the consensus estimate of $2.78 per share.

Key contributors to this growth included the Intelligent Cloud segment, which saw a 20% increase in revenue, and the Personal Computing and Productivity and Business Processes segments, which grew by 19% and 13%, respectively.

Despite these robust figures, the market's reaction was mixed, possibly due to broader concerns about the tech sector's growth prospects and valuation.

The market’s reaction to these earnings reports underscores the risks associated with high investor expectations. When companies like Tesla and Microsoft, which are influential market players, report results that do not perfectly align with these high expectations—even if the results are positive—it can lead to significant volatility.

This scenario highlights the dangers of earnings optimism: if companies fail to meet or exceed lofty expectations, it can trigger rapid sell-offs and increased market volatility. Investors should remain cautious and consider the broader market context, particularly during high market valuations.

Additionally, there was noticeable risk-off sentiment in the markets, observable through the AUD/JPY exchange rate. The AUD/JPY rate declined from mid-March to the end of July 2024, with a particularly sharp drop starting in mid-June.

This decline signals a strengthening of the Japanese yen against the Australian dollar, often considered a safe-haven currency. This trend suggests that investors sought stability and reduced exposure to riskier assets, which the Australian dollar often represents due to its ties to global commodities.

If you are unaware, a declining AUD/JPY rate typically indicates a shift towards a risk-off sentiment among investors. The AUD is often linked with riskier assets because Australia's economy is heavily influenced by global commodity prices, which can be quite volatile. In contrast, the JPY is viewed as a safe-haven currency, particularly during times of market stress.

The stability of the DXY during this period suggests that the stability of the US dollar has not been significantly impacted by these shifts. Instead, the changes in AUD and JPY are likely driven by regional or specific economic factors rather than a broad-based move in the US dollar.

This steadiness in the DXY could indicate that the risk-off sentiment isn't primarily driven by concerns specific to the US economy but rather a general risk-off sentiment spreading across markets.

The chart's main point is to highlight a period of increased risk aversion, with investors potentially reacting to global economic concerns or regional uncertainties. This is reflected in their preference for the yen and a move away from riskier currencies like the Australian dollar. Such behavior is consistent with typical market responses during times of heightened economic uncertainty or geopolitical tension.

Lastly, considering the VIX, which is shown in the graph below, there's a noticeably large green candle from Friday, July 19th. This spike likely relates to a significant event, such as the CrowdStrike incident that caused widespread internet disruptions.

However, the more critical observation is the trend forming before this event, where volatility had become quite low, making puts relatively cheap. The subsequent economic data releases, including the advanced GDP measure and PCE numbers, led to an increase in hedging activities, which drove a substantial bid in the VIX, indicating rising market volatility expectations.

Once the GDP and PCE numbers came in, however, the VIX started to get crushed once again. The data came in almost in line with expectations, and therefore, the aforementioned hedges were likely closed. We will discuss the data in more depth in the next section.

This section has highlighted the key events over the past few weeks, as earnings season is underway and people on the street are returning to the offices after a summer break. The next few weeks will be highly interesting as earnings from Amazon (August 1st) and Nvidia (August 28th) are yet to come. Will they disappoint to the extent it sends the whole market down?

Time will tell, but as we see risk measures such as the VIX coming down after recent data and the AUD/JPY pair reaching significant lows, you might wonder if we will have some kind of relief rally in the coming weeks. We advise keeping a close on Amazon, as their earnings will tell us much about consumer sentiment and overall economic activity.

China Cutting Rates

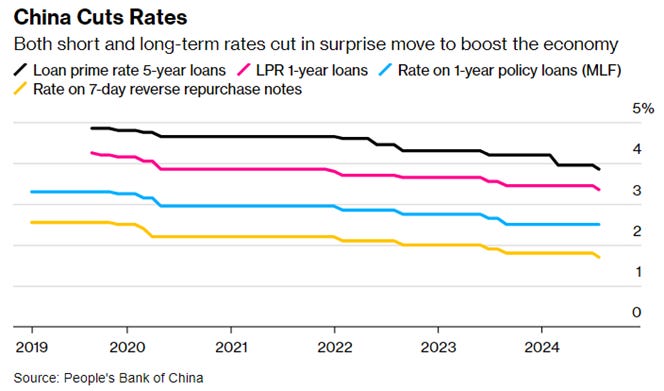

China recently implemented notable interest rate cuts to boost its slowing economy, which has been grappling with various challenges. The People's Bank of China reduced the 1-year loan prime rate from 3.55% to 3.45% while lowering the 5-year loan rate to sub-4%.

This move aims to lower borrowing costs, stimulate a stale economy, and address ongoing issues in the real estate sector, a crucial component of China's economic health.

The reaction in Chinese markets following these rate cuts was mixed. The Shanghai Composite Index showed a slight increase of 0.4%, while the Hong Kong Hang Seng Index fell by 0.3%. This muted response indicates ongoing concerns among investors about the effectiveness of these measures, particularly given broader economic challenges such as the significant debt burdens faced by major property developers like Country Garden.

The real estate sector, a vital driver of China's economy, continues to struggle despite these rate cuts. While lower mortgage rates could theoretically boost housing demand, deeper issues like over-leveraging by developers and weak consumer confidence persist. The recent rate cuts are seen as a part of a targeted strategy to provide support rather than a comprehensive solution to these problems.

For the U.S., a weaker yuan resulting from China's lower interest rates could make Chinese exports more competitive on the global market. This increased competitiveness might pressure U.S. companies, particularly in manufacturing and technology, by affecting their market share and profit margins.

Additionally, the divergence in monetary policies between China and the U.S. could influence global capital flows. As China lowers rates to stimulate growth, the U.S. Federal Reserve remains focused on controlling inflation, potentially leading to higher U.S. interest rates. This could attract more capital to U.S. markets, strengthening the U.S. dollar and impacting exchange rates and trade balances.

Overall, China's economic policies have significant implications for global trade. Lower interest rates might help stabilize China's economy and ensure steady demand for commodities and goods from other countries. However, ongoing issues in the property sector and consumer spending could limit the effectiveness of these measures, contributing to global economic uncertainty.

The contrasting approaches to monetary policy between China and Western economies highlight the different challenges they face. While China focuses on growth, Western countries like the U.S. are dealing with inflationary pressures, potentially leading to varied economic outcomes.

What now?

As this article is already quite long, I’ve decided to split it up into two articles. The second article will be published tomorrow around market open. As such, make sure you are subscribed so you don’t miss out!