Top 3 Bargain Solar Stocks

Top 3 Bargain Solar Stocks

Solar Energy and What To Come

Introduction:

Welcome everyone, I’m pleased to announce the first contributor article from Friso on this substack. I hope you all enjoy it as much, as I enjoyed it.

With that being said, let’s get started!

Why Solar Stocks?

Welcome everyone to my first article on Stock Info’s Substack.

Over the last years, I have been closely following solar stocks and therefore it seemed like a great start to share my three favorite businesses in the industry. All three companies cover different crucial segments in the solar supply chain and have their own competitive advantages.

On the other hand, none of them are direct competitors of each other and could be held in a diversified portfolio to benefit from the solar energy transition.

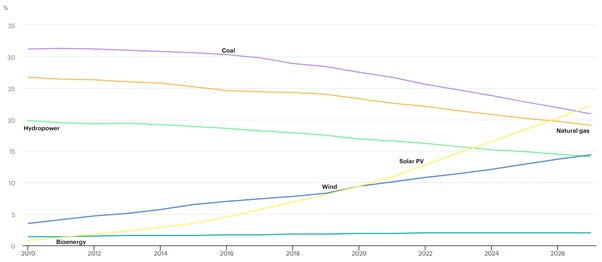

First, you might want to know why the solar industry will be interesting for your personal investment portfolio. Annual solar photovoltaic (PV) capacity additions are expected to increase every year for the next five years according to the IEA or the international energy agency.

Furthermore, the cumulative solar PV capacity should exceed natural gas by 2026 and coal by 2027. Both utility scale solar and retail solar projects are gaining more and more traction due to lower solar module prices and higher energy prices. Solar energy is becoming the cheapest energy source and will increasingly benefit homeowners with electrical vehicles becoming the standard in the next decade.

Enphase (ENPH)

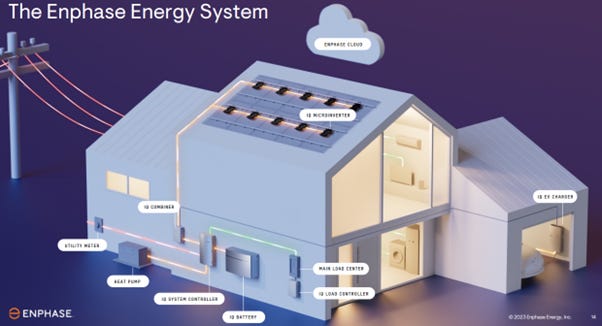

Jumping right into the first business, Enphase Energy is a global energy technology company that designs, develops, manufactures, and sells microinverter-based solar-plus-storage systems.

Inverters are needed to convert energy of the solar module from DC (direct current) to AC (alternating current), so that you can use the energy inside your home. There are two popular types of inverters on the market: string inverters or microinverters. String inverters connect all solar panels together.

While Enphase's semiconductor-based microinverter system converts energy at the individual solar module level, which provides several advantages over traditional solar panel systems, including:

Increased energy production: Microinverters track the output of each solar module individually, which can lead to up to 25% more energy production than traditional solar panel systems.

Improved reliability: Microinverters are less vulnerable to shading, rain or snow than traditional solar panel systems, which can lead to higher reliability and uptime. Each microinverter is isolated from the others, so if one fails, it does not affect the rest of the system. String inverters maximum output is that of the lowest generating solar panel. If the solar system is facing multiple angles on the roof, like south and west, then microinverters are the way to go.

Enhanced monitoring and control: Enphase's microinverters come with a built-in monitoring system that allows homeowners to track their energy production and usage in real time.

Lifespan: Another important aspect of microinverters is the 25-year long warranties, built to last as long as the solar panels, while string inverters tend to have lower warranties of 8 to 12 years.

Back-up power: Enphase's IQ8 microinverter is the world's first grid-forming microinverter, capable of providing backup power without a battery by forming a microgrid during a power outage relying solely on sunlight.

The initial costs of a microinverter system will be higher than that of string inverters, but after 25 years microinverters should have shown their true value to customers.

Further, Enphase is about to launch a new microinverter product. The IQ8P is targeted at a small commercial market in North America and Europe, and emerging residential markets (Brazil, Mexico, India, etc.). The new product should support panels up to 650-watt DC, more than enough to provide full energy from the latest Tiger Neo solar panel of JinkoSolar, with power output estimated at 635W.

In addition to its microinverter systems, Enphase also offers a variety of solar-plus-storage products, including batteries, energy management software, and EV charging systems. These products allow homeowners to store excess solar energy for use at night or during power outages, to better manage their energy consumption and charge their electrical vehicles.

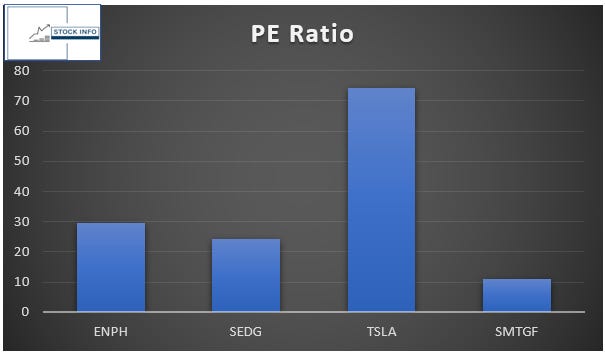

The company's main competitors are SolarEdge Technologies (SEDG), SMA Solar Technology (OTCPK:SMTGF), Tesla (TSLA) and Fronius International.

Enphase uses a business model that has a low amount of capital expenditures, because they do not use large factories to manufacture inverters. As a result, the company benefits from gross margin that are exceeding competitors.

More and more free cash flow is leftover, which can be reinvested in R&D, fund the business in a sustainable way without dilution and ultimately be used to repurchase shares outstanding at attractive prices to reward shareholders.

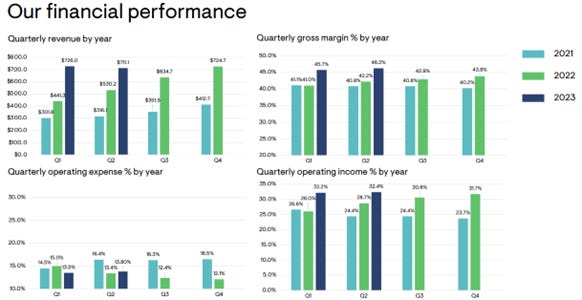

In two years, Enphase saw its revenue increase rapidly from quarterly $300 million to $700 million. However, the last quarter changed investor sentiment due to a quarter-over-quarter revenue decrease for the first time in years. Yet, investors forget how great of a quarter the first one was. Revenue grew 64% year-over-year, which easily outpaced the year before. In the second quarter, Enphase was still able to grow revenue 34%.

This is remarkable because higher interest rates have been tempering the demand for solar projects in America. Each rate hike makes it more expensive to loan money, which creates a slowdown in long term investments, like placing solar panels and batteries. Moreover, the largest solar market state in America, California, is making changes to their net metering program.

Under NEM 3.0, the value of solar energy credits decreased by 75% for new California solar customers. Therefore, it has an impact on the payback time of the solar system, lowering the incentive to place a new solar installation. Surprisingly, in the high inflationary environment Enphase was not only able to cut costs, but even increase prices of their innovative products. Despite the decrease of revenue from Q1 to Q2, gross margin and operating income increased, which showcases Enphase price power.

The third quarter is expected to be the weakest point of 2023, as inventory levels are getting a correction. Nonetheless, this should be a temporary miss in the growth trend and with new product launches globally, Enphase has more than enough growth opportunities left in Europe and emerging markets.

Investors can take advantage of the overreaction of the market, since the valuation of the business has become a lot more attractive.

Valuation

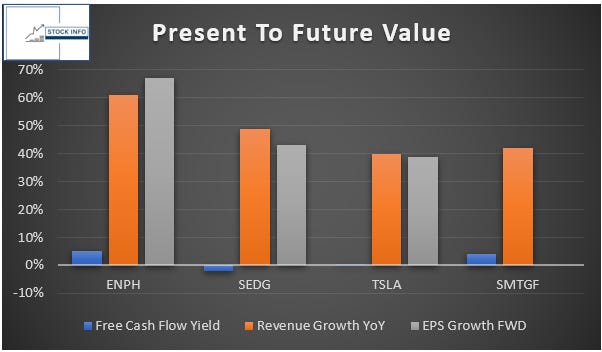

Historically, Enphase is currently trading at the lowest price-to-earnings ratio since the COVID-19 pandemic. Based solely on the PE ratio it will be hard to see which one is cheaper than the other, considering all four companies are still focusing on being more efficient and increasing earnings at a fast pace.

Therefore, I have listed some facts of the present and some estimates for the future. Enphase did grow the fastest year-over-year of all three competitors. In addition, Enphase is the most attractive right now when it comes to free cash flow yield.

Free cash flow yield for the company sits at a decent 5%. In the following year, Enphase is also expected to grow their GAAP earnings per share the most by 67%, outperforming the others.

Enphase has built up a strong balance sheet with a current ratio of around 3.4x. As a result, the management can start doing share buybacks to stop the dilution of the shareholders. In the second quarter, Enphase bought back 1.25 million shares at an average price of $159.43 for a total of $200 million. A new $1 billion buyback program was announced as well, which shows the confidence of management in future growth and commitment towards shareholders.

Lastly, Director Thurman J. Rodgers bought 32,600 shares of the company’s stock in a transaction on September 14th. The stock was purchased at an average cost of $122.76 per share, for a total transaction of $4,001,976.

Two more in-depth articles on Enphase: Stock Info’s and Friso’s Article

JinkoSolar (JKS)

JinkoSolar is a leading global solar module manufacturer and renewable energy solutions provider. Established in 2006, the company has emerged as one of the largest and most innovative players in the solar industry. With a strong focus on research and development, JinkoSolar has achieved significant technological advancements and a solid reputation for delivering high-quality solar products.

JinkoSolar operates a vertically integrated business model, encompassing the entire solar value chain (excluding polysilicon). The company designs, manufactures, and sells a range of solar PV modules, as well as other solar energy products and services. Wafers and solar cells that are not used in the solar module production are sold to peers in the industry.

The company has established a robust global presence, with a wide distribution network. Further, it has strategically positioned regional offices, warehouses, and subsidiaries in key solar markets worldwide, enabling it to effectively serve its customers.

JinkoSolar has achieved several milestones in solar module efficiency, including record-breaking conversion efficiencies for its products. By continuously investing in R&D, the company aims to stay at the forefront of technological advancements, improve energy generation efficiency, and drive down the levelized cost of energy for solar power.

Technology & Important Metrics

There are different solar module technologies out there that have several advantages or disadvantages. Mono PERC is currently the most used solar panel, but the technology has reached its limits in energy efficiency progress. At the moment, N-Type TopCon technology is rapidly taking over market share and is estimated to be 62% of the overall market by 2026.

N-Type TopCon has much higher energy efficiency and is known for its relatively low costs to produce. There are two other upcoming technologies HJT and xBC, which are more complex to manufacturer and therefore have a higher cost. HJT has great efficiency and can hit very high bifacial rates, but it struggles with the power output of the panels.

The xBC technology is used by Aiko Energy, those panels have high efficiency and power output. However, they are new to the market and expensive to build.

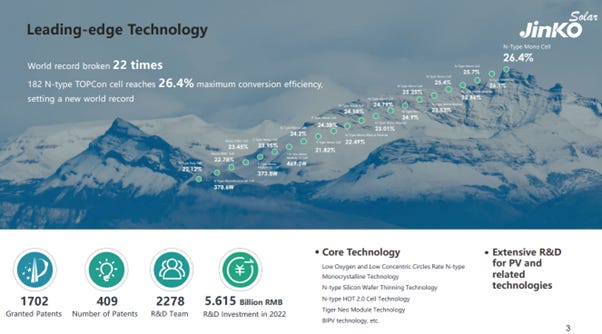

JinkoSolar is the industry leader in manufacturing N-Type TopCon solar modules. The company has broken the world record 22 times regarding the efficiency of the panels, which is now standing at 26.4%. The average mass-production cell efficiency is standing at 25.8%.

Next to efficiency, JinkoSolar’s panels have the benefit of producing enormous power up to 635W for the Tiger Neo module. The Tiger Neo is the best of his class, outperforming the panels of Sunpower, Maxeon, Longi, Trina Solar. Only the xBC panels of Aiko match the efficiency of the N-Type TopCon panels, yet JinkoSolar still tops the power output.

Canadian Solar’s latest TOPBiHiKu7 Bifacial is another high performing panel that tops Jinko’s power output by 45-65W due to exceptional bifaciality (85% compared to Jinko’s 80%) and barely lower efficiency.

All around, JinkoSolar’s innovation has a strong proven record.

Operational Improvements

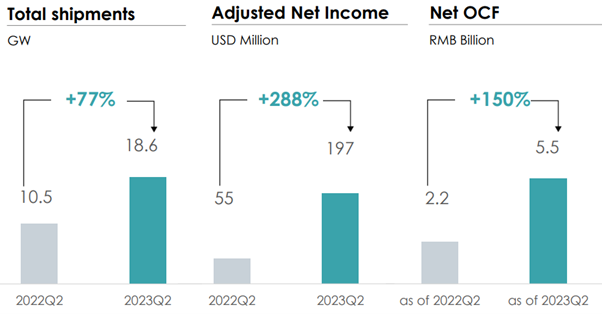

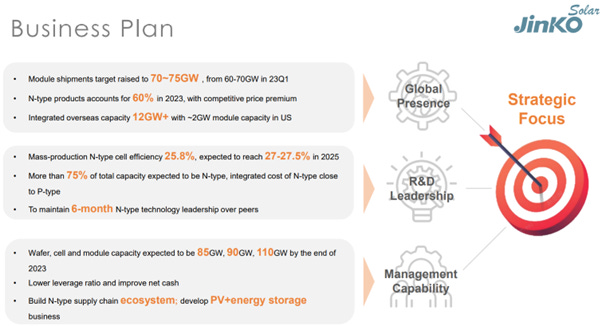

JinkoSolar reached a new stage in their business development. After years of capital expenditures, they have built worlds largest overseas integrated capacity of more than 12GW with manufacturing in Vietnam, Malaysia, and the US. The total annual N-Type cell capacity is expected to reach more than 70 GW by the end of 2023. The company is growing extremely fast with shipments up more than 77% and adjusted net income up more than 288%, demonstrating the company’s focus on efficiency.

While solar module prices have been declining, JinkoSolar has benefited from an even sharper decline in polysilicon prices (material needed to make wafers).

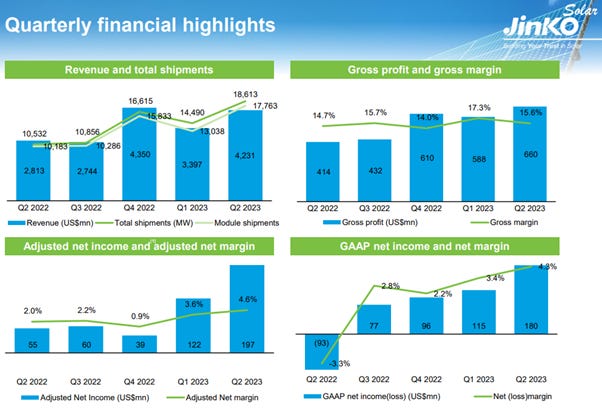

GAAP net income grew from -3.3% to 4.3% in the second quarter of 2023. Throughout the year, the company was also one of the only solar panel makers that increased guidance for 2023.

Valuation

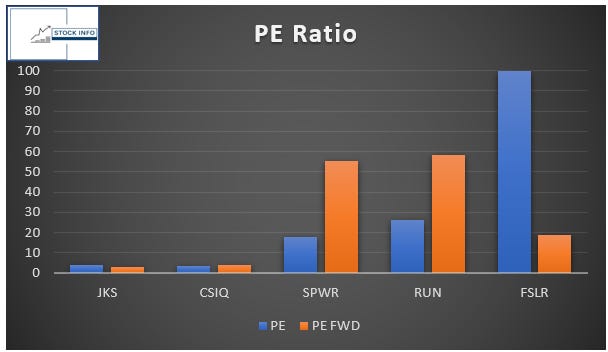

When comparing JinkoSolar to competitors based on price-to-earnings ratio, we can see two clear winners. Both JinkoSolar and Canadian Solar trading at incredibly low pe ratio’s below 5x. You might think that JKS and CSIQ would be growing at a slower pace compared to the other three more expensive companies, but this is surprisingly not the case. JKS and CSIQ are respectively expected to grow 40% and 24% next year, while the others barely reach 17% forward revenue growth.

JinkoSolar balance sheet is not the best I have seen. The current ratio is above 1, so they have enough liquidity to pay short-term bills. But as you can see the best times of profitability are yet to come.

Net income is raising and cash flow generation should improve in the coming years. In the business plan, the management mentioned that a lower leverage ratio and improvement in the net cash position are primary focusses.

JinkoSolar and Canadian Solar have proven their capabilities in building a fully integrated business model and serving the needs in the renewable energy space. Both businesses are poised to get more profitable over the coming quarters, which could boost the momentum in a positive direction for solar stocks.

Next to margins, demand for solar modules is still high and is growing year over year. I favor JinkoSolar more in the solar module space for two important reasons.

Jinko was able to avoid U.S. tariffs on import solar panels, while Canadian Solar did not yet find a loop around that.

Secondly, Jinko announced a $1.50 per share dividend, good for a 5% dividend yield. And is looking to buy back more shares, which indicates to me a stronger price recovery going forward.

Daqo New Energy (DQ)

The last solar company I want to discuss is Daqo New Energy. Daqo New Energy is a high-purity polysilicon manufacturer based in China. The company makes use of a chemical vapor deposition process (CVD) combined with upgraded hydrochlorination technology.

Hydrochlorination technology is an advanced solution, which minimizes the complexity of construction management and usage of resources. Daqo has designed an extremely efficient rate between the amount of polysilicon obtained and the production costs.

The photovoltaic supply chain can easily be visualized by the image below. The segment that has a shortage or the lowest production capacity is most of the time the highest margin business.

Over the last years, there was a polysilicon shortage causing prices of polysilicon to rapidly increase. As a result, the margins of the downstream supply chain were thin, since the costs were high and got pushed from segment to segment.

Luckily, solar panel makers saw soaring demand due to the energy crisis and could shove additional costs to the customer. Daqo was able to make a windfall, because of high polysilicon prices and reinvested the money into manufacturing expansion.

One of the competitive advantages Daqo New Energy has, is the extremely low cash cost to produce polysilicon. Now that polysilicon prices have fallen to $10-12/kg, the business is still cash flow positive and has an EBITDA margin of 36%. Further, the average selling price gap between low quality (P-Type) and high-quality (N-Type) polysilicon has been growing.

This is a positive factor for Daqo with the new factory in Baotou city coming online, which mainly produces high-quality N-type polysilicon.

Next to polysilicon for solar, Daqo New Energy will start exploring polysilicon manufacturing for the semiconductor industry, which demands higher-purity polysilicon, and this could be a higher margin business in the future.

Polysilicon prices have dropped for a combination of reasons. The first reason is the capacity expansion of multiple polysilicon manufacturers, that has created more supply than demand. Further, wafer manufacturers had an inventory glut of polysilicon, due to the limited supply of high-purity quartz, leading to even less demand.

Lastly, Daqo New Energy mentioned in the latest earnings call that they would decrease their stacked inventory, what flooded the market and influenced the prices.

However, wafer expansion is not going to stand still at all with the demand for solar panels. JinkoSolar is building a gigantic 56GW wafer-cell-module integrated manufacturing facility in Shanxi, China.

On the other hand, three Chinese polysilicon manufacturers with high production costs have already suspended operation due to losses, and even leading suppliers are said to have stopped shipments.

Valuation

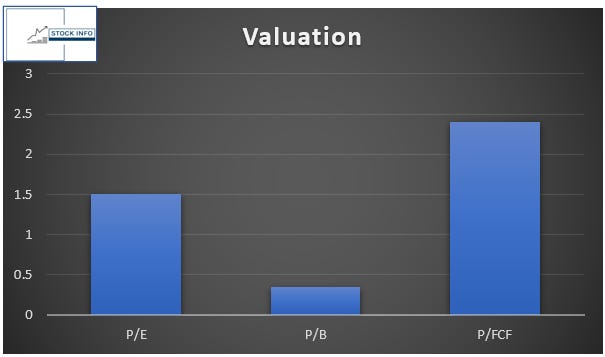

At the current prices, Daqo New Energy is trading at absurd discounts. The stock has a price-to-earnings ratio of 1.5x, price-to-book of 0.35x and price-to-free cash flow of 2.4x. Further, the free cash flow yield for the stock is 42% and has a book value of $63 per share ($27 stock price).

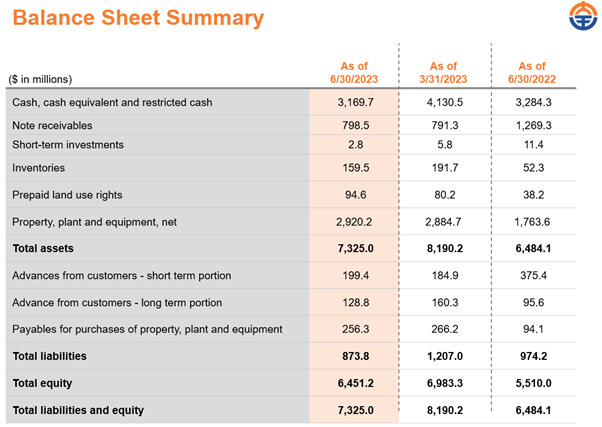

Daqo New Energy has a valuation of $2 billion at the time of writing. Surprisingly, the company has more than $3.1 billion in cash and $800 million in note receivables which cover the total debt of the company.

Funny enough, most of the company’s liabilities are advances from customers, which will convert into revenue as soon as the products are delivered to the customer.

Obviously, the management team knows better than anyone how inexpensive the shares are trading at.

Therefore, a $700 million buyback program has been approved and has almost been completed. The share buyback should decrease the share outstanding and create upward pressure on the stock.

While the $700 million buyback is a great start, more will be needed to correct the stock from the absurd valuation it is currently in.

Takeaway

The energy transition to renewables is not slowing down at all. The international energy agency goes as far as calling out that annual solar PV capacity additions will increase every year for the next five years.

The solar sector has turned into one of the most disliked areas in the stock market. The opportunities to benefit from the renewable energy transition, by buying the most profitable and high-quality businesses, are growing every day.

Enphase, JinkoSolar and Daqo New Energy are my top-picks for the coming years, as they are well-positioned industry leaders in their own part of the solar supply chain. Without a doubt volatility will be high in the coming weeks, but no-one can deny the long-term trend.

Nevertheless, investors need to keep in mind that JinkoSolar, Daqo New Energy and Canadian Solar has been identified by the SEC under the Holding Foreign Companies Accountable Act.

This means the companies will be delisted by 2024, if they do not show the right auditing under the rules of the United States. All three companies are confident that the latest annual report followed the rules and that they should not be delisted.

Thank you for reading. If you have any questions, do not hesitate to reach out in the comment section below or hit us up on X.

Addition from Brent:

I hope you enjoyed this first contributor article and we would very much appreciate your support by liking and sharing this article. If you want to read more of our work, make sure to subscribe for free by clicking the link below!

Disclosure: I/we have a stock, option or similar derivative position in some of the companies mentioned, and might add to our positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

keep it rocking, interesting thematic, cheers!