Starbucks a good buying opportunity or a struggling business?

"In The Spotlight" Starbucks

In our first “In the Spotlight” we will be analyzing Starbucks Corporation (SBUX).

Intro

Starbucks is a company that has gained some attention by value investors. We take a look at “why” this is the case.

SBUX is facing headwinds such as inflation and protectionism politics.

How will the possible sale of the UK stores affect Starbucks?

SBUX has a strong brand name and competitive business model.

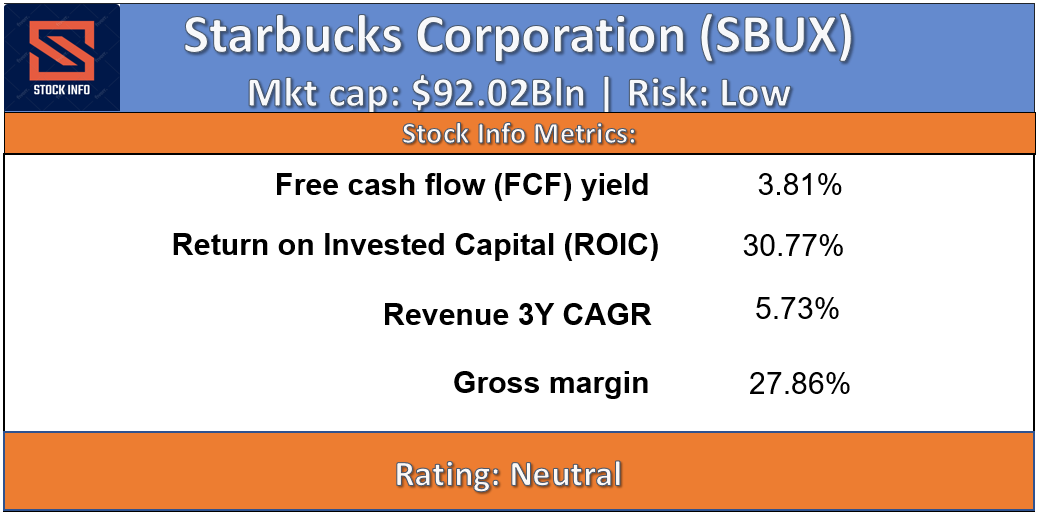

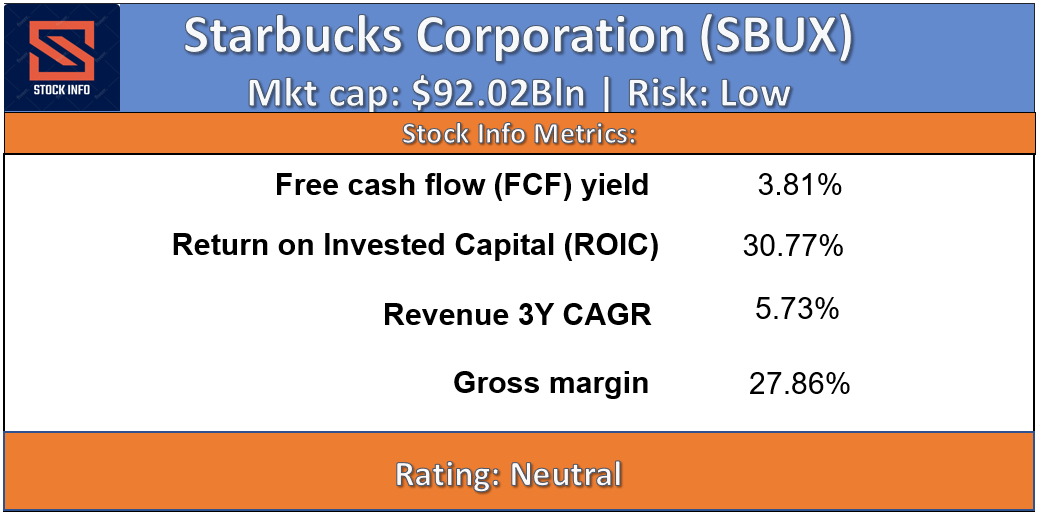

The Numbers

SBUX has a normal FCF of 3.81%, which indicates that the company could buy itself back in 26 years.

SBUX has a weak revenue 3-year annual growth rate of 5.73%, this shows SBUX is becoming a mature business, which indicates that Starbucks is struggling to continue hyper growth.

SBUX has a strong ROIC of 30.77%, indicating that each $100 invested in the business results in an additional $30.77 of operating income. This proves that SBUX has a nice moat and doesn’t need much money to run its business.

SBUX has a mediocre gross margin of 27.86%, indicating that it has strong pricing power.

Forward PE: At the current valuation Starbucks has a forward PE of 28.05. This is pretty similar to competitors. Macdonald’s has a forward PE of 25.56, which is slightly lower. Compared to their closest competitor in the US they are looking fairly good. Dutch Bros (BROS), which currently has a forward PE of a staggering 174.67.

When we take this into consideration, we can clearly see that SBUX has a fairly low FCF. We prefer companies which have a higher FCF and have a little more growth potential. Furthermore, SBUX has a strong ROIC and is starting to become at an attractive valuation although we would like to see the FWD PE in the low 20’s.

Headwinds

Recession will crush consumer spending. One of the biggest fears for SBUX shareholders should be a recession. At the moment we are in a period with rampant inflation. As families are starting to struggle due to significant price increases across the board, mostly in food and energy prices, people might decide to cut out there Starbucks coffee and go for cheaper alternatives. A recession would thus be detrimental to SBUX as their products are considered as a luxury product to most consumers.

In addition to the above, Starbucks is a consumer discretionary company, which historically get hit quite significantly in an economic downturn. The reasoning behind this is pretty simple. For Starbucks by example. If u need to cut spending, where would u cut first? Of course, for a lot of people this would be there daily Starbucks trip or at least go less often than before.

Law of large numbers. Starbucks is the largest coffee house chain in the world. Due to this, Starbucks is starting to struggle as they can no longer maintain this fast-paced expansion, which causes them to see a slow in growth. We believe the growth rate percentage of Starbucks will decrease in the upcoming years. In addition, we believe they might go further with closing stores as they will struggle due to inflation and other issues.

Inflation. Inflation also has an impact on SBUX itself. due to an increase in product cost, Starbucks will suffer from decreasing margins as they won’t be able to increase the price of their products much further as they are already quite expensive.

Increasing competition. Starbucks is struggling due to increasing competition all over the world. They are losing ground in China as Luckin Coffee Inc. (LKNCY) remains dominant. Additionally, the political tension between China and the US are on the rise again, which could harm SBUX in the future. Furthermore, we have the increasing competition in the UK, which is the biggest market for SBUX in the Europe. In addition, the UK has a growing number of independent operators, as well as Costa coffee (which is owned by The Coca-Cola Company).

Unionization is an issue that got a lot of media attention over the past month and is starting to become a serious issue for SBUX. Hourly wages have now been increased to $17 an hour, which will increase expenses. Furthermore, SBUX has decided to suspend their share buyback program as they want to invest more into staff and cafes among other things.

Strengths

Brand name. Starbucks has become a house hold name. Everyone knows Starbucks and a lot of people swear by it. A lot of people have made a habit of getting a Starbucks to start the day. Furthermore, Starbucks has become kind of a status symbol similar to Apple’s iPhone.

Loyal customers. Starbucks has very loyal customers, due to the reasons already listed above. In the wake of this, it could very well be that SBUX will suffer less than the average consumer discretionary company as it already is a luxury brand. A Starbucks coffee is now seen as an affordable luxury, which wasn’t really the case in 2008, which could also add strength in an economic downturn. Although, this might be the case, we believe rampant inflation in addition to decreasing consumer spending will affect SBUX’s business quite significantly so we aren’t convinced this is a valid reason as of now.

Cheap, if we would only take PE into consideration Starbucks is trading at historically low valuations. Starbucks has a PE of 22 at the moment of writing, which definitely is not bad. We do expect earnings to decrease in the upcoming quarters, which would result in a lower “E” in the PE ratio.

Dividend, Starbucks gives a nice dividend, which is definitely a big plus for the longterm investors who love to see their portfolio having some cashflow. As of now the payout ratio is 57.83%, which is quite high already, but it does leave room for further expansion in the future.

Insider Buying

Howard Schultz, the current CEO of Starbucks corporation has a good track record within the company. He has served as a CEO from 1986 until 2000. He served as CEO again from 2008 until 2017. In April of this year Mr. Schultz rejoined once again to get the company back on the right path as an interim CEO.

Starbucks Corporation hasn’t had much significant insider buying lately. Nevertheless, Mr. Schultz has been buying shares in the recent dips, as can be seen in the table below.

Mr. Schultz as of recent data, owns around 21,795,538 shares of SBUX. This is a big amount, which we like to see with insiders. This indicates the CEO has a serious incentive to provide share appreciation as this would benefit himself. There weren’t any insider purchases since 2018. Thus, it is quite encouraging to see Mr. Schultz has bought shares in the recent dip. Although, the value purchased isn’t as significant for Mr. Schultz, we believe this is a good indication that the CEO believes the stock is currently undervalued.

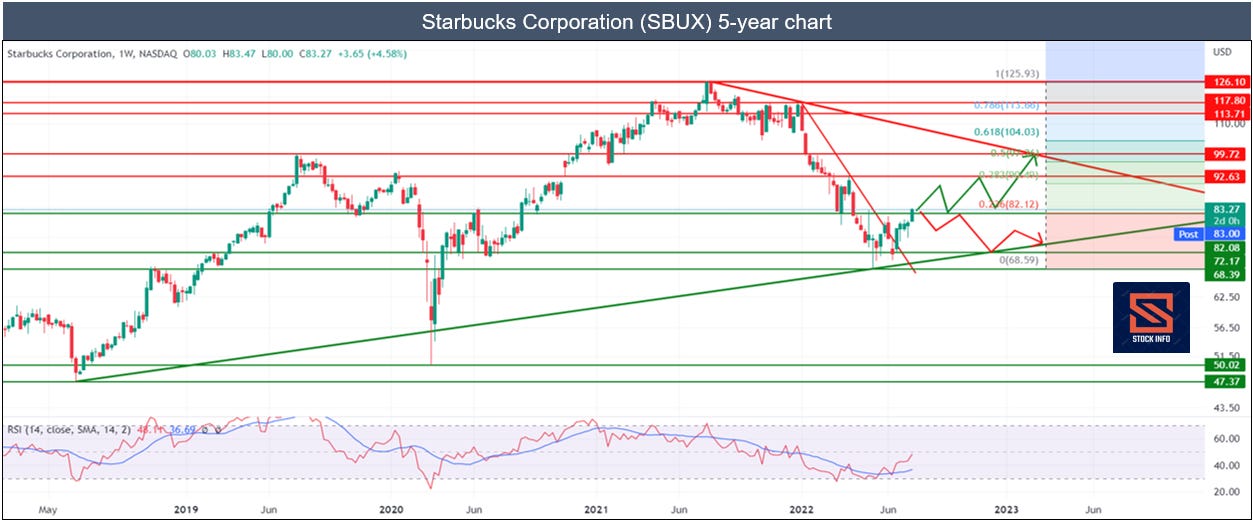

The Charts

As can be seen on the chart below Starbucks touched its trendline support (which is intact since the covid crash from March 2020). This can be seen as a very significant support, which as of now seems pretty buyable. The stock isn’t out of the woods yet, but the chart seems pretty promising as we made a higher high and we broke above the resistance at $82.08, which now acts as support. Upcoming resistance lays around $90.45 and $92.63. Immediate support is $82.08 right now. For the long-term support I would be looking at low $70’s and preferably on the green trendline support. Important to keep in mind that the RSI is getting quite high right now, it would be good for this to cool down a bit. This would be healthy for the bullish trend to continue.

Now let’s have a look at the long-term chart. The green and red arrows are the possibilities right now. We spoke about the supports and resistances above. Right now, the green arrow looks more likely, but the macro environment is so uncertain that this very much looks like a bear market rally. Furthermore, for a long-term position we would only be interested in buying at the green trendline support or if SBUX continues to show significant strength in the upcoming weeks and months. Before we can start looking at the all-time high (ATH) again, SBUX has to break above the red trendline resistance.

Conclusion

We believe SBUX is a solid business that suffers from high inflation and other headwinds. The increase in competitors is a problem, but we believe Starbucks is a very solid brand with a loyal following. Furthermore, Starbucks might suffer in the short term, but if you have a time horizon of 10+ years SBUX is a stock that could fit in your portfolio. An important thing to keep an eye on in our opinion is the growth rate. We don’t necessarily like the possible sale of the UK stores as this could show that SBUX might change strategy and will try to maintain market share rather than grow and become even more dominant.

Thanks for reading our first In the Spotlight! I hope you enjoyed it.

Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.