QUBT High on Hype - Too Many Red Flags

Quantum Computing Inc. (QUBT) Has nothing to show for

Introduction and TLDR

Dear reader,

I hope you had a beautiful Christmas. After the festivities it might be a good time to prepare your portfolio for 2025 and look for potential new ideas. Here is one of these ideas, which could be a great addition to your portfolio at the right time.

Quantum Computing Inc. (QUBT) has generated plenty of buzz lately— touting a small NASA contract and claims of an in-house foundry for “TFLN” (thin-film lithium niobate) photonic chips. While quantum computing is very much here to stay, we don’t believe QUBT is the right long-term play here at this moment in time as the company has some serious red flags.

TFLN Chip Foundry Doubts: Independent checks suggest QUBT’s stated manufacturing facility can’t possibly be fit for large-scale chip production. As a matter of fact, it is likely an office building.

Minimal Revenues: Despite sporting a market capitalization exceeding $2 billion, QUBT’s sales remain under half a million dollars annually.

Repeated Pivots: The company has jumped from beverages to quantum software, and from AI to chips, without building a solid track record of sustained commercial success. Focusing on the latest hype to get some momentum in the stock. There have been numerous firms that have mentioned this weird behavior of QUBT’s management. A notable piece worth reading can be found here.

High Share Dilution: Frequent capital raises are diluting existing shareholders, amplifying downside risk.

Given the mismatch between QUBT’s market valuation and its fundamentals, a careful, bearish approach seems warranted—at least until the company demonstrates tangible operational progress.

What Are TFLN Chips (and Why They Matter)?

“TFLN” stands for thin-film lithium niobate—a material known for its ability to handle and manipulate light (photons) rather than electrical signals. Traditional computer chips use electricity running through silicon. In contrast, TFLN chips aim to leverage light’s properties to achieve benefits such as:

Higher Bandwidth: Potentially faster data throughput.

Lower Power Consumption: Photonic circuits can be more efficient than purely electrical ones.

Enhanced Quantum Applications: Photons can serve as a platform for quantum data exchange, which might complement certain quantum computing tasks.

While TFLN is a promising material, mass production of such advanced chips typically requires a specialized facility with sophisticated cleanroom environments, heavy machinery, strict contamination controls, and robust funding.

This is where Quantum Computing Inc. claims to hold a potential “first-mover advantage,” yet on-the-ground reports raise questions about whether the company’s site in Tempe, Arizona, truly meets the requirements of a serious chip foundry. Research from Iceberg Research shows that the foundry location is questionable to say the least.

Questioning the Arizona “Foundry”

Quantum Computing Inc. has frequently highlighted its plan to roll out a dedicated TFLN production facility. However, several issues cast doubt on the feasibility and timing:

Basic Office Space: Investigations of the listed address reveal what appears to be an ordinary commercial office suite, lacking the industrial infrastructure (docks, specialized ventilation) typically seen in chip manufacturing.

Limited Capital Outlays: The company’s financial statements do not reflect the level of spending one would expect when outfitting a state-of-the-art photonic chip factory.

Aggressive Timelines: QUBT’s claim that production is just around the corner (within a quarter or two) seems overly ambitious if the necessary equipment and processes are not already installed.

In sum, the “foundry” may be more aspirational than operational—a concern for anyone banking on QUBT’s near-term manufacturing milestones.

The NASA Contract: Too Small to Matter?

A well-publicized NASA contract brought QUBT extra attention, yet public data show that this deal is valued at roughly $26,000—hardly transformative for a company that has, been valued at billions of dollars by the market. Although partnering with NASA sounds prestigious, this figure suggests the arrangement is more of a small-scale test or exploratory engagement rather than a lucrative revenue generator. In addition, they conveniently didn’t mention the value of the contract in their press release.

When a heavily promoted contract boils down to such a small sum, it raises a broader question: Are other QUBT announcements similarly inflated in importance?

A History of Dramatic Pivots

Beverage Beginnings: QUBT’s corporate predecessor once operated in a completely different sector, manufacturing beverages.

Quantum Software & AI: The company eventually rebranded as a quantum software venture, then hinted at AI-focused acquisitions—announcements that did not lead to visible, large-scale commercial success.

Now TFLN Chips: More recently, management seized on the semiconductor rally—fueled by big names like Nvidia—and positioned itself as an emerging optical chip manufacturer.

When a business doesn’t seem to work pivoting to adapt to new opportunities can be smart, but normally this is already a red flag. However, frequent shifts without follow-through or substantial revenue may indicate a company reliant on buzzwords rather than a proven business model, which might be the case here. It is no surprise that they move to a sector with a lot of hype each time. This feels a bit like the companies who all of the sudden became NFT companies back in 2021.

Dilution, Valuation, and Management

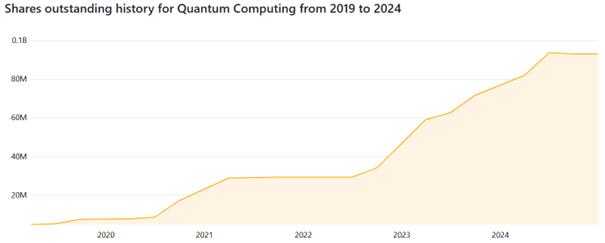

Frequent Capital Raises: QUBT’s burn rate has led to regular share issuances, diluting shareholders over time. As a smaller technology venture with modest revenue, QUBT faces the risk of further funding rounds if its projects take longer to mature—or fail to do so entirely. As can be seen in the chart below, QUBT’s shares outstanding have increased by 20x since 2019.

Companiesmarketcap.com

Lofty Valuation Multiples: Even after some price volatility, the stock has traded at price-to-sales ratios well over 1,000x, which comes as no surprise as the company barely has any revenue, let alone free cash flow.

Management Priorities: While raising capital is normal for early-stage tech firms, we wonder whether management’s main objective is to finance generous salaries or to deliver a long-term, revenue-generating product and creating shareholder value.

Technical Analysis

There could be another significant upward move before the stock comes down. That’s why when you short a stock in a hyped sector with a lot of momentum it is important to wait for a clear turnaround. In this case, something we would call a parabolic short. While we discussed parabolic shorts earlier and there are multiple ways to play this. Qullamagie’s description is one of the best.

For now, the stock’s momentum continues to be strong and I would rather be long than short this stock at this moment in time. The stock was up over 7,500% in less than 6 months following its bottom in the beginning of July at $0.355, reaching a high of $27.15 earlier this month.

QUBT has been perfectly following its 10 and 20D EMA’s, which have acted as strong support levels each time. These can be considered “buy the dip” opportunities for now. A breakout above its recent all-time high (ATH) at $27.15 could fuel another strong rally.

As such, a parabolic short could become viable if the stock deviates significantly from its 10D EMA, (100%+ above its 10D for example) and a strong red candle following afterward. Or for a higher conviction short, you could wait for the stock to lose its dominant moving average in this case the 20D EMA. The first support will more than likely be the 50D EMA in that case, which is over 45% lower.

Positioning: A Waiting Game—or a Hedged Short

For Optimal Risk/Reward there are a few considerations to be made:

Long-Term Investors: If you believe in quantum computing’s future but doubt QUBT’s ability to execute, it may be prudent to wait for legitimate operational milestones—like evidence of a functioning TFLN foundry or a notable jump in revenue—before risking capital. In addition, there are plenty of interesting competitors, which we believe are a better bet at this moment in time.

Short Strategy with a Twist: For those considering a bearish stance, a put debit spread can limit the cost of short exposure. Meanwhile, adding a far out-of-the-money (OTM) call option can act as a hedge in case sentiment swings wildly and triggers another hype-driven surge. Nevertheless, I would simply wait for the stock to clearly lose momentum before trying to short this thing. As such, I currently don’t have short exposure to this stock, but it is one that is high on my watchlist for the upcoming weeks and months.

Using the options combo allows you to hedge against a “crash up” scenario. In this case, you are protected against a sudden “meme stock” surge. But, as with any options strategy where you are paying a debit, it is crucial to not pay too much as this can kill the profitability. Shorting stock while selling puts as a collateral could be a good way as well to collect some premium while you wait for the stock to eventually collapse.

Potential Alternatives in Quantum Computing

While there currently is a lot of hype in the sector and a lot of these stocks having crazy valuations and not a lot of revenue to show for it. There are some potential alternatives you can play for Quantum exposure. Especially for the momentum traders it probably doesn’t come as a surprise as these stocks have been on your radar over the last weeks.

Let’s take a look at the alternatives:

IonQ (IONQ): IonQ focuses on trapped-ion quantum computers and provides access to its systems through leading cloud providers. With strong institutional backing—Amazon and Lockheed Martin among them—IonQ shows higher revenue growth, a substantial cash balance, and a clear roadmap (including its anticipated “Tempo” system) that could deliver early commercial quantum advantages.

IonQ with Amazon Defiance Quantum ETF (QTUM): For those who prefer a more diversified approach, this ETF invests in a basket of quantum-computing and AI-related companies (including IonQ, Rigetti, and others). It spreads out risk across multiple players rather than betting on a single stock. While some holdings may deviate from pure quantum plays, it can offer broad exposure to the evolving sector.

If you go through the ETF’s holdings we can’t find QUBT in there, coincidence?

D-Wave Quantum (QBTS): Though still unprofitable and navigating significant R&D challenges, D-Wave has carved out a niche with its quantum annealers and has begun expanding into gate-model systems. It is an admittedly higher-risk pick, but some investors may still find it more focused on real quantum solutions than QUBT.

Rigetti Computing (RGTI) is another notable quantum player with its own chip-fabrication facility and a “full-stack” strategy that encompasses hardware sales, cloud services, and quantum software. The company has recently garnered attention thanks to a breakthrough in AI-assisted quantum calibration, as well as some government contracts.

Despite these positives, Rigetti’s financials are still weak, with limited revenues, heavy R&D spending, and a strong likelihood of further share dilution over the next few years. While its vertical integration could position Rigetti for future success—especially if it can solve the scaling issues that plague quantum computing—investors must be comfortable with the substantial risk and multi-year timeframe before the technology matures and drives meaningful profitability.Google (Alphabet): A major tech player with deep pockets, Google’s Quantum AI division recently unveiled its “Willow” chip, claiming performance leaps previously considered impossible. While Google’s quantum efforts are only part of its vast operations, the company has the financial strength to persevere through the long, expensive R&D cycles that quantum computing demands.

While all of these niche quantum computing stocks still have a lot of work to do, they have a lot less red flags compared to QUBT at this time. Quantum Computing is one of these sectors that have received a lot of hype over the years (similar to AI), the stocks have now finally gained some momentum. Especially for the traders, these have been must-own setups.

Conclusion: High on Hype, Low on Proof

The promise of quantum computing is real, and TFLN technology may indeed have a place in future photon-based data transmission or computation, for the tech experts reading this, feel free to add some feedback on the tech itself.

But, Quantum Computing Inc. has yet to demonstrate the operational scale, revenue growth, or stable corporate strategy to match its lofty claims. Between:

A small NASA deal ($26,000), which isn’t meaningful at all. Nonetheless, the company used this to get itself in the spotlight.

A “foundry” that might be mostly office space,

A track record of pivoting to trendy sectors without significant commercial traction,

And constant share dilution

The burden of proof lies heavily on QUBT to show that its ambition can translate into verifiable, growing revenue. Until that happens, the downside risks appear significant relative to any potential rewards.

We believe it is important to remain cautious. In the short term, the stock is attractive for traders (both on the long and short side), but in the medium to long term, QUBT must prove it can deliver real, sustained value rather than just the next round of hype. We believe that this stock will eventually collapse as it is unlikely that they will be able to live up to its promises.

Nonetheless, if you are long make sure you manage this with solid risk management, but staying long as momentum continues is the right decision for now. However, we prefer other stocks within the sector to play the momentum.

Disclaimer: This article is for informational purposes only and does not constitute financial or investment advice. All opinions are based on publicly available information and reflect the author’s judgment at the time of writing. Investors should conduct their own research before making any investment decisions. The author does not hold a position in QUBT at the time of publication. We did not receive any remuneration for writing this article.