Hims & Hers: A Potential 100-Bagger In the Making?

Hi everyone!

I’m pleased to announce Agrippa’s first article for the Stock Info Substack. Agrippa’s first article is a mega piece about HIMS 0.00%↑ , what else did you expect? Agrippa is well-known in the Hims & Hers community on X, formerly known as Twitter.

I hope you will all enjoy this mega article, with that being said, take it away, Agrippa!

Introduction

In this article, I will delve into an investment case for Hims & Hers, a leading telehealth company listed under the ticker symbol $HIMS. It's important to note that I am an investor in the company, and this discussion is intended solely for educational purposes and is not investment advice.

Hims & Hers was founded by Andrew Dudum in late 2017, and he remains as CEO to this day. The company went public in early 2021 through a merger with Oaktree Acquisition Corp., a special purpose acquisition company (SPAC), debuting on the market with a valuation of $1.6 billion. Their mission is to help the world feel great through the power of better health.

With a thriving subscriber base that has increased to 1.3 million as of Q2 of 2023—more than tripling since its IPO—the company's valuation currently stands at a market cap of $1.37 billion.

This article is set out to be a thorough A-Z analysis, unpacking Hims & Hers' business model, competitive edge, and its overarching strategy within the telehealth sector.

Business Model

Hims & Hers operates as a comprehensive “Health & Wellness'' platform, distinguishing itself through its tailored offerings via the Hims platform for men and the Hers platform for women, each with a dedicated website and mobile app. The essence of Hims & Hers’ business model is anchored in the provision of medications, chiefly aimed at managing chronic illnesses and longer duration medical problems.

Hims & Hers primarily sells over-the-counter (OTC) or prescription drugs, offering the prescription free of charge if deemed necessary by their network of medical doctors, who operate as independent contractors for the company. Most of their offerings comprise generic medications, which are essentially equivalents of brand-name drugs, having the same usage and effects, but are usually sold at lower prices. They do not sell any controlled substances, which are subject to much stricter regulations.

Hims & Hers sets itself apart by offering uniquely formulated medications through a process known as pharmaceutical compounding. This process enables the creation of distinctive, user-friendly forms of medications, enriching the customer experience while adhering to the company's ethos of delivering cost-effective healthcare solutions.

For instance, they have creatively reimagined common erectile dysfunction (ED) treatments such as Cialis, Levitra, & Staxyn into flavored “Hard Mints”, combining these drugs at different dosages into an enjoyable mint. Additionally, the company has curated a formulation that melds ED pills with cholesterol-lowering statins, offering a dual benefit of addressing erectile dysfunction while supporting heart health. Another example of their compounded proprietary formulations are the lemon-flavored "Hair Blends" chewables, which contain the two potent hair loss medications of Finasteride and Minoxidil.

The requirement for prescriptions for certain medications is seamlessly integrated into the Hims & Hers platform, where clients can either fill out a survey or schedule online consultations with licensed MDs right through the platform. Additionally, Hims & Hers extends 24/7 live support with medical providers for existing clients, enabling them to pose unlimited questions and receive medical support at no extra cost.

Furthermore, the subscription service model enhances the accessibility and affordability of these healthcare solutions, offering different pricing tiers that become more economical with longer subscription durations. Free shipping and discreet packaging are additional advantages that enhance the appeal of this customer-focused model.

This holistic business model of Hims & Hers embodies a modern, digitally-driven healthcare ecosystem that merges convenience with affordability while offering innovative medication formulations to render effective and user-friendly healthcare solutions.

Pharmaceutical Compounding

To understand Hims & Hers' unique value proposition, one needs to understand what pharmaceutical compounding is. At its core, pharmaceutical compounding is the art and science of creating personalized medications tailored to an individual's specific needs. Historically, this was the essence of pharmacy — pharmacists crafted each medicine by hand for each patient. However, as cheap, mass-produced medicines became the norm due to their convenience and the ability to produce them on a large scale, the practice of compounding largely receded into the background, seen as too labor- and time-intensive for widespread use.

Despite this, compounding has made somewhat of a resurgence in recent years, particularly in areas such as personalized skincare products. This resurgence is partly due to a growing interest in customized healthcare solutions that address specific patient needs that off-the-shelf products cannot meet. Even so, compounded medicines remain a relatively small niche. The main challenge lies in the difficulty of producing these personalized medications at scale, which has historically limited the reach of compounding pharmacies to a local or regional market.

Enter Hims & Hers. As a company, Hims & Hers stands out as one of the first market players to successfully navigate the complexities of compounding medications while maintaining high gross margins — around 80%. They have managed to scale the production of compounded medications in multiple domains, including skincare, hair loss treatments, and erectile dysfunction (ED) medications. By leveraging telemedicine and direct-to-consumer models, Hims & Hers is breaking new ground.

The company has harnessed the traditional values of pharmaceutical compounding — personalization and specificity — and combined them with modern manufacturing and distribution processes. This unique approach allows Hims & Hers to offer the kind of tailored healthcare once only available through local compounding pharmacies to a much broader market. In essence, Hims & Hers is actively working to bring personalized, compounded medications into the mass market, merging the old with the new in a promising and potentially transformative way.

Payment model

The company does not yet work with insurance providers, hence customers have to pay out of pocket. The company’s management team perceives this payment model to be more advantageous for customers, particularly those with high deductible insurance plans. It arguably reduces friction and potential decision-making delays by the customer, eliminating the need for customers to contact their insurance providers for every transaction.

Nevertheless, the company is open to integrating insurance reimbursements for future specific conditions and categories where cash payment isn't a feasible option, showcasing a flexible approach to payment models in line with customer needs and market demands.

Furthermore, the subscription model is a cornerstone of Hims & Hers' business approach, offering products across varying durations to cater to the continual needs of their clientele. In Q2 2023, the management team highlighted an enhanced pricing strategy to make longer duration subscriptions more appealing to customers. They have implemented price reductions ranging from 25% to 30% in some instances, demonstrating a proactive measure to incentivize sustained engagement with their platform.

Operations & Supply Chain

Hims & Hers operates significant pharmacy and fulfillment facilities, including a 300,000 square feet facility in Ohio and a 25,000 square feet pharmacy in Arizona. The company currently conducts its pharmaceutical compounding operations at its dedicated pharmacy in Arizona. Plans are in place to expand these operations to their facility in Ohio in the future.These in-house operations are bolstered by established partnerships with a network of affiliated and partner pharmacies across the United States and the UK. As of Q2 2023, 70% of total orders were handled by affiliated facilities, up from 55% the year prior.

Current Product Offering

Hims began its journey towards the end of 2017, initially launching with two core categories: Sexual Health and Hair Care on the Hims platform. As time progressed, the Hers platform was introduced, starting with the same two categories but with the addition of Skin Care. Fast forward to today, both platforms have expanded their offerings to include Sexual Health, Hair & Skin Care, and Mental Health.

The products within these categories are a mix of personalized proprietary treatments and legacy products. Legacy products are those traditionally known in the market such as generic Viagra, standalone Minoxidil for hair loss, and generic Lexapro for depression. On the other hand, personalized treatments are custom-tailored to the individual needs of the users. These include innovative products like the previously mentioned "Hard Mints”, or previously described “Hair Blends”, which are compounded based on the user's specific requirements.These custom formulations are determined through a survey filled out by the user, detailing their specific situation through multiple questions.

The shift toward personalized treatments is surging, now representing over 35% of the company’s online revenue in Q2 2023, with more than 20% of subscribers opting for these customized offerings. Newer market categories like mental health are growing at a mid-triple-digit rate and showing robust quarter-over-quarter unit economic improvement according to comments by Andrew Dudum, the company’s CEO.

Included in their comprehensive membership plans, Hims & Hers offer patients the valuable benefit of daily messaging access to medical doctors, allowing for consistent and personalized medical consultation. Additionally, members can schedule digital follow-up visits throughout the year without incurring additional fees, offering continuous care and convenience.

Primary Care:

Hims extends its reach beyond specialized care into the realm of "everyday health" and primary care, catering to a variety of common health issues typically addressed by a General Practitioner. Through their app, users can detail their health concerns, upload relevant images, and select a nearby pharmacy where prescriptions can be sent to. For a flat fee of $39, users can make use of this tele-health service which guarantees a response from a licensed Medical Doctor within a 24-hour window.

It's notable that while this service facilitates prescription issuance, the actual procurement of prescribed medication is carried out at external pharmacies, not through the Hims platform, allowing customers to locally obtain the necessary medications. This service streamlines the usually time-consuming process of scheduling and attending in-person doctor visits, making primary care more accessible and convenient.

According to their most recent 10Q filing, service revenue, which includes this consultation service, accounts for less than 10% of the company's revenue. While this service enhances the overall customer experience and accessibility to primary care, it's not a significant revenue driver for Hims & Hers.

Apostrophe:

In the first half of 2021, Hims & Hers acquired Apostrophe, a notable teledermatology platform and compounding pharmacy based in the US, to bolster its dermatology offerings. This strategic acquisition facilitated a significant expansion in personalized dermatology treatments on both the Hims and Hers platforms. Since the acquisition, the range of skincare products available on both platforms has seen a substantial increase, enriching the options available to consumers seeking dermatological solutions.

Despite its integration, Apostrophe continues to operate as a standalone entity, offering personalized skincare treatments. Much like Hims & Hers, Apostrophe also adopts a subscription-based model for its offerings.

New & Upcoming Product Offering:

Heart Health:

On July 31, 2023, the Hims platform branched out into the cardiovascular health sector, currently with a single offering that combines ED treatment with cholesterol-lowering statins. This new venture, termed Heart Health by Hims, is a part of a larger ambition to offer holistic, personalized health and wellness solutions. The initiative provides a way for healthcare providers to personalize sexual health treatments that also support cardiovascular health by combining active ingredients found in clinically proven medications into a single pill.

This endeavor is bolstered by strategic collaborations. A notable partnership with the American College of Cardiology (ACC) supports Hims & Hers' ongoing commitment to clinical excellence. The Heart Health by Hims approach is rooted in clinical protocols based on ACC's Atherosclerotic Cardiovascular Disease risk estimator principles. Moreover, Heart Health by Hims customers will have access to cardiovascular health resources and educational materials through CardioSmart.org, the ACC’s patient engagement initiative.

Additionally, a partnership with Labcorp will soon facilitate lab-based heart health testing for Heart Health by Hims customers. Lab results will be integrated directly into the Hims & Hers proprietary electronic medical record system, which aids in further personalizing care.This initiative reflects a step towards identifying individuals with elevated cardiovascular disease risk factors and connecting them with preventive care.

According to hims’ management team, the expansion into the cardiovascular area is strategically aimed at catering to an older demographic, broadening the scope of Hims & Hers' target audience. While the Heart Health product is priced at a premium, the pricing strategy still aligns with the company’s objective of maintaining mass-market accessibility, ensuring a broader spectrum of individuals can benefit from this initiative.

The move into the realm of cardiovascular health with the introduction of combined ED and cholesterol-lowering statin treatments marks a significant shift towards preventative healthcare for Hims & Hers. By extending its offering of health services to include preventive measures, the platform not only addresses immediate health concerns but also looks to the future, focusing on reducing the risk of chronic diseases.

Weight Loss:

Hims & Hers plans on launching a weight loss category towards the end of 2023. Initially, GLP-1 products for weight management won't be available due to concerns over consistent delivery, supply chain issues, and emerging new side effect profiles. However, they are targeted for potential inclusion in the future.

Initially, a mix of generic and personalized treatments will target the underlying causes of weight gain like metabolic resistance, hormonal issues, and mental health concerns. Moreover, the weight loss category will encompass a holistic approach including behavior modification, nutrition, and fitness coaching.

In the Q2 2023 earnings call CEO Andrew Dudum has also emphasized the holistic approach required for effective weight management, which encompasses good nutrition, physical activity, and adequate sleep. Upcoming app improvements, including enhanced content, nutrition tools, and tracking features, aim to provide a comprehensive approach towards weight management setting a solid foundation for a more integrated and health-centered user experience.

Potential Future Categories & Product Releases:

Hims & Hers has hinted at further expansion into areas crucial for holistic healthcare. One notable avenue is their potential delve into hypertension and hyperlipidemia management, aligning with their recent venture into heart health. The initial offering within the heart health category—a blend of cholesterol-lowering statins with ED medications—targets hyperlipidemia. This move suggests a broader framework that could see more products launched within this sub-category as part of a comprehensive heart health suite. Hypertension, another significant part of cardiac care, could also see dedicated product releases as part of this expansion.

In the Q2 2023 earnings call, the management illuminated the replicable infrastructure crafted for cardiac care, outlining its potential application to other chronic conditions like metabolic disorders, insulin-resistant disorders, diabetes, menopause, hormonal balancing, and weight management. This insight hints at a well-charted roadmap where these categories could be seamlessly integrated into the Hims & Hers platform in the near future.

In reflecting the long-term ambitions of Hims & Hers, the management team has previously articulated the company's aspiration to unveil approximately two new categories per year.

Geographical Markets

United States:

Hims & Hers has a presence across all 50 US states, although Puerto Rico is excluded, and certain treatments are available only in select states.

UK:

Expanding its geographical footprint, Hims & Hers ventured into the UK market in H1 2021 through the acquisition of London-based health platform, Honest Health. This strategic acquisition not only broadened the company's product portfolio with a focus on hair loss treatments—such as compounded topical Finasteride with Minoxidil solution—but also leveraged an exclusive partnership with a UK compounding pharmacy and fulfillment center. This move significantly enhanced its distribution capabilities in the region, particularly in pharmaceutical compounding. During the Q2 2023 earnings call, CEO Andrew Dudum shared optimistic insights regarding the UK operations, highlighting a mid-triple digit growth rate and strong quarter-over-quarter unit economic improvement.

Potential Future Market Expansion:

Hims & Hers views markets that share similar consumer dynamics and regulatory landscapes with the US as favorable for potential expansion. This includes regions like the UK, Western Europe, and possibly extending to countries like Canada, Germany, and Australia. The management has also shed light on past engagements with health systems and regulatory bodies in Asia and the Middle East. Although these regions appear to be on the company's expansion radar, they are anticipated to follow a few years behind the expansion pace set in other mentioned markets.

Branding & Marketing Strategy:

Hims & Hers brand positioning caters to digital natives, primarily targeting millennials and Gen Z, while its recent expansion into heart health expands the demographic reach to include older individuals, all within a digital-first framework. The branding encapsulates a nuanced approach: Hims aims to destigmatize men's health issues, bridging the communication gap between men and the healthcare system. On the other hand, Hers strives to streamline and personalize the healthcare journey for women who typically find traditional systems cumbersome. This dual branding strategy effectively addresses the unique healthcare needs and perceptions of both genders, under a unified ethos of providing personalized, digital-first healthcare solutions.

Transitioning from a direct response marketing strategy to a destigmatizing, awareness-based approach since late 2020, Hims & Hers has invested in long-term brand equity and visibility. This is reflected through high-visibility placements and traditional brand awareness campaigns. The omnichannel marketing strategy encompasses various platforms including social media, TV spots during major sporting events (NFL, NBA, UFC), streaming channels such as Hulu, and both influencer and celebrity endorsements. Notable celebrity partnerships formed with Jennifer Lopez, Miley Cyrus, NFL star Rob Gronkowski, and Kristen Bell, who is the brand ambassador for Hers’ mental health division, have been instrumental in enhancing brand trust and market reach.

Furthermore, strategic retail partnerships have extended Hims & Hers’ presence into over 20,000 retail locations via collaborations with major retailers like Target, Walgreen’s, CVS, Bed Bath & Beyond, and The Vitamin Shoppe, along with an online retail collaboration with Urban Outfitters. Though primarily a marketing and branding mechanism, these partnerships also offer a tangible touchpoint for customers, aligning with the blended online and offline approach adopted by Hims & Hers to engage a wider audience. This comprehensive marketing approach harmoniously intertwines with the brand's narrative, resonating with the modern consumer's evolving healthcare expectations.

MedMatch - Hims’ AI initiative

In Q2 2023, Hims filed for a trademark for their AI initiative named MedMatch. According to the CEO Andrew Dudum, MedMatch employs AI to analyze past patient outcomes, cross-referencing treatment success with patient characteristics. This insight enables it to recommend the most likely successful treatment and dosing for new patients based on their specific issues and traits.

This initiative holds greater significance than it might initially appear. Traditional medical approaches often resemble a "trial and error" method when treating new patients. More seasoned doctors typically pinpoint effective treatments more swiftly due to their accumulated experience (i.e. data), allowing them to recognize patterns that lead to better recommendations.

Machine learning elevates this process, moving beyond mere intuition to methodically quantify and analyze data. With this advanced approach, Hims & Hers could be positioned to offer superior and more personalized recommendations and treatment plans.

Governance & Talent Pool:

Hims & Hers has a governance structure composed of a Board of Directors, an Executive Management Team, and a Medical Advisory Board. The board includes individuals with significant experience in the medical and tech sectors. Andrew Dudum, the CEO, has a background in fostering startups, including his involvement with Atomic Labs. Furthermore, professionals such as Dr. Toby Cosgrove, with his tenure as the President and CEO of the Cleveland Clinic, offers medical insights to the board.

The Executive Management Team members each have specific expertise relevant to their roles. Among the notable members, Melissa Baird, the Chief Operating Officer, has experience in the direct-to-consumer sector, with previous executive roles at Draper James and Bonobos. Yemi Okupe, the Chief Financial Officer, has financial experience derived from leadership roles at companies such as Uber, eBay, PayPal, and Google. Dr. Pat Carroll, the Chief Medical Officer, emphasizes care quality, having served in the same role at Walgreens from 2014-2019.

Hims & Hers also recently welcomed Khobi Brooklyn as the new Chief Communications Officer. She has extensive communication expertise from roles at firms such as Square, Tesla and Nike. Moreover, in December of 2022, the company added Dr. Scott Knoer as their first-ever Chief Pharmacy & Innovation officer. Dr. Scott Knoer previously held leadership roles as the Executive Vice President and CEO of the American Pharmacists Association (APhA). He is in charge of overseeing the company’s compounding facilities in Ohio and Arizona, leading the development of Hims & Hers’ proprietary formulations.

By Q4 2022, the company's employee count was 651, an increase from 398 the previous year. Given its overall business growth, it's fair to assume that the headcount has risen significantly since then. However, the head count relative to its revenue suggests that the company operates with a lean organizational structure.

Growth & Expansion Strategy:

The primary growth strategy of Hims & Hers is organic growth through category expansion and diversification of product offerings. Nevertheless, the company is open to strategic Mergers and Acquisitions (M&As) under distinctive circumstances. Previously management has highlighted that the company receives hundreds of M&A opportunities annually, yet very few meet their criteria which revolve around unique talent, capabilities, or infrastructure that could significantly improve customer experience.

Their previous acquisitions of Apostrophe and Honest Health exemplify this strategy, bringing in infrastructure and capabilities for delivering personalized treatments at scale. This is a rarity even in specialist settings, thereby reflecting the company's M&A strategy aimed at acquiring distinctive capabilities that deliver substantial value.

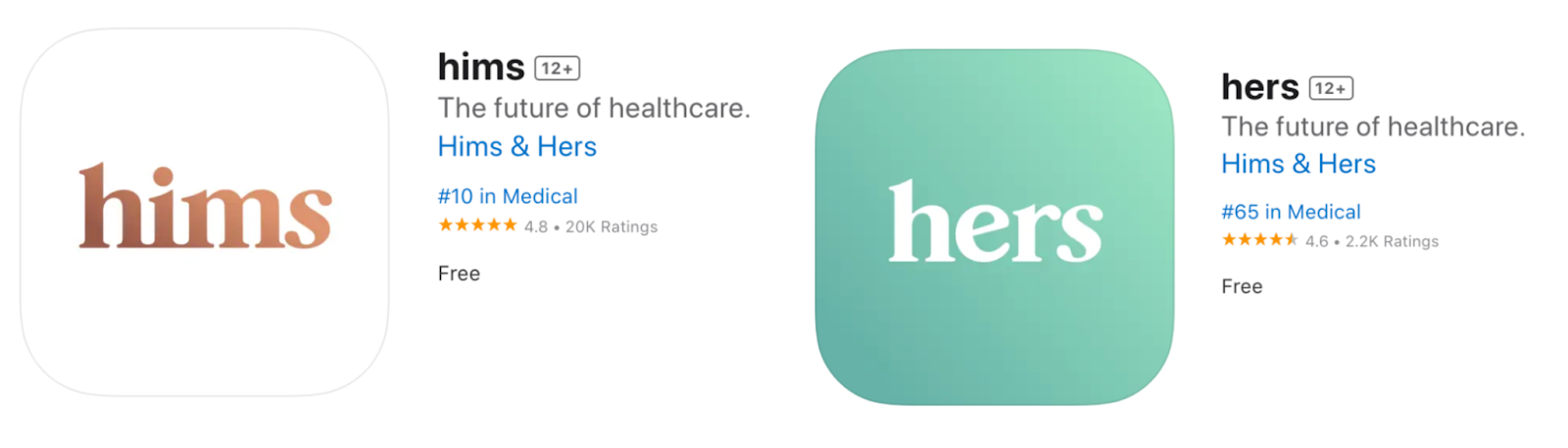

App Store Performance

The company's iOS apps, Hims and Hers, have made a successful entry into the App Store's Medical category since their launch last year, with Hims boasting an impressive user rating of 4.8 and Hers closely following with a solid 4.6 rating.

The Hims app is ranked #10 and Hers at #65 in the App Store's Medical category, with Hims achieving an all-time high rank of #5. While daily fluctuations are common, the notable 52% increase in total ratings for the Hims app since early August points to an impressive increase in user adoption over the past 3 months.

Competitive Environment:

In the dynamic telehealth sector, Hims encounters competition from 8 notable players: Amazon, Walmart, Costco, Cost Drug Plus, TelaDoc, Blue Chew, Keeps, and Roman. These competitors contend for market share across various fronts, adding diversity to the competitive landscape.

Amazon:

Amazon has ventured into the healthcare sector through Amazon Clinic and Amazon Pharmacy. Since August 1, 2023, Amazon Clinic has been operational across all 50 US states, offering virtual consultations for over 30 common health conditions. Utilizing a message-based portal, it facilitates rapid consultations with telehealth providers. Although insurance isn't accepted, it's FSA (Flexible Spending Account) and HSA (Health Savings Account) eligible. The pricing for consultations varies between $30 and $74, based on whether it's message-only or video-based, and it claims to provide a 24/7 service. Amazon Pharmacy complements this service by ensuring a smooth transition from consultation to medication fulfillment, with separate costs for medications.

Overall, Hims & Hers and Amazon largely compete in different domains. Amazon Clinic focuses on telehealth and primary care consultations, similar to Hims & Hers' primary care service which acts as a middleman between medical doctors and clients. Unlike Amazon Clinic, Hims & Hers provides more specialized offerings including proprietary health and wellness products.

Hims & Hers holds a competitive advantage against Amazon in categories where it offers branded products, as the consultations and prescriptions are provided for free with the aim of locking in multi-month subscriptions. In contrast, Amazon charges a minimum of $30 for consultations, which could deter potential customers aware of Hims & Hers' no upfront cost approach for this service.

While Amazon's brand recognition could make it a strong competitor in telehealth, Hims & Hers' main revenue comes from its branded products, a market Amazon hasn't entered.

Costco & Walmart:

Much like Amazon, both Costco and Walmart have moved into the telehealth sector, offering telehealth services and consultations at comparable prices. Their business model aligns closely with Amazon's approach, primarily competing against Hims & Hers on the ‘convenience’ front.

However, there's an argument to be made about the entry of these big players into the telehealth space. Their presence could potentially lend more credibility to the sector as a whole, indirectly benefiting Hims & Hers. The validation of telehealth services by such established retail giants may drive a broader acceptance among consumers, which could, in turn, drive more traffic to specialized telehealth providers like Hims & Hers, who offer a more personalized healthcare experience.

Cost Plus Drugs:

Founded by billionaire Mark Cuban, Cost Plus Drugs is a newcomer in the healthcare sector with a mission to reduce prescription drug costs. Their business model centers around a membership-based approach where members pay an annual fee of $60 to access lower drug prices. The company operates as a digital pharmacy, claiming to offer medications at market cost, plus a 15% markup and a $3 dispensing fee, aiming to provide transparency and cost-saving benefits to the consumers. Cost Plus Drugs requires individuals to obtain their prescriptions independently, potentially adding to the cost and time required to access necessary medications.

Cost Plus Drugs aims to disrupt traditional pharmacies with a reduced pricing model, ensuring a comprehensive selection of medicines with improved pricing transparency. Meanwhile, Hims & Hers offers a more holistic approach to healthcare offering both the prescription and the end product.

Moreover, Hims & Hers carves a niche in offering more personal and specialized treatments. While these tailored options are still catering to the mass market, they come at a pricing premium. Consequently, Hims & Hers' offerings are likely to always maintain a higher price point compared to the conventional medications available at Cost Plus Drugs. While Hims & Hers engages consumers with its personalized, convenient health solutions, Cost Plus Drugs is effectively competing in the domain of affordability, seeking to become the go-to for cost-conscious patients.

Teladoc:

Similar to Amazon Clinic, Walmart, and Costco Teladoc provides virtual healthcare services, allowing patients to consult with healthcare professionals remotely. However, Teladoc differentiates itself by operating on both B2B and B2C models, offering telehealth services to organizations and individuals. In the B2B domain, it partners with employers, hospitals, and insurance companies, while on the B2C side, it provides direct services to consumers for medical consultations. The business model revolves around membership fees, visit fees, and partnerships. Pricing for individual consumers varies with insurance coverage; General Medical visits can cost as low as $0 per visit with insurance, and $75 per visit without insurance.

Just like the previously mentioned competitors, Teladoc does not sell its own branded products or medicines, thus it doesn't directly rival Hims & Hers' core business model. However, similar to the likes of Amazon, Walmart, and Costco; Teladoc's service could lead to consumers receiving prescriptions which they can fill at traditional or online pharmacies, thereby bypassing Hims & Hers' offerings. Hence, while their core services differ, there is an indirect competition between them due to some overlap in the customer journey toward obtaining medications.

Blue Chew, Keeps, & Roman:

Blue Chew, Keeps, and Roman are consumer-oriented brands that market various medical products, both over-the-counter and prescription medications, positioning them as direct competitors to Hims. Blue Chew specializes in erectile dysfunction (ED) medications, while Keeps focuses on hair loss treatments. On the other hand, Roman has a broader offering, covering areas such as sexual health, hair and skin care, fertility, and weight loss, which brings it in closer competition with Hims & Hers. Like Hims & Hers, all three primarily operate on a subscription model, which does not integrate with health insurance plans. Additionally, all three companies offer the convenience of obtaining prescriptions for their medication offerings directly through affiliated medical doctors.

Keeps is dedicated to helping men prevent and treat hair loss. Their product range is similar to that of Hims in the hair care category, featuring treatments like Minoxidil, Finasteride, and 2-in-1 Finasteride-Minoxidil solutions. Unlike Hers, Keeps doesn’t offer hair loss treatments for women, nor do they offer flavored or compounded oral medications.

Blue Chew markets generic ED medications in flavored chewable forms, akin to Hims' flavored “hard mints”. However, they lack the compounding ability of Hims, as they don't offer personalized ED treatments at custom dosages. Additionally, unlike Hims, they don't offer products that mix ED medications with cholesterol-lowering statins, which furthermore sets Hims apart from them.

Roman emerges as a significant competitor to Hims, with a wide range of branded products across multiple categories. While they cater to both genders under the same platform, their offerings for women seem more limited compared to Hers. Noteworthy is Roman’s offering of GLP-1 injection drugs in the weight loss category, which Hims & Hers have chosen not to provide initially due to safety and availability concerns.

Like Hims & Hers, Roman has both a web platform and an app called “Ro”. In the "Medical" category of the App Store, Roman's app is at rank #174, holding an average rating of 4.8 from 1.8k reviews.

However, Roman appears to lack the personalization aspect that Hims & Hers emphasize. For instance, their ED treatments mainly involve reselling generic medications in pill form without the option for blending different medications into one customized pill. Apart from their 3-in-1 hair loss spray, Roman doesn’t seem to engage much in compounding or creating unique product formulations like gummies or flavored mints.

Largely, Roman comes across as a reseller of generic medications with branded packaging, lacking the creation of personalized treatments. This stands in contrast to Hims & Hers, who offer a more diverse range of categories and services for both men and women, along with a wider array of proprietary formulations focused on consumer personalization.

Does Hims have a Moat?

Determining whether Hims & Hers possesses a competitive edge primarily depends on one's stance regarding pharmaceutical compounding. Should one view personalized medicine merely as a passing trend, Hims & Hers' emphasis on such treatments wouldn't present a significant moat.

Nonetheless, I contend that the personalized care sector is set to flourish. Individual differences suggest that customized medications could enhance treatment effectiveness. The convenience of a single compounded medication, over multiple separate ones, holds particular appeal, especially for those managing chronic conditions daily. This is a service segment where many consumers are likely willing to pay a premium. With over 35% of Hims & Hers' recent online revenue coming from such personalized solutions, the demand in the market is evident.

Hims & Hers' investment in data and the development of the MedMatch initiative indicates a commitment to evolving their personalized offerings through AI and machine learning. Their network of pharmacies and production facilities underpins their ability to efficiently deliver high-quality, custom medications at controlled costs. The financial and expertise commitments required to establish such an operation are substantial, yet Hims & Hers has steadily made these investments.

Hims & Hers' holistic approach to healthcare significantly distinguishes it in the competitive landscape. Their diverse treatment options coupled with seamless doctor communication via one unified digital platform, deliver a unique and comprehensive healthcare experience. Among the competition, Roman stands out as the only direct rival providing a comparable holistic digital platform. Despite this, Hims & Hers maintains its edge with exclusive and personalized product formulations.

The company's brand-building efforts, via marketing and high-profile partnerships, further reinforce its market position. Although Hims & Hers is a relatively young company, these strategic moves are rapidly cementing its presence in the modern-day healthcare sector. I believe Hims & Hers already possesses a small moat, one that is poised to grow stronger as the company expands into new markets and offers an increasing variety of proprietary formulations.

Ownership Snapshot

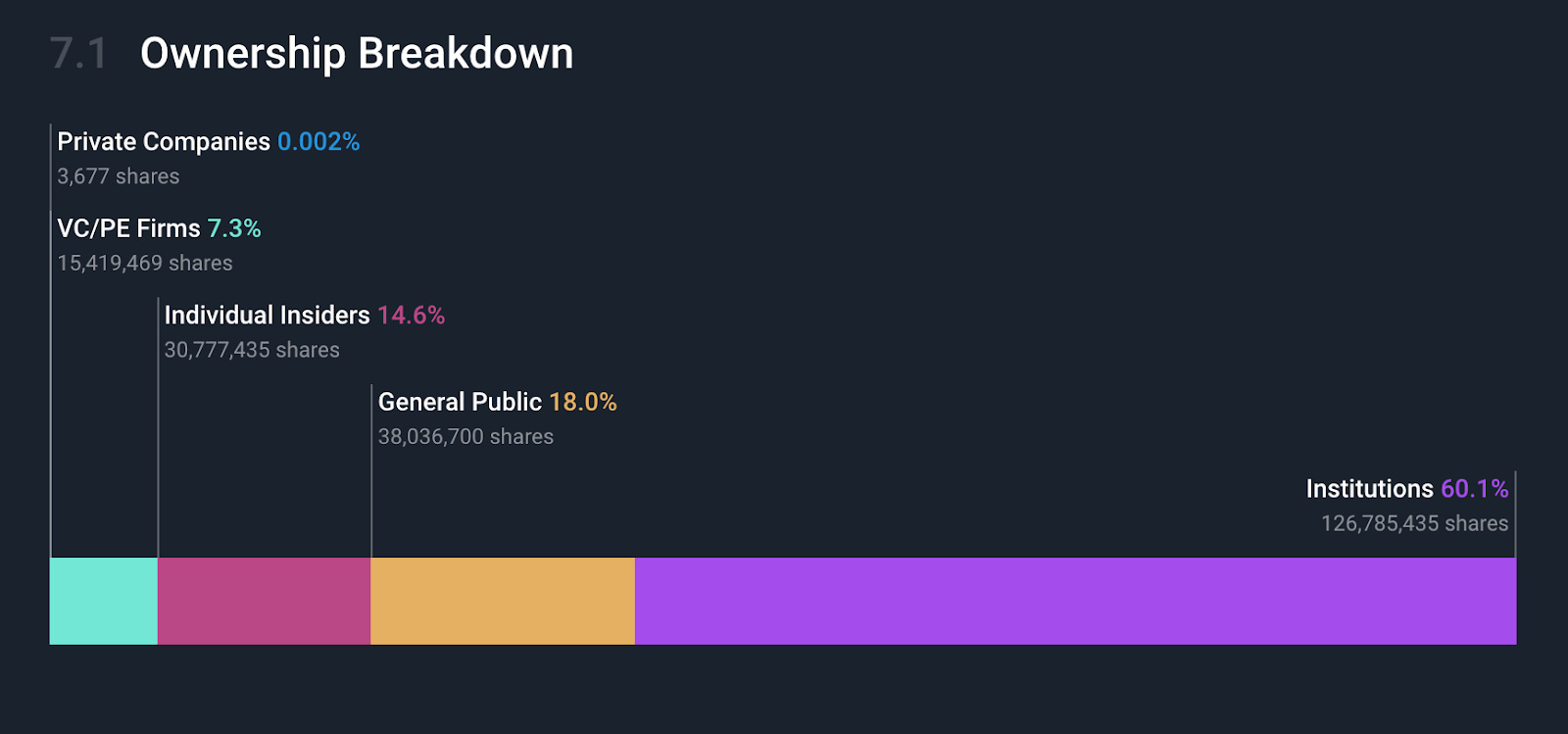

The share structure of Hims & Hers highlights a significant aspect of the company's governance. With 211 million shares outstanding, classified into Class A and Class V shares, the power dynamics are clear. Class A shares come with a standard one vote each, whereas the Class V shares—held exclusively by CEO and founder Andrew Dudum—carry 175 votes each. This structure effectively grants Dudum a controlling influence over corporate decisions, illustrating his commitment and confidence in the company’s direction.

Insider ownership stands at a substantial 14.6%, with Andrew Dudum himself holding 9.5% of the total shares, according to Simply Wall Street. Venture capital, private equity firms, and other institutions collectively own 67.4%, while retail investors account for 18%. The shifting tides of ownership have seen retail participation decline from over 31.4% in March 2023 to the current 18%, in comparison to the rise in institutional holdings from 46.6% to 60.1% over the same period. Moreover, institutional ownership stood at about 55% just before the Q2 earnings release and has since increased even further, indicating that institutions likely viewed the Q2 results favorably.

This shift suggests a growing institutional belief in the company’s future, while retail investors appear to show caution. From a shareholder perspective, the increasing institutional stake could be perceived positively, as these entities are often regarded as informed and stable investors, potentially smoothing out price volatility due to their longer-term investment horizons.

Financial Analysis

In this chapter, we'll examine the financial trajectory of Hims & Hers since its 2021 IPO, including a retrospective glance at select 2020 metrics revealed in 10Q filings for year-over-year analysis in 2021. Notably, Hims & Hers has demonstrated exceptional financial performance to date.

Top & Bottom line:

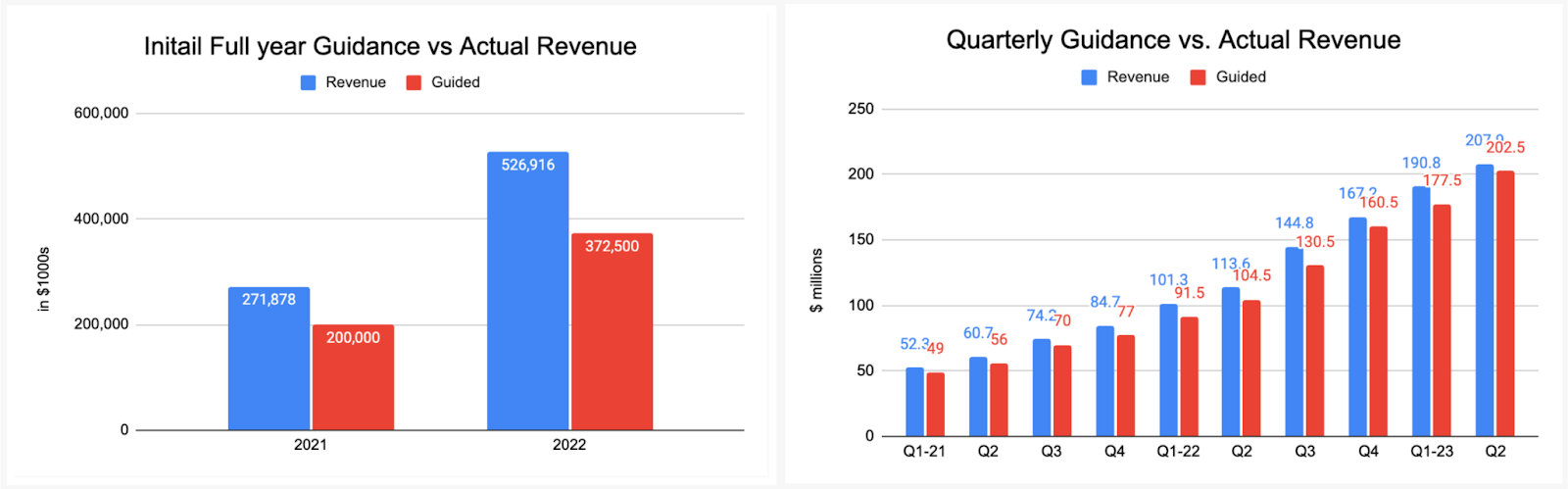

The company's quarterly revenue soared from $30 million in Q1 2020 to $208 million in Q2 2023, marking a compounded annual growth rate (CAGR) of roughly 74%. Despite this, net income has remained in the red, indicating ongoing unprofitability. Nonetheless, over the last five quarters, the company has notably narrowed its net loss each consecutive quarter, edging closer to profitability.

Management has set a long-term target of reaching at least $1.2 billion in annual revenue and a minimum of $100 million in adjusted EBITDA by 2025. For 2023, they forecast revenue between $830 million and $850 million with an adjusted EBITDA of $35 to $40 million. Considering the company's trajectory and proximity to GAAP profitability, I expect Hims & Hers to achieve profitability, likely by 2024.

It's also important to note the company's conservative approach to guidance, having consistently surpassed its own forecasts since going public. Without fail, it has exceeded both annual and quarterly projections, often revising its guidance upwards throughout the fiscal year. With this pattern, the 2025 targets announced in Q1 2023, which CEO Andrew Dudum described as a 'floor', are likely to be adjusted higher in future revisions.

Margins:

Currently, with gross margins above 80%, Hims & Hers has been demonstrating robust profitability at this level. This is due to its strong pricing strategy and operational efficiencies. Despite negative operating and net margins, the trend over the past six quarters indicates improvement. Management expects gross margins to eventually level off around the mid-70s percentile. Interestingly, the company’s net margins have outpaced operating margins, benefiting from the positive returns on short-term bonds, thus gaining an indirect advantage from the current high-interest rate climate.

Since its IPO, operating expenses, excluding marketing, as a percentage of revenue, have steadily declined, signaling increasing operational leverage. Conversely, marketing expenses have remained consistently around 51% of revenue, reflecting a bold growth strategy. While allocating over half of revenue to marketing might seem overly aggressive, the company's remarkable expansion validates this tactic, with revenue growth outpacing all other expenses and nearing breakeven net margins. In other words, the efficacy of marketing investments is evident in the substantial top-line growth. Nonetheless, for long-term sustainability, a reduction in marketing expenses relative to revenue will be essential to steer the company towards profitability.

Cash & Debt:

Hims & Hers boasts a robust balance sheet with $193 million in cash, cash equivalents, and short-term investments, though this is a reduction from the $323 million held at the time of its IPO. Despite this decrease, the company's cash reserves have been on an upswing for the last two quarters, coinciding with its achievement of positive operating cash flow for the first time in consecutive quarters. The absence of debt coupled with a positive cash flow trajectory virtually eliminates the risk of bankruptcy, contingent on the continuation of positive cash flow trends.

While Hims & Hers' operating cash flow has improved, this has paralleled an increase in stock-based compensation (SBC) in absolute terms. Nevertheless, when scaled to revenue growth, SBC has remained stable, suggesting that the surge in operating cash flow isn’t merely a byproduct of unusually high stock compensation awards.

Dilution:

Hims & Hers is experiencing steady, albeit minimal, growth in basic shares, currently totaling 208 million. Basic Share count is the actual number of outstanding shares. However, there's a notable rise in potential dilution (Dilutive Share count) from stock options, RSUs, and warrants, largely due to expansive stock-based compensation plans. This increase isn't necessarily indicative of future basic share count growth, as these potential shares could expire without value. Moreover, certain dilutive securities are contingent on performance milestones; for instance, CEO Andrew Dudum stands to vest 1,623,070 stock options only if the share price hits a minimum of $38.31.

It's important to note that stock-based compensation (SBC) could lead to less dilution if Hims & Hers' share price were to rise, since compensation costs measured in dollars would require issuing fewer shares. Conversely, a lower share price would necessitate more shares for the same compensation value, increasing dilution. Despite this, given the company's robust growth, the current level of dilution seems manageable. The company's ability to attract and retain exceptional talent through SBC is vital, with their interests aligning with the company's goals. Nonetheless, it would be ideal for dilution to stabilize at an annual rate of not more than 2%.

Risks

This section outlines the primary risks from my perspective, which are crucial for every prudent investor to consider for a comprehensive understanding of potential challenges. It is essential to weigh these factors carefully when evaluating the company's future prospects.

Misunderstood Business model:

A significant motivation for writing this article was to demystify Hims & Hers' business model for the investor community. As someone who regularly engages with other investors on X, I've observed a gap in understanding, particularly regarding Hims’ innovations in pharmaceutical compounding. There's a lack of awareness about what medical compounding is and how it enables Hims & Hers to provide personalized treatment options, which is more sophisticated than merely reselling generic medications—a misconception I believe others should reserve for competitors like Roman.

The clarity of a company's business model is not just a matter of convenience for investors; it is a significant factor in their confidence and willingness to invest. When potential and current investors struggle to comprehend the core operations, unique value propositions, and future potential of a company, it can lead to undervaluation and underperformance in the stock market. For Hims & Hers, the complexity of their operations in pharmaceutical compounding—a niche yet critical aspect of their business—is not commonly understood. This obscurity poses a tangible risk as it can deter investor engagement and lead to a persistent gap between the company's intrinsic value and its perception in the marketplace. Addressing this communication gap is thus not just an opportunity, but a necessity to ensure investor trust and to accurately reflect the innovative strides the company is making within the industry.

In my view, this confusion can be attributed to Hims & Hers' need for clearer investor communications. While their Investor Relations site contains a wealth of information, including news articles, presentations, and earnings call transcripts, the presentation of this data could be more streamlined and accessible. By enhancing their online communication, especially on platforms like X, and improving their investor relations website, they could significantly reduce misunderstandings and potentially improve their market valuation.

Many B2B SaaS companies excel in clarifying their business models and value propositions through detailed, visually engaging websites, complete with explanatory videos and graphics. These resources, primarily designed for clients, also serve as a valuable tool for investors seeking a deeper understanding of the business. Hims & Hers, as a consumer-focused B2C brand, and hence their customer-facing website prioritizes consumer engagement over detailed explanations of their business model. Therefore, it would be highly beneficial for Hims & Hers to revamp their investor relations website, incorporating elements that offer a comprehensive overview of their business operations. Such an upgrade could provide the clarity needed to bridge the informational gap and allow investors to grasp the full scope and nuance of their business model beyond the consumer interface.

The recent appointment of Khobi Brooklyn as Chief Communication Officer, with a focus on investor relations, is a promising step that suggests management recognizes the need for better communication. With her expertise, there's potential for substantial improvements. I look forward to seeing these changes implemented before fully endorsing the positive impact of her role.

Product Diversification & Lack of Transparency:

Hims & Hers faces a significant risk in its perceived limited scope, primarily recognized for its hair loss and ED products. Despite expanding into skincare and mental health since their IPO, the lack of segmented revenue disclosure leaves investors guessing about the financial contribution of each product line. Additionally, the absence of separate earnings data for the Hers platform raises questions about its performance.

While it is understandable for a relatively new company to focus on its initial successful offerings, investors would benefit from greater transparency regarding the revenue breakdown by platform and product category. This level of detail would offer a clearer picture of growth areas and the company's evolution beyond its flagship products. Hims & Hers' reluctance to disclose detailed information presents an obstacle for investors seeking transparent insights into the company's revenue streams.

SPAC overhang:

Launching as a SPAC casts a shadow over the company's stock, largely due to the negative sentiment surrounding many SPACs perceived as underwhelming investments. While Hims & Hers' decision for a SPAC merger likely stemmed from the desire for an expedited public listing, aligning with the company's dynamic nature, the general stigma attached to SPACs weighs on its stock.

That said, the essence of being a SPAC doesn't inherently disadvantage the company beyond this association. I view this situation as a temporary bias that will dissipate as the market shifts its focus from the method of going public to the company's actual performance. In this light, the SPAC route may present a strategic opportunity: should the stock have debuted through a traditional IPO, it might have commanded a more favorable valuation at present.

Acquisition:

The potential for Hims & Hers to be acquired by a larger company, given its current valuation of around $1.3 billion, might appear to be a considerable risk. Nevertheless, this risk is mitigated by the concentrated voting power held by CEO Andrew Dudum. With his approximately 8.37 million Class V shares, each wielding 175 times the voting power of the ordinary Class A shares, Dudum has decisive control over significant corporate actions, including acquisition proposals. His majority voting rights effectively safeguard the company from any unwanted takeover attempts. Andrew Dudum’s dedication to the company's long-term growth and his vision for its future strongly suggest that he would be averse to agreeing to a sale, especially prematurely.

High Churn:

Hims & Hers' churn, which is a measure of the percentage of subscribers who discontinue their service within a certain timeframe, is not publicly disclosed in its entirety. The company emphasizes a subscriber revenue retention rate of at least 85% for those with a tenure of over two years, implying a churn rate of 15% for these longer-term customers. Yet, information from a Q1 2022 cohort indicates that the first-year retention rate might be closer to 50%, improving significantly for subscribers who stay beyond that initial period.

My analysis on social media platform X, which involved an in-depth churn rate calculation, suggested that the overall annual churn rate for Hims & Hers might be around 34%. This is relatively high but must be contextualized within the company's rapid growth trajectory, where a large portion of the customer base are in their first year of subscription, a period which naturally experiences higher churn.

The current churn rate is less concerning when considering the company's robust year-over-year revenue growth of over 80%. It's evident that the high churn has yet to materially impact financial performance. Additionally, the company is taking strategic steps to manage and potentially reduce churn, including incentivizing longer-term subscriptions through price reductions.

The key takeaway is that while a high churn rate generally requires attention as it can burden revenue growth, in the case of Hims & Hers, the impact is mitigated by the company's aggressive growth and proactive measures to retain customers. It will be essential, however, to monitor how churn trends as the company matures and the growth rate normalizes.

Profitability:

The path to profitability is a critical consideration for Hims & Hers, as with any company. The inability to achieve GAAP profitability with substantial net margins is a risk for the company and its investors. Ownership of shares in a business that fails to become profitable is tantamount to holding a non-yielding asset. Growth-focused companies typically postpone profitability and their market value is primarily driven by the potential of future earnings.

Despite the speculative nature of investing in unprofitable companies, due to the uncertainty surrounding their ability to turn a profit, Hims & Hers appears to be on the cusp of profitability, with a relatively narrow net margin deficit of -3.5%. It's my perspective that the company's ongoing lack of profitability is a deliberate strategic choice; the substantial investment in marketing is fueling impressive growth rates.

There is likely a calculated trade-off at play here: the company could potentially cut back on marketing expenses to achieve short-term profitability, but this could come at the cost of long-term growth. Instead, Hims & Hers is opting to invest in brand-building and awareness campaigns. While such marketing efforts can be costlier upfront compared to direct advertising tactics, they can foster sustainable organic growth, leading to a natural decrease in marketing expenses as a percentage of revenue over time.

The strategic approach to marketing, with a focus on building brand awareness, suggests that the company is laying the groundwork for a self-sustaining and organic customer acquisition model that could lead to reduced marketing spend and, consequently, a path to profitability. Investors and analysts will need to closely monitor how these investments in brand-building translate to long-term profitability and whether the company can adjust its spending effectively without stifling growth.

Questionable Moat:

The perceived strength of Hims & Hers' competitive moat largely depends on the value placed on personalized medicine. Their substantial investment in this area suggests it may be challenging for competitors to replicate their niche position swiftly. Yet, if one views the company merely as a distributor of generic medications, the moat appears less formidable, given the cheaper alternatives available through competitors such as Cost Plus Drugs.

Investors should closely observe the evolution of Hims & Hers' product offerings in personalized medicine to gauge market reception. Presently, with over 20% of their customers choosing personalized treatments, it's critical for investors to track this percentage for growth. An increasing trend would not only validate the company's strategic direction but also strengthen the case for a sustainable competitive moat in the personalized healthcare market.

Dilution:

Dilution is another critical factor to monitor, especially for a company with substantial growth prospects like Hims & Hers. While the current dilution rate is justifiable in light of the company's growth trajectory, investors should keep a vigilant eye on the share count. Presently, the basic share count is rising at a measured rate, suggesting that dilution is under control. However, shareholders would be well-advised to keep this metric on their radar to ensure that any future equity issuances do not excessively erode their stake in the company’s potential upside.

Regulatory Risks:

The landscape of telehealth is rapidly evolving, and with it comes a heightened sense of regulatory risk, particularly in markets such as the USA and UK where Hims & Hers is operational, as well as any other regions the company may enter in the future. The healthcare sector, known for its stringent regulations, presents a complex regulatory environment that any player in this field must navigate carefully.

Despite the inherently regulated nature of the healthcare industry, the entry of major corporations like Amazon, Costco, and Walmart into the telehealth market serves as a strong validation of the sector's longevity and potential. These companies, with their robust compliance frameworks and resources, would not venture into an area with an uncertain regulatory future, suggesting a stable path forward for telehealth services.

Hims & Hers exhibits a conscientious approach to this regulatory landscape. The company has strategically chosen not to deal in controlled substances and to offer products composed of generic medical compounds that have received FDA approval. This cautious selection of product offerings minimizes regulatory scrutiny and aligns with best practices for risk management.

Additionally, Hims & Hers has shown prudence by deciding to avoid the new GLP-1 weight-loss drugs for the time being, citing concerns over potential long-term side effects. This decision underscores the company's commitment to patient safety and its proactive stance in mitigating regulatory risk.

Governance at Hims & Hers is another area that inspires confidence regarding regulatory compliance. The company's leadership includes medical professionals who bring years of experience in working with regulatory bodies within the healthcare sector. This expertise is instrumental in guiding the company through the intricacies of healthcare regulations and in maintaining rigorous standards of compliance.

Nonetheless, investors should remain alert to the shifting sands of healthcare regulations. It is vital to monitor new legislative developments and to evaluate how Hims & Hers adapts to these changes. While the company's current approach reduces exposure to regulatory risk, the unpredictable nature of healthcare laws necessitates ongoing vigilance from both the company and its investors.

Fair Value Assessment & Conclusion:

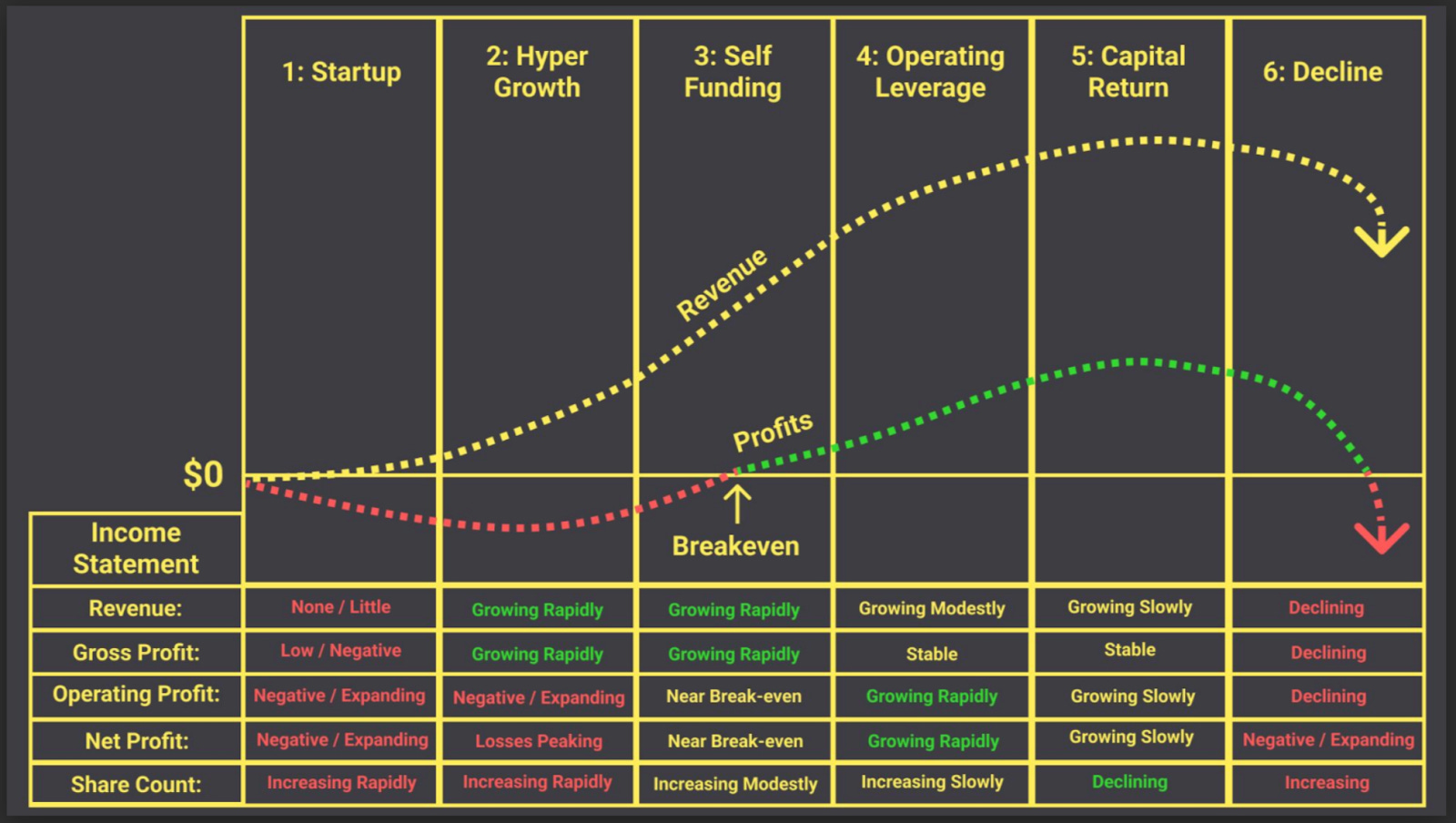

To assess the fair value of Hims & Hers, it is critical to adopt the appropriate valuation approach, which will be informed by the company's stage of business growth and maturity. Reference to Brian Feroldi's Business Growth Cycle and Valuation Method diagrams proves beneficial in this regard, helping to pinpoint the most suitable valuation metrics for a company like Hims & Hers, which is still in a growth phase and not yet fully matured.

Hims & Hers is positioned at the beginning of its 'Self-Funding' stage, characterized by its strategic focus on revenue growth and improved gross margins, concurrently approaching profitability. For companies in this phase, the Price to Gross Profit (P/GP) emerges as the most pertinent valuation metric. This ratio, which bridges the Price to Sales and Price to Earnings metrics, is particularly useful here. It factors in gross margins, unlike Price to Sales, and is applicable before a company has stabilized its net margins, which is a prerequisite for Price to Earnings evaluations.

The Price to Gross Profit ratio offers a lens through which to compare a company's market price with its gross profit, thereby gauging if the stock is undervalued or overvalued based on its gross earnings. A lower P/GP ratio indicates a potentially undervalued company.

In calculating "Price", one can either use market capitalization (MC), derived from the outstanding shares multiplied by the share price, or opt for Enterprise Value (EV), which provides a more comprehensive valuation. EV sums up the company's total worth, incorporating market capitalization with debt and subtracting any cash and cash equivalents. The rationale for favoring EV over MC is that it presents a truer reflection of a company's total value, accounting for debt and cash balances.

With a current Enterprise Value of $1.17 billion and a trailing twelve-month gross profit of $570 million, Hims & Hers has an EV/GP ratio of 2.06. This ratio positions the company as significantly undervalued, especially when considering its growth trajectory, boasting a compound annual growth rate (CAGR) exceeding 70% since IPO.

For a clearer perspective on the company's market standing, I have compiled a comparative analysis featuring similar growth-oriented stocks and their respective P/GP ratios. This comparison underscores the compelling valuation of Hims & Hers in the current market.

For the Enterprise Value (EV) of Hims & Hers, I referred to data from YCharts, and for the trailing twelve-month (TTM) gross profit, figures from Stock Analysis were used. Additionally, the most recent year-over-year (YoY) revenue growth data was extracted directly from the companies' earnings reports.

The list I compiled primarily includes companies that are at a growth stage akin to Hims & Hers, where the focus is on driving revenue growth and enhancing gross margins. Among these, only a select few, such as Palantir, Crowdstrike, MercadoLibre, and Nu Bank, have achieved GAAP profitability.

Upon examining the average Price to Gross Profit (EV/GP) ratio for these companies, excluding Hims & Hers, it stands at 16.8. This figure implies that Hims & Hers, with its EV/GP ratio of 2.06, appears substantially undervalued—by a factor of approximately 8.15. However, given the potential overvaluation of some listed companies and the risks previously discussed, a more conservative estimate would suggest that Hims & Hers is undervalued by a factor of ~5.

This underscores a significant potential for share price appreciation. If Hims & Hers can sustain a Compound Annual Growth Rate (CAGR) of 20% over the next decade, its business could expand sixfold. Should the market then apply a more equitable valuation multiple of 4 to 5 times, shareholders could witness a share price escalation of up to 30 times the current value. Conversely, if Hims & Hers maintains a more aggressive CAGR of 30% and its valuation aligns with the fair market value, the stock could soar up to 70 times its current price, without factoring in potential share dilution.

These projections are not overly optimistic considering the company’s established growth trajectory and its substantial opportunities across various verticals. Hims & Hers has room to grow by venturing into new geographical regions, broadening its reach in healthcare segments, and enhancing its product offerings. Additionally, market valuations tend to fluctuate with overall market moods. Many of the companies in my previous list experienced EV/GP ratios ranging from 50 to 100 during the bullish years of 2020 and 2021.

It is within the realm of possibility that Hims & Hers could see its valuation multiple expand by up to 10 times over during the next 10 to 15 years, coupled with a five to tenfold increase in business operations reflecting a modest CAGR of approximately 15 to 20%. This could potentially translate to a 50 to 100 times increase in the current share price. Projecting forward, this would elevate the company's market capitalization to around $130 billion. Considering the expected expansion of the money supply, a $130 billion market cap in 10 to 15 years could effectively be the equivalent of today's $80 to $100 billion market cap size.

While the aforementioned projections represent an optimistic scenario for Hims & Hers, the company's prospects appear promising. Boasting a management team replete with top-tier talent, an attractive business model evidenced by strong consumer adoption and impressive revenue growth, and guided by a visionary founder and CEO, the company is well-positioned for success. The inherent flexibility and optionality of their business strategy provides a multitude of pathways for expansion and innovation.

As long as Hims & Hers continues its excellent track record in business execution, the outlook is bright. The current share price suggests that the company is undervalued by approximately a factor of ~5, hinting at substantial return potential for investors. Assuming Hims & Hers maintains its trajectory, shareholders stand to gain significant rewards in the future.

Addition from Brent:

I hope you enjoyed Agrippa’s first contributor article and we would very much appreciate your support by liking and sharing this article.

Furthermore, If you have any questions, do not hesitate to reach out in the comment section below or hit us up on X.

If you want to read more of our work, make sure to subscribe for free by clicking the button below!

If you want to read more about HIMS, make sure to take a look at my article as well!

Disclosure: I/we have a stock, option or similar derivative position in some of the companies mentioned, and might add to our positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

Well done 👏🏻

Great study of a stock I like! Let’s hope tomorrow for great results and great fcf