Duolingo: Language Learning the Fun Way

Duolingo Analysis

Introduction

Duolingo is a stellar growth story, which once again exceeded expectations with its Q4 earnings report from a while ago. Duolingo is a global leader in the online language learning industry, offering an attractive interactive platform that makes learning a new language easy and accesible.

While investors were calling the stock expensive over the last year Duolingo’s (DUOL) stock soared higher and is up over 60% over the last year. This shows that a company with strong growth and fabulous execution is sometimes worth the premium valuation.

In this article, we will take a deeper look at Duolingo’s Q4 earnings and the company as a whole. In addition, what can we expect in 2024?

Before we get started, make sure to subscribe by using the button below to receive more in-depth content like this completely free in your inbox.

So without further ado, let’s take a look at the numbers!

The Numbers

Q4 2023 revenue came in at $151 million, up 45.4% year-over-year, beating estimates by $2.62 million. The year-over-year growth is the best it has been throughout the year. As such, we could say this was a fabulous quarter. The exceptional performance this quarter was due to a continued acceleration in user growth and the better-than-expected performance of Duolingo’s New Year’s promotion.

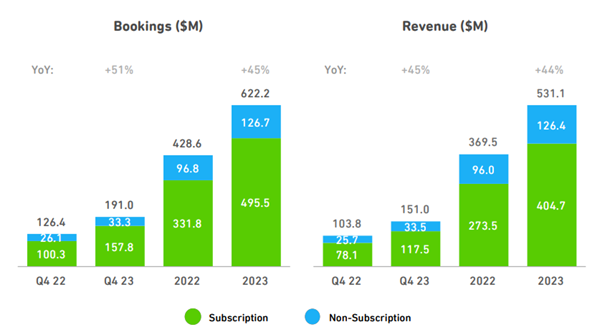

Both revenue and bookings came in at record highs in Q4 2023, total bookings reached 191 million composed of 157.8 million subscribers and 33.3 million free users, in total an increase of 51% year-over-year.

Revenue was up 45% year-over-year, reaching $151 million in Q4 2023. With $117.5 million in subscriber revenue and $33.5 million in non-subscriber revenue.

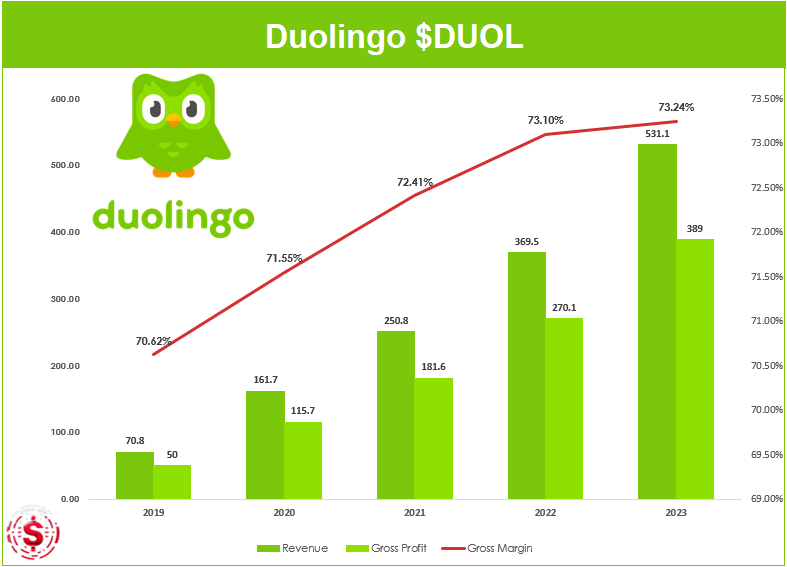

When we look at the full year, revenue was up 44% year-over-year, with revenue reaching $531.1 million. Subscriber revenue was $404.7 million over the last year, accounting for 76.2% of the total revenue.

Bookings reached $622.2 million in 2023, up from $428.6 million or an increase of 45% year-over-year. In conclusion, we can say that Duolingo continues to grow at a rapid rate and has been able to justify its ‘expensive’ valuation tag that people gave it in 2022.

When we look at the GAAP EPS, Duolingo achieved a GAAP EPS of $0.26, beating the consensus by $0.10. An interesting note is that EBITDA came in at $7.2M this quarter.

This is the first time EBITDA was positive in Duolingo’s history. A very positive sign for investors and this might put the stock on more people’s radars, as positive EBITDA is a must for a lot of investors.

When looking at adjusted EBITDA, which has been positive for a while, we can see that it has been growing rapidly. More importantly, the adjusted EBITDA margin is 17.6%. The reason adjusted EBITDA has been higher throughout the year is Duolingo’s changed focus on cost-cutting and using capital more efficiently. As can be seen in the chart below, adjusted EBITDA is up $78.2M year-over-year, this increase was driven by revenue growth and efficient cost-cutting measures, as mentioned above.

The gross profit for the year came in at $110.4 million for the quarter, equating to a gross profit margin of 73.1% in Q4 2023, 0.1% lower than Q4 2022. This is not a great sign, but we could argue this is more or less stable. In addition, a gross margin of 73.1% shows the strong pricing power Duolingo has.

Year-over-year, gross profit reached $389 million, up from $270.1 million in 2022. This translates to a gross profit margin of 73.2%, an increase of 0.15% year-over-year. The year-over-year increase was mainly driven by higher margins on the English Test and the higher subscription margin compared to last year.

This is a sign of the high pricing power, Duolingo has been able to increase its pricing without losing customers. This is a perfect scenario for investors like ourselves, which shows the potential moat Duolingo has.

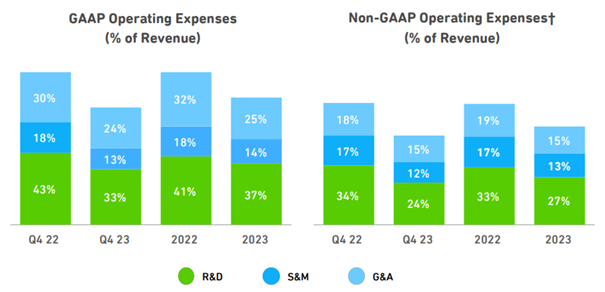

A negative is the lower efficiency of the advertising, which is shown by the lower advertising gross margin. Just a quick refresher on what the chart below shows. The chart below shows the % of revenue that Duolingo spends on different expense factors. R&D stands for Research and development, S&M stands for Sales and marketing, and G&A stands for General and administrative.

Important to look at with Duolingo is the stock-based compensation, also known as SBC. In Q4 2023 stock-based compensation was $27.3M, the full year 2023 stock-based compensation was just shy of $100M. 1/4th of the SBC during Q4 2023 was related to the long-term equity awards meant for the pre-IPO founders, these are meant as the only equity awards for the founding shareholders till 2031.

Why is this important you might ask? These awards are related to the stock price. The total dilution of shares includes the management incentives. This means that if the stock doesn’t perform well, there will be less dilution. As such, some healthy dilution would be good to see in the next few years as this would mean that Duolingo’s stock price has soared, which is what we love to see as shareholders after all.

Now let’s move forward to the free cash flow, or what I like to call the real “profit”. Free cash flow is the money the company can use to reinvest in its business, buy back shares, and so on. Free cash flow for 2023 reached $144.3 million, which is an increase of 3.12x year-over-year or 312%. The free cash flow has been improving every quarter for the last year. This shows that the management is executing well and that its cost-cutting measures are working.

Other vital numbers for companies like Duolingo are DAUs and MAUs, daily active users, and monthly active users. For platforms like Netflix (NFLX), Meta Platforms (META), Snapchat (SNAP), and Duolingo DAUs and MAUs are probably the most important numbers to watch. If there is one thing you don’t want to see as an investor it is a decrease in DAUs and MAUs as this might mean that a platform is becoming less relevant.

Don’t worry, both numbers were up significantly.

The DAUs reached 26.9 million in Q4 of 2023, up 65% year-over-year. This is an even bigger increase than last year, last year DAUs grew 61.3% year-over-year. The MAUs were up 46% year-over-year to 88.4 million.

Something we love to see is that the year-over-year growth in DAUs is higher than the year-over-year growth in MAUs, this indicates that Duolingo has been successful in activating its monthly users and turning them into daily users. This is exactly what we like to see as investors.

You might ask, why are DAUs so important? First of all, daily users are more likely to subscribe to Duolingo’s premium version., Super Duolingo. Secondly, the more activity there is on the app, the more ad revenue Duolingo makes.

You could see that effect in subscriptions indeed. They increased from 4.2 million in Q4 2022, to 6.6 million in Q4 2023, up 57% year-over-year.

Earlier in this article we talked about the higher margins on the English test. Well, this brings us to Duolingo’s third income stream, next to advertisements and subscriptions. While this isn’t a significant source of revenue its revenues are up 29% year-over-year. Another source of revenue is the In-App purchases, which increased $3.1 million to $8.9 million, up 52% year-over-year.

Below you can find the table with all the revenue information in if you want to take a look yourself.

Something that I want to address is the significant revenue growth Duolingo continues to attain. This was the most prominent bearish argument just 2 years ago. During the pandemic, Duolingo saw a strong increase in users and people expected this to slow down significantly once the pandemic was over. Well, it is fair to say that Duolingo has been able to prove everyone wrong. The company continues to execute and DAUs and MAUs are growing even faster than last year.

Guidance

If we look at the guidance for Q1 2024 and the full year 2024 guidance, we can see that Duolingo is guiding for another impressive year. The company is guiding for revenues to come in between $717.5 million and $729.5 million, this is an increase of 35-37% year-over-year.

For Q1 2024, the company expects revenue to come in between $164 million and $167 million, indicating year-over-year growth between 42%-44%. The consensus revenue estimate from analysts is $727.72 million for the full year 2024.

Furthermore, the company is also expecting an adjusted EBITDA Margin of 21.5% to 23.5% throughout the year, this translates to an expected adjusted EBITDA of $154.3 million to $171.4 million. Fantastic numbers, not much more we can say about that.

Something that I want to address is that a lot of growth for Duolingo simply comes from word-of-mouth advertising, which means that this doesn’t cost Duolingo anything. This shows the strength and the superiority Duolingo has compared to other language learning platforms. Duolingo as a brand is becoming a real stamp on the younger generations.

Something else worth noting is that the company is still making impressive moves toward its long-term profit target. CFO Matt Skaruppa mentioned the following during the earnings call.

“We'll continue to make progress towards our long-term profit target. We expect to add an additional 500 basis points of adjusted EBITDA margin this year to reach 22.5% at the midpoint. Our adjusted EBITDA margin will vary a bit quarter-to-quarter given our bookings and hiring seasonality. Specifically, we expect adjusted EBITDA margin for Q2 to be lower than Q1, Q3 to be about the same as Q1, and Q4 to be the highest.

For the full year we are targeting an incremental margin at or slightly above our long-term adjusted EBITDA margin target of 35%. This year we expect to achieve our adjusted EBITDA margin expansion by getting operating leverage across all three cost categories of non-GAAP OpEx.”

Another important question from analyst Zach Morrissey from Wolfe regarding why the management remains confident that the strong user growth numbers remain sustainable in the future. CEO Luis von Ahn gave the following answer.

“The majority of our growth comes from just making our product better. I mean it's mainly word of mouth and because of that it's actually quite predictable. I mean it's not perfectly predictable, it is quite predictable because we just know that our product just keeps getting better and better. So, we expect that to be the case in this -- throughout this year.

We're, of course, very proud of the fact that for 10 quarters in a row we accelerated the user growth. And that's what's kind of surprising that we just -- we always kept on thinking well maybe this is -- we're going to kind of not accelerate user growth anymore, but we did that for 10 quarters in a row.

And this time around, we expect kind of mid-50s going forward. And part of the thing that also helps us feel comfortable about this is we just have so much more of a TAM. I mean we're -- there's about two billion people in the world learning a foreign language. We have close to but slightly under 100 million MAU. So, there's just a lot more room to grow. So, we feel pretty good about that.”

The key takeaways from this statement are:

● Making our product better

● Much more TAM

Duolingo’s focus on continuously making their products better is where the focus is at. This is what separates the good companies from the great companies. Duolingo isn’t focused on just driving revenue by growing at whatever the cost. No, they want to make the product better and let the product speak for itself through word-of-mouth advertising.

Secondly, the Total Addressable Market ((TAM)) for Duolingo is simply immense. After all, everyone who wants to learn a foreign language is part of Duolingo’s addressable market.

Furthermore, Duolingo expects strong top-line performance throughout the financial year 2024. Mainly driven by rapid user growth and continuous improvements in the conversion of free users to paid subscribers. One way Duolingo wants to do this is by helping users select the best subscription plan for their needs. While this is still in a test phase, this is a good improvement in my opinion. In the end, customer satisfaction is very important and only possible when they are on the right subscription plan.

Personal Insights and Earnings Call

While I was doing my research for this write-up I decided to use Duolingo myself. I’ve always been interested in Duolingo as an investment, but never used the actual product myself. I have to say I’ve been enjoying it over the last few weeks and doing much more than what is needed to just keep my “streak”. Hopefully, I’ll be able to speak some basic Spanish soon.

This brings us to this paragraph, the most important driver for future growth is Duolingo's great free product, which they continue to further improve. If you haven't used it yet and want to learn a new language casually, I think you should.

Furthermore, a great free product is the best marketing strategy a company can have. The great free product is the reason that Duolingo has so much organic user growth. In addition, the more a free user uses the platform, the more likely he is to eventually get a subscription

Another crucial factor that could affect Duolingo is its ability to integrate artificial intelligence into its products. CEO Luis von Ahn mentioned the following during the earnings call regarding AI used for cost-cutting and reducing headcount.

“We did reduce our contractor force but this was not like full-time employee layoffs or anything like that. And yes, probably the biggest reason for the reduction of the contractor force was the use of AI. I mean we are -- wherever we can in the company, we -- if something can be done by AI, we're going to take the opportunity.

The places where we're using AI, there's kind of two big places. One is just in our content creation. And we're just -- not only are we reducing costs there, but probably even more importantly, we're able to do things a lot faster. And what's good about that is, it also allows us to experiment faster.”

An example of such an experiment is the roll-out of DuoRadio. DuoRadio requires a lot of data generation. Von Ahn mentioned that this would have been an impossible project in the past as it would have cost the company over 10 years to generate that data. Now, with the use of artificial intelligence, they can do it in a few months. According to von Ahn, artificial intelligence is useful as it accelerates the development of new products and helps improve current products.

Furthermore, Duolingo is also focusing on improving retention rate and increasing their platform lifetime value ((LTV)). Duolingo has been doing this by putting more resources behind the family plan, which according to their data has a higher retention rate and as such increases the LTV. Currently, the family plan is 18% of the subscriber base.

Additionally, Duolingo is also focusing on making investments to further drive long-term growth. CEO Luis von Ahn said the following during the earnings call.

“We will also make additional strategic investments to drive long-term growth. We will continue developing advanced content for English learners who make up the largest part of our addressable market. We will also continue to develop our math and music courses by expanding their content and making them even more fun engaging and effective for learners of all ages.

Last year we reached an incredible milestone. Our learners completed their 100 billionth lesson. Perhaps even more impressive is that we have about 90% share of global online language learning MAUs. And yet we still see so much more potential and opportunity ahead of us. There are hundreds of millions of language, math, and music learners out there who have yet to sign up for Duolingo, and we're working on winning them over.”

100 billionth lessen, that’s quite the milestone if you ask me. Even more impressive is the 90% global market share the company has. Duolingo has a monopoly on the online language learning market and for now, I don’t see any direct competitor in sight. The CEO even mentions that Duolingo is just getting started. This shows the ambition he has to grow Duolingo into a language-learning behemoth.

For more insights about the company’s products I highly recommend checking out the initial articles from Kris and his earnings review from last year. Addressing all the products would make this article too long and they simply deserve an article on their own.

Conclusion

Duolingo had another fabulous quarter and year. The company continues to grow at a rapid pace and further improves its products, including AI integration.

Duolingo posted strong full-year guidance. In addition, the business is debt-free, which is something you don’t often see with rapidly growing companies like Duolingo. Accompanied by its large addressable market and strong management execution, Duolingo is setting itself up for exponential growth for years to come.

While Duolingo already has a market cap of $10 billion, the multi-bagger potential is still there with the potential Duolingo has. Especially, with all the potential innovations that are still possible in the years to come, like artificial intelligence being integrated further into its products or finding ways to convert even a higher percentage of free users to subscription plans.

The only reasoning to be cautious could be valuation, other than that, this is a fabulous business with strong growth potential

That was it for the Duolingo Earnings analysis. Leave a like and comment below if you enjoyed this post. Sharing with your friends, colleagues, and family is much appreciated!

I fully agree with your optimism. Great company (at a sporty price). Here’s my take on it:https://open.substack.com/pub/hightechinvesting/p/duolingo-stock-whats-next-for-2023s