CSV Carriage Services, Inc. ($CSV) Death is knocking at Profit's doors

"In the Spotlight" CSV Carriage Services, Inc.

In this “In the Spotlight” we will be discussing CSV Carriage Services, Inc. ($CSV). This is another one that will be written in cooperation with Jacob Rowe from Burry Edge a good friend of ours. He is an individual specialised in “Deep Value” Opportunities.

Intro

< For our Halloween celebration piece, we figured that Carriage Services would be a great choice (just kidding it was coincidence.) >But today’s choice features the topic of death services including, burials, cremations, and all other funeral services. We believe that analyzing this company with a top-down approach will be the best way to approach this company.

The Numbers

CSV has a decent revenue 3-year annual growth rate of 15%.

CSV has a decent ROIC of 23%, indicating that each $100 invested in the business results in an additional $23 of operating income.

CSV has a decent gross margin of 33%, indicating that it has strong pricing power.

CSV has a solid FCF of 15%, which indicates that the company could buy itself back in about 8 years.

Forward PE: At the current valuation CSV has a forward PE of 11.15.

Starting from the Top

First of all, we would like to begin with the macroeconomic perspective for the company. We will take a look at some of the headwinds that carriage will be facing in the coming days.

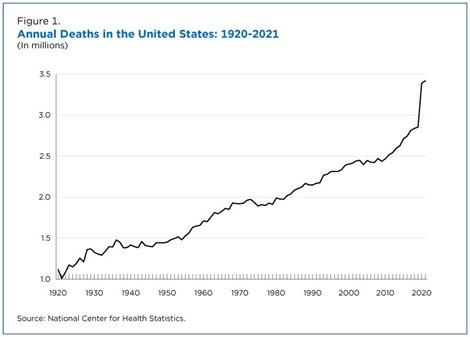

The first consequential trend is death rates. Since covid, I am sure you can imagine that death rates did in fact increase, and this will lead to an impact on topline revenue in the short run (there is already an impact, and it is mild in our opinion). Below you can see the obvious increase in death rates from covid and the flatlining post covid.

Clearly, there has been a large increase in deaths each year. We believe this trend will most likely continue through the next decade. Mainly due to the fact that the baby boomer population ages further and Americans continue to get much older. Below is the forecast for a 48% increase in older Americans over the next 20 years.

As you can understand, this has large implications for the industry. We believe this will allow for long term growth over the coming decades. This isn’t insane growth (a CAGR of about 2%) but, this will help push the industry along. It is definitely a bullish outlook for the industry as whole.

Due to the fact that an aging population means a higher number of deaths over the coming decades, with the death rate pre-covid flatlining around 79 years old (showing no signs of improvement). So, love it or hate it, this is the reality that the death services industry is facing in the coming decades.

Cremations are in demand

This obviously is a good thing for the company, but, probably not good for the cremated.

For years, analysts and investors have been worried about the effect of cremations on the profits of death services companies and that is still a worry today. This would be a significant headwind but, we have great news for any would be investors, just check out the charts below and you tell us if you notice an impact.

Clearly revenues have increased (along with EBITDA) for years, so I don’t think there’s too much to worry about! My mindset is along the lines of the CEO, and that’s if they aren’t feeling any impacts with cremations being 57% of the market then I think the future bodes well. This ability to maintain growth is due to amazing acquisitions and good management, which is the overall theme of this company. In addition, it doesn’t hurt that gross margins are even higher on cremations.

A Little History

Carriage services has gone a long way in its 30 years of service. Ran by the same CEO, who is now 78, for those 30 years, they have experienced a wealth of change that has led them to become the high functioning company that they are today.

In the 90s, the company almost went under like most companies in the industry due to overleveraging their way to massive growth. After that debacle the company had to try to fix the disaster, they had formed. They were able to do this in the following 7 years.

How you may ask? By getting rid of waste, deleveraging and focusing on cash flow they were able to become a decent company in the mid-2000s and that’s when this CEO really turned this company into what they are today.

Growth By Acquisition

In this paragraph, we will be discussing the growth by acquisition of the company and we will be discussing the competition.

After the downfall, the CEO/Founder began to decentralize the company. He shredded middle management, then proceeded to focus and raise his standards for the quality of managers that he would have at the localized level. After finding top notch local managers he was able to push more responsibility at a local level and allow these great managers to be more agile and adjust to the local needs. This corresponded to the company’s strategy of growth through acquisition, by utilizing these great managers to increase margins. The next goal was developing a strong strategy of buying great companies that had strong upside potential. Starting in 2010 they began to build a new system of buying companies and these are still roughly the standards they operate with today.

Clearly, they look for price, but all these other standards they have created ensures that they are able to get great companies for a great price. Now, you might be thinking that they could run out of businesses to buy. But, according to carriage services the market is only getting better, as most of the industry is privately owned (and family). Furthermore, most owners are aging and are willing to sell their companies for cheap to a consolidator that will treat it well.

Their only public competitor, which grows in a similar fashion, is SCI. SCI operates similarly but at a much larger scale than what carriage services operates and is the industry’s biggest player. Overall, the companies only control less than 20% of the total market and this leads to plenty of room for both companies to grow so competition is not a problem from an acquisition standpoint for the foreseeable future.

When CSV acquires new companies, they immediately increase profitability and margins to get the most value out of their acquisitions. The company’s ability to allow their motivated and elite localized management systems to independently (and effectively) operate has enabled this great margin expansion in new acquisitions. Surprisingly, great managers, when left to their own vices, are great at managing things! This is why their decentralized approach is so important to future growth.

See the chart below for how well they do (same store implies a store that they have had for at least 5 years):

Management and Capital Allocation

If you look at this company, there is no inherent moat, just like every other company in the industry. What carriage does have is a great CEO and a great management team who is ready to take the reins when he leaves.

If you read his letters, it is exactly the type of CEO that is written about in the book “The Outsiders”. He is constantly trying to innovate separately from his competitors and run a streamlined decentralized company. His ability to hop on cheap debt and turn that into value for shareholders cannot be praised enough as he has done throughout the last 20 years. We expect a clean transfer of power as he is already allowing other managers to control meetings and company direction with a hands-off approach, which sets up an easy transfer later to mitigate risk when he leaves.

They operate on a 5-year plan that is updated every 5 years to achieve their goals. This has been the case since 2005 and will most likely continue into future years. Their current strategy for capital allocation can be found in the listed points below:

Acquiring a company that meets the standards of the list I shared before (they are planning on acquiring 2 companies this quarter)

Debt Reduction (this is a current focus)

If an adequate company is not available, then buying back shares is a preferred method.

Share prices must be 10% below their estimated intrinsic value of the company (which is currently $75 a share). They have retired 20% of dilutive shares since Q2 2021 (their 4th time buying back shares)

Management rarely holds boatloads of cash and is constantly looking for ways to allocate it. They also run a trust which operates at roughly the same amount of returns the last 10 years as the S&P 500.

This will most likely improve through a downturn and could lead to an increase in their balance sheet. Management operates at beautiful ROIC’s, the first half of this year they operated at a 20% ROIC. This is consistent with what this management has been able to produce historically. Their FCF margins are simply incredible year after year and is due to blatant focus by management to increase and then allocate effectively. In the case their stock crashes due to current macro-economic conditions not pertaining to CSV's business model. We are confident that the company will buy back shares by the truckload. In addition, it should be mentioned that CSV refinanced their $400M in senior notes from May 2026 at 6.625% to May 2029 at 4.25%, which added significant value to the company (I also believe this is how they funded the mass amount of share buybacks).

Insider Purchases

As you can see in the table below, the insiders have been quite active lately. This is good to see and gives even more strength to our thesis. In particular seeing the COO increase his stake by a significant amount is what we like to see.

The Charts

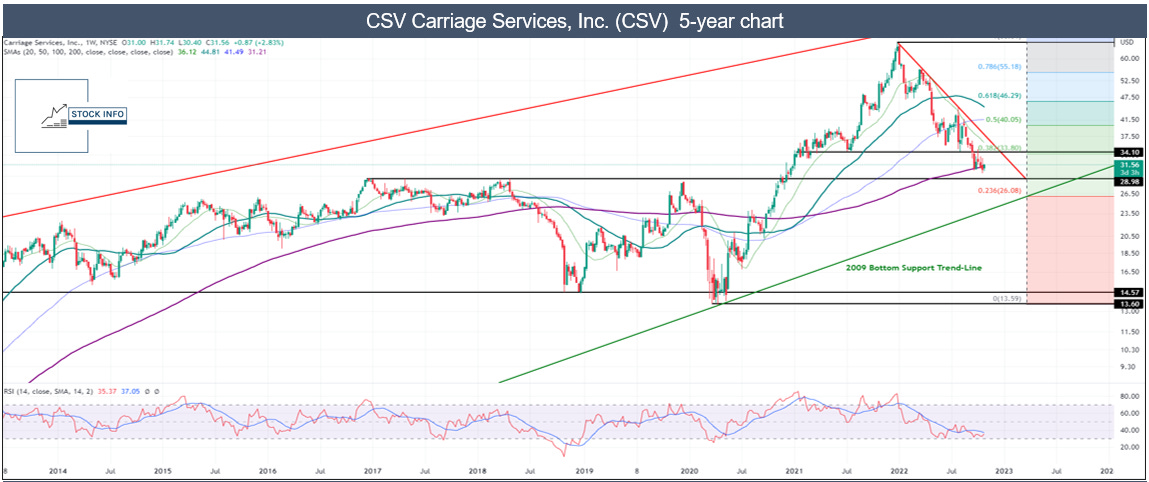

As can be seen on the chart below CSV currently has a YTD bottom around $30. If the market continues to deteriorate, we could see the price drop towards the $29 support level. This would mean more downside is possible.

We can see the stock is falling together with the market as it is currently down close to 52% since its ATH of late December last year. Currently, the stock has found some support on the 200WMA, which you will be able to see in the chart below. Ideally, we would like to see the stock stay above the crucial $29 support level. If that support isn’t able to hold, we could see more downside and CSV would become an increasingly attractive opportunity. We believe the stock provides a very enticing buy opportunity on every dip below $30.

Now let’s have a look at the long-term chart. We can clearly see the stock is having a rough time. The stock has fallen close to 52% since its all-time high, as we mentioned above.

CSV does have a strong business as we discussed in this article. We believe the company is poised to grow further. Although, the company might struggle due to current macro-economic headwinds, we believe this is a strong company is one to keep an eye on for the long-term. As you can see, the stock found some support on the 200WSMA as we already mentioned above. In addition, we got the up trending green support line, which should act as a very strong support level. We would like the stock to break above the current $84 resistance level. Afterwards, we would like to see the stock break out of its steep downtrend that it has been in since last year.

Valuation and Expectations

To conclude this article, we would like to talk a little bit more about the valuations and expectations that we have for CSV.

CSV’s growth was expected to slouch this past quarter as they had stated, they increased overhead to update their facilities and technology, since they needed to modernize everything. This was a planned event, but the market still seems to have missed the memo and they immediately fell off drastically.

We believe this creates one of the best opportunities in the market to get an undervalued company for an absolute steal. They are currently priced at $31.45 a share after undergoing some macroeconomic headwinds with covid ending, higher interest rates leading to a lower market, and a rougher than expected 2nd quarter/ I agree with management, and I get a value of about $72/share using a DCF with 15% CAGR and a 5% discount rate.

Furthermore, I expect that to be realized as revenue settles out over the next couple of quarters. They might not seem cheap with an 11x EV/EBIT but I believe due to numerous factors including being in an industry that is not heavily impacted by recessions along with second to none management, this company deserves a much higher stock price. If we take this management and the pretty stable industry into consideration, we don’t think we have to project any major impact from a large recession for this business. Taking this into consideration, we get a high multiple and a 50%+ margin of safety on a consistent business with consistent returns.

To us, that sounds pretty good. We believe that below $30 it is definitely a stock to keep an eye on.

Thanks for reading this in the Spotlight! Special thanks to our co-writer @Burryedge We will be doing more articles with other talented people soon. We hope you enjoyed it. Feel free to leave a comment below or contact us. Make sure to check out our twitter account by clicking HERE, that way you won’t miss out when we release a new article. Click here to check out our other articles HERE.

Disclosure: We (Stock Info) have no stock, option or similar derivative position in the companies mentioned, and we have no intention to buy or sell within the next 72 hours. Our co-writer for this article Mr. Jacob Rowe does already have a position.

I/we wrote this article ourselves, and it expresses our own opinion. I/we are not receiving compensation for it. This article shouldn’t be seen as investment advice as I/we are no financial advisors. I/we have no business relationship with any company whose stock is mentioned in this article.

Insiders have been buying even more this month. Both purchases were informative.