Crocs Inc. ($CROX) just an ugly shoe or a great investment?

Crocs Inc. ($CROX) just an ugly shoe or a great investment?

"In The Spotlight" Crocs

In this “In The Spotlight” we will be discussing Crocs Inc. ($CROX).

Intro

Crocs Inc. is an iconic brand, which could become a long-term winner.

Crocs is a company that has gained some attention over the last 2 years. CROX significantly improved its business as covid tailwinds made the stock price soar. From 2020 bottom to 2021 top, the company gained over 2000%.

Has CROX become a better business over the last 2 years?

As of now, the HEYDUDE acquisition seems to be a good acquisition, the initial returns are promising.

All these questions and much more will be discussed below.

The Numbers

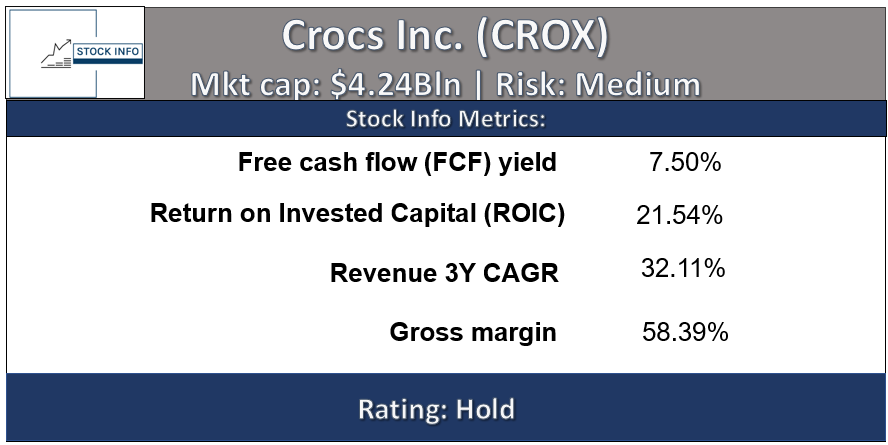

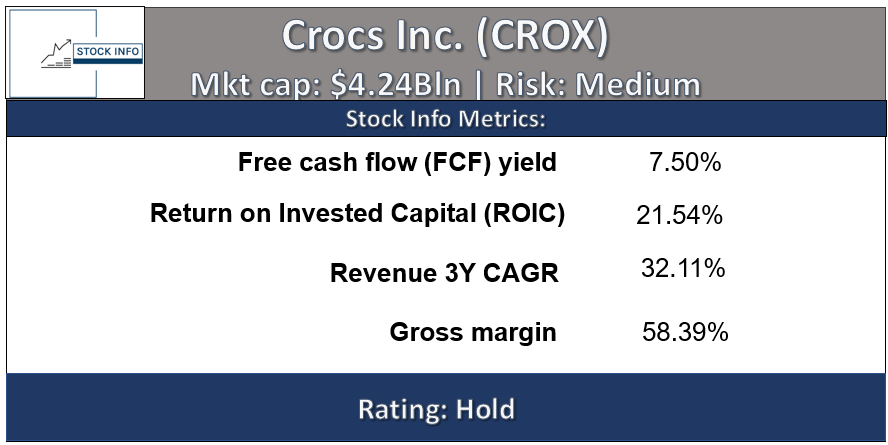

CROX has a strong revenue 3-year annual growth rate of 32.11%. This strong growth rate is partially fueled by Covid-19 tailwinds.

CROX has a solid ROIC of 21.54%, indicating that each $100 invested in the business results in an additional $21.54 of operating income. In the past this was higher due to Covid-19 tailwinds.

CROX has an excellent gross margin of 58.39%, indicating that it has very strong pricing power.

CROX has a solid FCF of 7.50%, which indicates that the company could buy itself back in about 14 years.

Forward PE: At the current valuation CROX has a forward PE of 6.64. This is low when we compare this with their competitors. Skechers ($SKX) has a forward PE of 12.54, which is almost double.

When we take everything into consideration, we believe CROX is currently a hold. They have excellent pricing power in addition to a strong 3Y CAGR. We are looking forward to the upcoming earnings to see how CROX performs in difficult times. In the TA aspect at the bottom of the article, we will go more in depth on interesting pricing points.

The Growth Story

Crocs is an iconic lifestyle footwear brand founded in 2002. Crocs is growing rapidly around the world. In addition, they are expanding their product lines. CROX has been able to position itself as a niche brand with style as well as comfort.

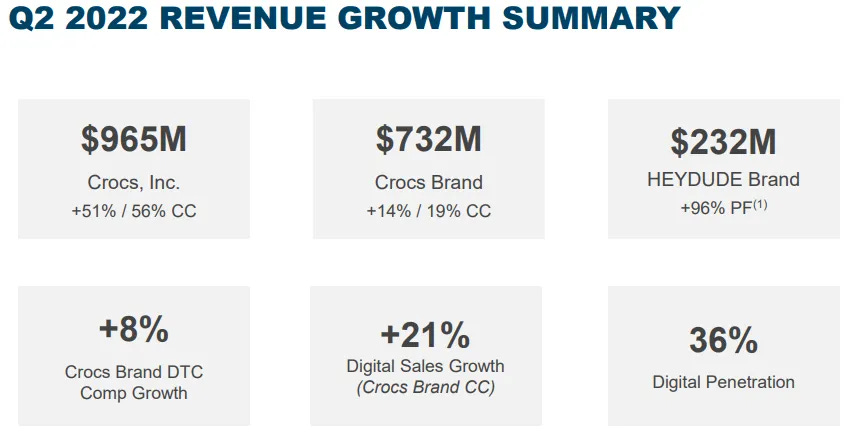

Crocs growth has remained strong over the last quarter with top line growth of 19%. This is very impressive as sales continued to grow while the broader footwear market remained stagnant.

Furthermore, the acquisition of HEYDUDE at the end of last year seems to be an excellent strategic move. HEYDUDE exceeded expectations and brought in in $232M in sales.

Weaknesses

Recession will crush consumer spending. One of the biggest fears for CROX shareholders should be a recession. As we mentioned in our Starbucks article (check it out by clicking HERE). As families are starting to struggle due to significant price increases across the board, mostly in food and energy prices, people might decide to cut spending on leisure wear shoes like Crocs.

In addition to the above, Crocs is a consumer discretionary company, which historically get hit quite significantly in an economic downturn. The management has addressed this issue and has decreased its short-term revenue expectations.

Cost of HEYDUDE acquisition, Crocs used a substantial amount of cash to fund the HEYDUDE acquisition ($2bln), which causes the balance sheet to be in a slightly worse state compared to other competitors. The company is nowhere near to financial distress, but as investors we should pay attention to their debt level and debt servicing expenses going forward, especially in the current macro-economic environment.

Consumer taste is fast changing. The fashion industry has a tendency to quickly change taste. Crocs' "ugly-chic" design is appealing to a wide range of customers across the world at this point. However, if the company fails to read the fashion trends correctly in the future, the company's growth will be at risk. Therefore, investors should pay close attention to their quarterly numbers and market trends.

Strengths

Brand name. Crocs has become a house hold name. Everyone knows the “ugly” shoe and a lot of people swear by it. Furthermore, it is particular popular with Gen Z and millennials.

Loyal customers. Crocs has very loyal customers. The design and comfort are loved by its customers, which might make CROX a stronger than average consumer discretionary company than others. In addition, CROX aren’t that expensive. Although, this might be the case, we believe rampant inflation in addition to decreasing consumer spending will affect Crocs business so we aren’t convinced this is a valid reason as of now.

Cheap, if we would only take PE into consideration Crocs is trading at historically low valuations. Crocs has a forward PE of 6.64 at the moment of writing, which is cheap. We do expect earnings to decrease in the upcoming quarters due to tough macro-economic conditions.

Sector Outlook: We believe the market for shoes will continue to grow, and fashion accessory market will expand alongside with it. The growth won't be explosive like some in the tech industry, but it will trend steadily with population growth and overall economic growth.

Photo by ALEXANDRA TORRO on Unsplash

Management and Insider Buying

Crocs seems to have an excellent management team. Its CEO and director Andrew Rees has more than 25 years of experience in the footwear and retail industry. Furthermore, we have Rick Blackshaw who is EVP and Brand President for HEYDUDE, which is an important division of Crocs Inc. They both have plenty of experience within the industry.

The rest of the board are all people with prior experience within the industry. As of now, the integration of HEYDUDE seems to work quite well.

It is interesting to note that the prior significant drop back in May and June saw insiders buying shares. This shows that the management has confidence in the future of the company. We would like to see some more insider buying activity if the stock revisits these levels. This would show great strength and confidence.

The Charts

As can be seen on the chart below CROX currently has a YTD bottom around the $45.95 level. This is an important support to watch. If the market continues to deteriorate, we could see the price drop below this level. This would mean more downside is possible. We would be looking towards $30 as a significant support. If it gets really ugly and we could see covid-19 bottoms.

We can see the stock clearly is having a rough time. At the moment of writing the stock is down 64% since its all-time high back in November of 2021. Last week we clearly rejected an important resistance the Top before the GFC, which is indicated by the purple line. Ideally, we would like to see the green trendline hold, this could be a good support level, but as of now this is uncertain. Currently, we are sitting at a potential support level. It would be an indication of strength if CROX is able to stay above this $66 level. We believe the stock is a decent buy below $50. The $46 support level would be an interesting point if the stock holds that level.

Now let’s have a look at the long-term chart. We can clearly see the stock is having a rough time. The stock has fallen 64% since its all-time high, as we mentioned above. The 2007 top to 2008 bottom saw a decline of almost 99%. Fortunately, it is unlikely that this scenario repeats itself as CROX has significantly improved as a business. We believe the stock market as a whole isn’t out of the woods yet. Although, we could see some significant bear market rallies, we wouldn’t be surprised if the market heads lower/ sideways for a while.

On the downside we believe the $28.65 level and the green trendline support (Support since GFC bottom) are attractive buying opportunities. If the company is able to withstand the current macro-economic headwinds, these levels could be generational buying opportunities. On the upside, the red trendline resistance could be very significant for the upcoming months. A break above would be a bullish signal. We believe the purple resistance line is one to watch as well as this level has been rejected multiple times before and has proven to be a tough nut to crack.

Conclusion

We believe CROX is a solid business with an excellent management team. The fashion industry is difficult as trends change quickly. For the future of CROX it will thus be crucial that the management is capable to see these upcoming trends quickly and capitalize on them. In addition, inflation and decreasing consumer spending are significant headwinds for the company. Furthermore, the company has strong competition from brands like Nike, Adidas and Sketchers to name a few. Although, CROX is a niche brand and might not suffer as much from competition as we think. We believe Crocs is a very solid brand with a loyal following. We believe the stock could see more downside in the short-term, but if management is able to execute and the recession will be less harsh than expected, this investment could pay-off big time earlier than expected. An important thing to keep an eye on is the growth. If CROX is able to keep growing at a fast pace this is a wonderful investment.

Thanks for reading this in the Spotlight! We hope you enjoyed it. Feel free to leave a comment below or contact us. Make sure to check out our twitter account by clicking HERE, that way you won’t miss out when we release a new article. Click here to check out our other articles HERE.

Disclosure: I/we have a stock, option or similar derivative position in some of the companies mentioned.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. This article shouldn’t be seen as investment advice as I/we are no financial advisors. I/we have no business relationship with any company whose stock is mentioned in this article.