Cash Extraction: Taking Profit Without Losing Exposure

Cash Extraction: Taking Profit Without Losing Exposure

Option Education 3

Introduction

Dear readers,

Welcome to this week’s substack post. As many of you know I’m a huge advocate of using option strategies in your portfolio. Why, you might wonder?

Well, options serve a multitude of purposes beyond just leveraging your investments. They can act as protective shields for your positions, hedge against market downturns, facilitate profit-taking without liquidating your holdings, and offer a host of other strategic advantages.

In this article, we'll delve into a specific strategy known as 'cash extraction’

What Is Cash Extraction?

A common dilemma most investors face in their investment career and might be familiar to you is “I bought shares of company XYZ and I’m already up X%. What should I do?” In essence, this quandary boils down to a fundamental question—'Should I continue holding my position, or should I consider selling?

This is precisely where the concept of 'cash extraction' enters the picture.

How does one go about realizing profits while maintaining exposure to potential gains, all while managing risk more effectively? You might be thinking, 'This sounds intriguing, but what's the catch?' The straightforward answer lies in the realm of options, a subject we'll explore in depth in this article.

Most people use certain % points to sell their positions partially. For example:

I sell when I have 50% profit

At +25% I will sell 1/3rd of my position, another 1/3rd at +50%, and the remainder I will sell at +200%.

Or I will sell half at +100%, because the remainder of the shares is “free”

It's perfectly natural to start questioning your position, especially when a stock's price experiences rapid appreciation within a short span of time. The heart of the matter revolves around a dilemma, one driven by the twin forces of fear and hesitation.

On one side, there's the fear of relinquishing unrealized profits, while on the other, there's the fear of missing out on even greater potential gains.

How, then, do we navigate this intricate puzzle and arrive at a solution?

Options!

We solve this problem by using options. In essence, cash extraction involves two straightforward steps

Selling your shares

Buying a call option for each 100 shares you have sold.

This is what we would call a cash extraction. Important to note that in case we want to keep the same exposure one can’t simply buy and sell whatever call they want. Instead, you need to buy a contract with 100 delta for each 100 shares you have sold.

First let’s take a look at what a call option actually is:

A call option is a contract, with each contract representing 100 underlying shares. As the buyer of such a contract, you get the right (but not the obligation) to purchase 100 shares of the underlying asset at a predetermined price and on a specified date. This predetermined price is what we call the “strike price” of the option.

In implementing this cash extraction approach, you effectively part ways with your existing shares (by selling them), while concurrently securing the right to repurchase them in the future.

If you have a limited knowledge of options, I highly recommend reading this article regarding the intrinsic and extrinsic value of options.

Let’s take a look below at an example that might be familiar for a lot of you in recent months Nvidia $NVDA.

Nvidia: How To Extract The Cash

Nvidia has run up significantly over the last few years, as can be seen in the chart below. The stock is up over 800% since its covid-19 bottom in March of 2020, and up over 190% year-to-date. As such, this is the perfect stock to talk about for cash extraction.

The decision regarding which contract(s) we will be buying for the cash extraction boils down to the following principles.

Days till expiration (DTE)

The strike price of the option contract

Liquidity of the option chain

Days Till Expiration

Currently, NVDA shares are valued at $416.10 per share, which equates to a total cost of $41,610 for owning 100 shares. Typically, when undertaking a cash extraction, we opt for LEAPS (Long-Equity-Anticipation-Security) contracts. In simpler terms, these are options contracts with ample time remaining until expiration. While the strategy can be applied with options having shorter timeframes (DTE), it comes with the trade-off of a diminishing 'right to buy shares' over time.

In this example, the liquidity isn’t really an issue as we are talking about a big tech stock. We can see these are liquid due to the pretty tight spread ( difference between bid -and ask price). However, it's worth noting that as we move deeper into or out of the money or select contracts with longer expiration periods, the liquidity of the options tends to diminish.

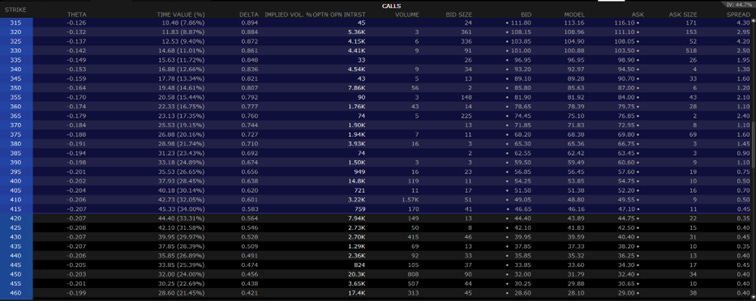

As can be seen below, the bigger the spread and as such, the lower the liquidity, the harder it will to trade these contracts. This is an example for Nvidia for the January 19th, you can see that the spreads for deep ITM options is wider compared to the spreads of the ATM options.

The Strike Price Of The Contract

When deciding on the strike price of the contract, we need to take into account what the price of the contract consists of. This is the so called intrinsic and extrinsic value of the contract, which is crucial to understand before moving forward. We discussed the intrinsic and extrinsic value of options here.

Generally, an options contract comprises two components: intrinsic value and extrinsic value, often referred to as time value. However, either of these values can be zero under certain circumstances. For instance, deep in-the-money options often exhibit zero time value, as demonstrated below.

The crux lies in extrinsic value, as it gradually decays out of the contract, causing a decline in the options contract's price, provided all other factors remain constant. This forms the fundamental principle behind a covered call strategy, where you sell a call option and profit from the extrinsic value dwindling to zero, or at least that's the ideal scenario. For a comprehensive exploration of covered calls, you can find our in-depth article on covered calls here.

It's important to note that time value is most pronounced in options trading at or near the at-the-money (ATM) strike price. As depicted in the chart below, the time value diminishes as we venture further in or out of the money. Once again, this data pertains to Nvidia's options chain with a January 19th expiration date.

The option contracts that are currently ITM can be seen by the purple color they have in the table.

In addition, what you might have noticed is that the price of out of the money options consists completely out of extrinsic value. If this surprises you and you still haven’t read our article about intrinsic and extrinsic value, make sure to do so. You can see that the bid price equals the “time value” for the OTM options.

In the realm of 'cash extraction,' a crucial aspect involves swapping your shares for a relatively 'pricey' call option. The goal is to secure a contract that resides deep in-the-money (ITM) and is not overly laden with 'time value.

‘Time value’ is rather expensive and can decrease very quickly, which we will discuss in another article. Furthermore, you can see a percentage next to the time value number. This is what we call “annualized return”. This is what we will lose in time value if we buy a contract.

In the context of cash extraction, we favor a low or positive annualized return figure. It's worth noting that there exist strategies to mitigate this loss in time value or even capitalize on its decline. However, these strategies, such as transitioning from a call into a bull call spread or employing more advanced option tactics, fall beyond the scope of this article.

How Do We Decide What Contract To Buy?

There are multiple ways to extract cash from a position, but for this article we will keep it simple and look to sell our shares and trade it for one call option for each 100 shares underlying.

But, a crucial point that has to be discussed is delta. What does “Delta mean”? Well, delta is a number between 0 and 1 and if we do this number times 100 it shows how much shares this call option represents at this moment in time.

A deep ITM call option might have a delta of 90, which would indicate that if the underlying stock gains $1, the call would gain $90. But, the price of an option is also influenced by other factors and “delta” isn’t stable either and changes over time. But, delta is a crucial starting point when looking at extracting cash through options.

As such, we could say that 100 shares represent 100 delta, which simplifies the concept a little. It is hard to trade 100 shares for an option with exactly 100 delta as we would always lose some “power”, but the benefit is that we get a lot less capital at risk in return.

Now let’s say we are selling our 100 shares for $420 a share and afterwards we buy a call option. We need to know how this impacts our risk, as we obviously won’t be risking 100x $420 = $42,000 anymore, but solely risk the value of the call option.

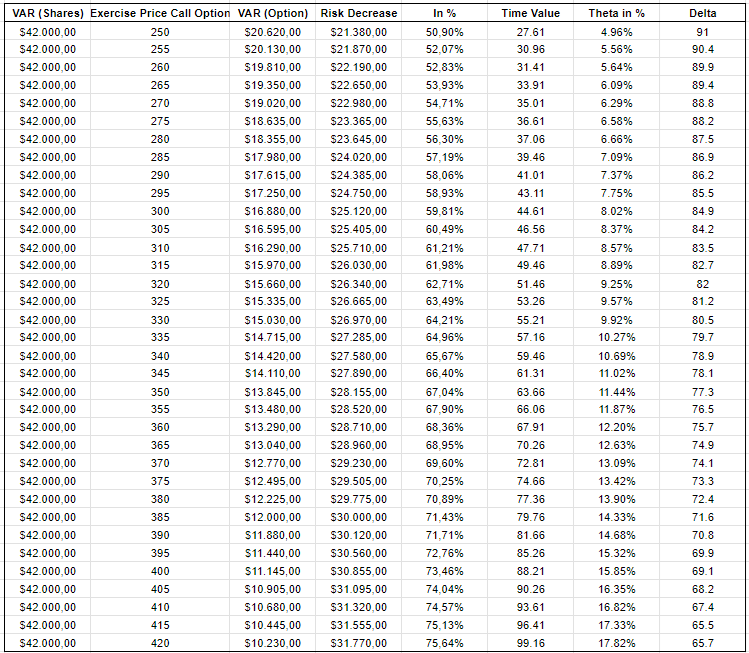

Let’s take a look at all the call contracts starting with strike $250 that are currently ITM. For this we will take a look at the January 2025 calls, which have 479 days till expiration left. Just to be safe, we will take the ask price, but normally when you are buying these contracts you will be paying closer to the “mid” price. Remember, the mid-price is the price in the middle between the “bid” and “ask” price.

In the table below, we will examine these contracts and how this affects our risk. VAR stands for Value-At-Risk, which is how much you are risking when holding this position.

We can see that we can significantly lower the value at risk of our position through the usage of buying ITM calls. As you can see, the risk gets lower the higher the strike price of the option, but the higher the strike price the more theta or time value we are buying. This time value will go out of the contract as we get closer to the expiration date. As such, we would rather buy deep ITM calls for cash extraction compared to ATM calls (which would be more beneficial for trading).

Furthermore, it is crucial to make a decision based on the price of the option, the amount of time value in the option and the days till expiration of the option.

Conclusion

This is a simplification of the process as there are many other factors that have an impact on the price of an options contract. Nonetheless, cash extraction is a beautiful mechanism to lower your value at risk. In addition, you could use this cash that you now have in your account after doing this cash extraction for other positions, which might be more rewarding in the future.

In conclusion, we've explored the concept of cash extraction, a strategy for preserving gains while maintaining exposure to an asset using options. This strategy offers investors a unique way to navigate the classic dilemma of 'Should I hold or should I sell?' by combining the sale of shares with the purchase of (deep) in-the-money call options.

Choosing the right call option hinges on factors like delta, strike price, time value, and days till expiration. These elements collectively determine the risk and potential reward of the cash extraction strategy. While a higher strike price minimizes risk, it also entails a greater time value premium.

Ultimately, understanding these intricacies and optimizing your option choices can help you effectively execute cash extraction, safeguarding your profits while staying in the game.

However, as with any investment strategy, careful consideration and due diligence are paramount to success.

If you enjoyed this post feel free to subscribe and I would appreciate it if you like and share this article with your friends and family!

Let us know what options topic you want me to write about in the future!