BYD: EV Market in a Slump Long Term Thesis Still Intact

BYD: EV Market in a Slump Long Term Thesis Still Intact

BYD 2

Hi everyone! It has been a while since our last Substack post, but here we are again with an article on “Build Your Dreams” $BYD.

Introduction

In the rapidly evolving automotive industry landscape, BYD Company Ltd (BYDDF) has become one of the biggest names. Originating from China, BYD has firmly established itself as a global powerhouse in the electric vehicle ((EV)) and battery market, reflecting the company's commitment to the changing transportation landscape. With an impressive history of car development and battery technology, BYD's contributions have propelled it to the forefront of the car (and EV) market and has played a crucial role in shaping the future of mobility, especially in China.

In our previous coverage of ”Build Your Dreams”, we argued that the company was an exciting investment despite a lagging Chinese economy still recovering from its COVID-19 lockdowns. The thesis has yet to play out quite as we anticipated, but we are starting to see a more active Chinese government in its quest to stimulate the economy.

In addition, we showed how dominant BYD has become in the global EV market, which still rings true. Despite the stock being down significantly since its all-time highs, we still see great potential in owning it for the future.

In this follow-up, we highlight the changes that have occurred for BYD. In addition, we will give an overview of how the Chinese economy has changed since our last piece.

This update comes at a time when the EV market has seen declining demand worldwide due to high interest rates and harsh financial conditions. However, as countries and corporations alike strive to reduce carbon emissions and combat climate change, the demand for innovative and sustainable vehicles is still set to be high.

An Update On The Sleeping Dragon

China's economic landscape for 2024 is evolving under the influence of deliberate monetary policies and structural reforms designed to ignite growth and tackle long-standing hurdles. A critical strategy has been the People's Bank of China's ((PBOC)) reserve cut, aimed at re-igniting the market and helping growth by unlocking a fair amount of capital. This measure is part of a broader commitment to a flexible monetary policy, supporting the pursuit of an ambitious growth target amidst a complex global and domestic economic backdrop.

However, there's a consensus among analysts that more stimuli might be necessary to combat deflationary threats and unemployment issues, given the business sector's tentative stance on workforce expansion. Although China achieved its growth target in 2023, the recovery seems less robust than expected, leading to projections of a slower growth rate in 2024. This anticipated deceleration shows the importance of bolstering domestic demand to balance out production capacity hikes and mitigate deflationary pressures.

Central to China's economic agenda is ongoing policy support and structural reforms emphasized by the World Bank. These reforms are vital for reigniting growth and overcoming structural barriers such as high debt and demographic shifts due to an aging population. Proposed solutions include reforming the fiscal framework and reducing local government financing vehicles (LGFVs) debt to stabilize and invigorate the economy.

The economic path China will follow in 2024 and beyond is expected to depend on how effectively these monetary and structural reforms foster recovery and sustainable growth. Balancing the stimulation of domestic demand, debt management, and external economic challenges will play a crucial role in defining the nation's economic future.

The most pressing issue for the Chinese economy scenario is rising deflationary pressures, which increase real borrowing costs and exacerbate the country's debt situation. The government's cautious response includes moderate policy rate adjustments and hesitancy towards extensive monetary stimulus. However, there's a tilt towards more substantial fiscal support, evidenced by the issuance of an additional RMB 1 trillion in sovereign bonds.

Furthermore, China's economic recovery needs to be more consistent, with 2024 predicted to face considerable obstacles. Political and regulatory uncertainties across different sectors have dampened investor confidence and affected the overall economic climate. In addition, we touched upon some of the difficulties in some recent economic data coming from China in our piece on Alibaba (BABA), which you can read HERE.

In this context, companies like BYD, which are operating within China, must adapt to the shifting economic policies and market conditions. Government initiatives favoring high-tech and green industries could provide opportunities for businesses in the electric vehicle and renewable energy sectors - this is where BYD is set to benefit significantly.

This is why investors should see BYD as a rather long-term hold. These initiatives will take time to materialize and even longer before they show up on BYD’s earnings. However, we expect the current policy path to be a tailwind for BYD.

Further Growth

Recently, BYD unveiled the Yangwang U8 SUV at the Geneva car show. The Yangwang U8 isa car which can also float. While this may just be the car’s “party piece,” it highlights the pioneering stance in automotive innovation and design BYD has taken. The U8 is also a luxury plug-in hybrid SUV, showing BYD is moving into making more luxurious cars than they previously have.

Furthermore, BYD's introduction of the U9 supercar underlines its strong venture into the high-end EV sector. The all-electric Yangwang U9, priced at a starting figure of $233,000, emerges as BYD's most lavish offering to date. It can achieve 0 to 60 mph in less than three seconds, the U9 challenges conventional supercars on performance and puts BYD as a closer competitor to companies like Ferrari (RACE) and Bentley (BSY).

This move diversifies BYD's portfolio into the luxury market, which they have not really touched beforehand. The U9 aims to shift the luxury EV market paradigm, contesting established luxury marques and redefining performance and design standards in the EV landscape.

In addition, BYD is pushing to establish a manufacturing foothold in Europe signifies a critical phase in its international expansion strategy. While details on BYD's European manufacturing plans remain unspecified, its push for a bigger global presence, including new vehicle launches in Mexico is great to see for BYD investors.

A manufacturing base in Europe would streamline logistics, overcome tariff and regulatory hurdles, and tailor BYD's offerings to the continent's preferences and stringent climate objectives, enhancing BYD's stature as a frontrunner in the global electric vehicle domain.

These moves underscore BYD's dynamic strategy in broadening its global footprint and portfolio.

Financials

We covered BYD’s historical topline numbers in our previous piece, and for that reason, we won’t go into too much detail surrounding 2019-2022. It is also worth remembering that BYD is reporting its fourth quarter earnings on March 26th, therefore, we do not yet have the full picture of 2023.

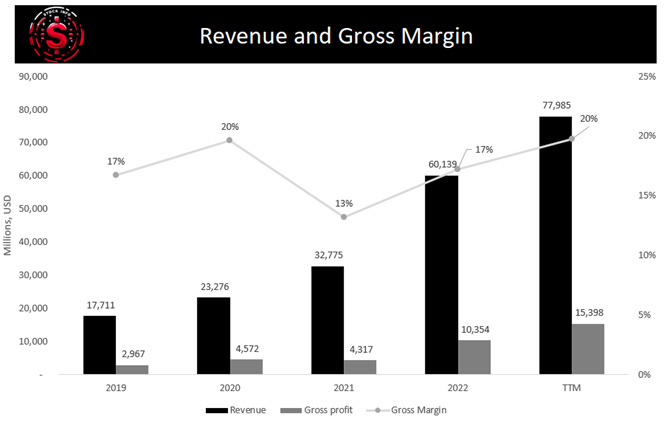

Focusing on the trailing twelve months (TTM), BYD's revenue surged to an impressive $77,985M, showcasing the culmination of consistent and significant growth from its initial $17,711M in 2019. This pattern reflects BYD’s expanding operations and possibly rising demand for its innovative offerings.

During the same TTM period, gross profit also saw a notable increase to $15,398M, indicating ongoing improvement in profitability. Despite this positive trend, the gross profit still lags behind the rapid pace of revenue expansion, suggesting that while sales have increased substantially, the cost of goods sold (COGS) has impacted profit margins. This period emphasizes BYD's financial strength while also highlighting the need for cautious management of costs amidst growing operations.

In addition, BYD's gross margin stabilized at 20%, after a journey that saw initial success at the same level in 2020. This stabilization suggests BYD may have regained control over its cost of goods sold (COGS) or at least optimized its sales mix, despite facing challenges in maintaining profitability due to potential rises in costs or shifts towards less profitable products.

A gross margin of 20% is good compared to other competitors and shows BYD's ability to navigate the complexities of cost management and product strategy to maintain a solid profitability level.

Next, we will look at some more of BYD’s financial metrics since 2019. We have already discussed the gross profit margin and will therefore start with the Sales, General, and Administrative expenses (SG&A) margin. The SG&A margin reflects BYD's rigorous efforts in operational cost management. A significant reduction from 41.08% in 2019 to 31.42% in 2020 highlights initial success in streamlining expenses.

However, the margin experienced an uptick in 2021 to 42.98% before adjusting to a more sustainable level of 35.10% in 2022 and 32.74% in the TTM, further illustrating BYD's ongoing commitment to operational efficiency.

Conversely, the R&D (Research and Development) margin tells a story of steady innovation, with an initial 27.25% in 2019, slightly fluctuating over the years, to settle at 29.11% in the TTM. This constant allocation of revenue to research underscores BYD's dedication to innovation while managing the investment proportion of its revenue.

The narrative of interest margin unfolds a new chapter in BYD's financial strategy, with negligible figures in the early years followed by a noticeable spike to 7.06% over the last twelve months, showing that higher interest rates are causing an uptick in financing costs and debt levels.

The EPS growth showcases theprofitability of BYD. With a remarkable 228.57% surge in 2020, followed by a -26.09% drop in 2021, which primarily highlights the ramifications of the COVID-19 lockdowns. The story takes a positive turn in 2022 with a 388.24% growth, moderating to a 62.65% increase over the last twelve months.

While FY2023 may not end with a three-digit growth in EPS, BYD's financial metrics paint a picture of a company that has successfully navigated through harsh financial conditions in China. The recent uptick in gross margin signals a potentially effective response to previous challenges in production costs or sales strategies, this shows BYD does have pricing power. The swings in SG&A and R&D margins highlight a balancing act between operational efficiency and commitment to innovation, which they have done successfully.

Meanwhile, the interest margin and EPS growth offer a window into BYD's financing approaches and profitability trajectory. Together, these indicators provide a multifaceted view of BYD's financial health and strategic positioning in the face of evolving market dynamics.

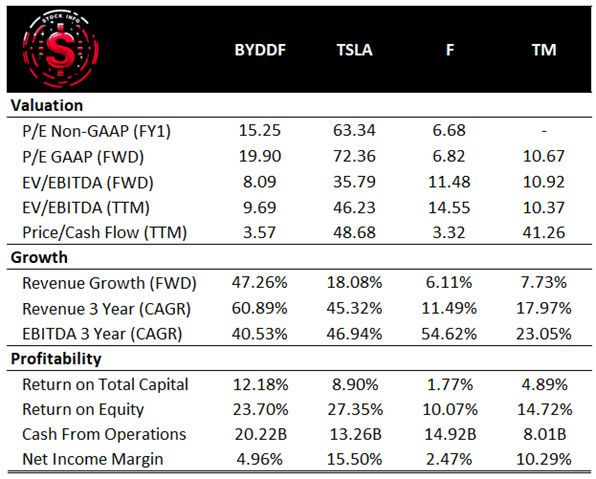

Next, we want to examine how BYD stacks up against its competitors based on various metrics. BYD's valuation metrics are moderate compared to Tesla's but are higher than Ford's and Toyota's.

The forward P/E (Price to Earnings) non-GAAP for the first year (FY1) stands at 15.25, suggesting investors pay $15.25 for every dollar of earnings, which is less speculative than Tesla's ($TSLA) 63.34 but higher than Ford's ($F) 6.68.

The forward P/E and EV/EBITDA (Enterprise Value to Earnings Before Interest, Taxes, Depreciation, and Amortization) ratios are also in the mid-range, indicating a reasonable expectation of future earnings and company value relative to its cash earnings. BYD's Price/Cash Flow ratio is the lowest at 3.57, suggesting its cash flow is robust relative to its stock price.

BYD shows impressive growth metrics. The Revenue Growth (FWD) is at a striking 47.26%, significantly outpacing its peers, which points to aggressive expansion and market penetration. The 3-year Compound Annual Growth Rate (CAGR) for revenue is 60.89%, again the highest among the compared companies, reflecting a solid upward trend over the medium term.

Similarly, the EBITDA 3-Year CAGR is also high at 40.53%, indicating that revenue is increasing and EBITDA is following along rather nicely.

BYD's profitability ratios provide a mixed perspective. The Return on Total Capital ((ROTC)) at 12.18% is the highest among the compared companies, implying effective utilization of its capital. The Return on Equity ((ROE)) is a robust 23.70%, second only to Tesla, showing that shareholders are getting a good return on their investment.

Cash From Operations is a notable 20.22B, indicating healthy operational efficiency. However, the Net Income Margin is relatively low at 4.96%, less than Tesla and Toyota (TM) but higher than Ford, which is a relatively big drawdown for BYD and something we want to see improve.

Conclusion and Investment Outlook

Despite the market's current challenges, BYD stands out for its strong foundation and vision for the future. They're pushing the envelope with new technology and expanding their reach, all while keeping an eye on sustainability.

Think of BYD as a trailblazer in the electric vehicle scene with a clear plan for a greener future. Their history and future plans are a testament to resilience and innovation, marking them as a key player to watch as we move towards a more sustainable world.

As mentioned earlier, BYDDF is not a stock you buy to hold in the short term. Investors should consider BYD a long-term hold as the economic and sustainability theses play out over the next few years.

We believe it is a great time to add BYD to your long-term portfolio at current price levels. We therefore rate the stock as a buy.

Thanks for reading!

If you like this post, make sure to follow us and share this as much as possible. This motivates us to keep writing these posts.

If you have any suggestions on stocks you want to see a write-up on, feel free to leave a comment or contact us on X.