Alibaba: The Unloved Treasure

Alibaba: The Unloved Treasure

China Discount Justified?

Introduction

In the bustling realm of e-commerce, Alibaba stands as a towering behemoth, a testament to innovation and entrepreneurial spirit. From its humble beginnings as a small online marketplace, Alibaba has transformed into a global force, revolutionizing the way businesses and consumers interact. With its vast network of platforms, including Taobao, Tmall, and AliExpress, Alibaba has established itself as the undisputed leader in China's e-commerce landscape. But its reach extends far beyond the borders of its home country, with a burgeoning presence in international markets that span the globe.

As Alibaba continues its relentless ascent, investors are taking keen notice. The company's stellar financial performance, coupled with its ambitious expansion plans, has propelled its stock to dizzying heights. Yet, that came to an end when Jack Ma came under the radar of the CCP and the Ant Group IPO remained halted. Can Alibaba reverse its momentum in the face of intensifying scrutiny and competition? Will its foray into new markets prove fruitful? And, perhaps most importantly, can the company navigate the complex regulatory landscape in which it operates?

Delving into the intricacies of Alibaba's business model, this article will unravel the factors that have fueled its remarkable success. We will explore the company's strategic positioning, its competitive advantages, and its potential for future growth. Along the way, we will address the challenges and uncertainties that lie ahead, offering investors a comprehensive assessment of Alibaba's investment potential. Further, we take you through a discounted cash flow model and illustrate Alibaba’s underlying value.

The Alibaba Ecosystem

Alibaba Group is a Chinese multinational conglomerate founded in 1999 by Jack Ma inside his own apartment, which has become one of world’s largest e-commerce and most valuable technology companies worldwide. It is headquartered in Hangzhou, Zhejiang, China, also known as ‘The House of Silk’.

Alibaba Group operates in various segments. The first segment we will discuss is the China commerce. This segment is by far the largest and most profitable business Alibaba has. Therefore, it is of utmost importance to fully understand what is behind it. China commerce exists out of two massive businesses: Taobao and Tmall.

Taobao is a Chinese online shopping website like Amazon, where consumers and small businesses can buy/sell a wide range of products. Tmall, also known as Taobao Mall, is a premium version of Taobao that focuses on connecting larger businesses and brands with consumers. It provides a platform for businesses to set up official online stores. Two other important businesses in the China commerce are Xianyu and 阿里1688. Xianyu is used goods e-commerce platform and 阿里1688 serves the Chinese domestic market and is focused on wholesale transactions. Another under the radar platform is Alimama. Alimama is Alibaba’s digital marketing platform driven by data and AI tech, that drives advertising sales on the ecosystem.

Over the last years, Alibaba has been seeking to expand their presence on the global market with their international commerce. Although international commerce is not yet profitable, the company is narrowing losses, and this segment should soon help increase the bottom line of the business. International commerce exists out of a lot of businesses, but four have a major appearance globally, and those are: Alibaba.com, AliExpress, Lazada and Trendyol.

Alibaba.com serves as a global platform connecting businesses from around the world. Alibaba.com facilitates business-to-business (B2B) trade by connecting manufacturers, wholesalers, and suppliers with buyers internationally. AliExpress connects Chinese sellers with buyers from around the world, offering a wide range of products at competitive prices. Similar to Taobao, AliExpress primarily serves individual consumers and small businesses.

Lazada is another e-commerce business with the largest part of their customers in Southeast Asia. On the other hand, Trendyol is an e-commerce platform based in Turkey

he third segment is the local services and probably the worst performing business in terms of profitability. The local services include: Ele.me and Amap. Ele.me is Alibaba's online delivery platform, connecting users with food and beverages, groceries, flowers, and pharmaceutical products. Ele.me focuses on efficient last-mile delivery to ensure that orders reach customers quickly and fresh.

Amap provides a range of location-based services, including digital maps, navigation, real-time traffic information, location-based search, and location-based advertising. Amap's data and services can be integrated into other Alibaba services such as e-commerce platforms, ride-hailing apps...

Next, we have the logistics and supply chain segment, which plays a crucial role in the Alibaba ecosystem. Cainiao network is Alibaba's logistics and delivery network. It works to improve the efficiency of the company's supply chain and provides logistics services to Alibaba and its affiliated companies.

Cloud intelligence group has been one of the most anticipated segments of Alibaba in the past years. Alibaba Cloud, also known as Aliyun, is the cloud computing arm of Alibaba Group. It offers a comprehensive suite of global cloud computing services, including computing power, data storage, and databases.

Digital Media and Entertainment is the last segment with Youku Tudou and Alibaba pictures reporting under it. Alibaba acquired Youku Tudou, a leading Chinese online streaming platform, to enhance its presence in the digital entertainment industry. Youku Tudou is often referred to as the "YouTube of China. Further, Alibaba pictures focuses on film production, distribution, and entertainment-related investments.

The other businesses, not included in the reported segments, are Sun Art, Freshippo, Alibaba Health, Lingxi Games, Intime, Intelligent Information Platform, Fliggy and other businesses.

While Ant Group was initially a subsidiary of Alibaba, it operates independently and is not wholly owned by Alibaba (33% stake). It's known for Alipay and other financial services, including wealth management, micro-loans, and insurance. Ant Group has been in the spotlight for its fintech innovations. Alibaba's third-party online payment platform, Alipay, is one of the largest digital payment platforms in the world and provides a payment system to the Alibaba’s ecosystem.

Alibaba's ecosystem and vertical integration will make it operationally efficient in the following ways:

Data sharing and integration: Alibaba's various businesses share data with each other, which allows them to better understand their customers and provide them with more personalized products and services. For example, Ele.me can use data from Taobao to recommend products to customers based on their past purchases.

Cross-selling and upselling: Alibaba's businesses can cross-sell and upsell each other's products and services. For example, a Taobao customer who purchases a new phone may be offered a discount on Ele.me food delivery.

Supply chain optimization: Alibaba's logistics and supply chain businesses can optimize the company's supply chain, which can reduce costs and improve delivery times. For example, Cainiao Network can use data from Ele.me to optimize delivery routes for food delivery.

Economies of scale: Alibaba's large size allows it to achieve economies of scale, which can reduce costs and improve profitability. For example, Alibaba can negotiate better deals with suppliers because of its large purchasing power.

Overall, Alibaba's ecosystem and vertical integration will help to maintain its competitive advantage.

A Move Towards Efficiencies and Sustainable Growth

In November 2020, the landslide of Alibaba’s stock price began as negative news kept downward pressure high. Everyone was waiting for the $37 billion IPO of the Ant Group, however the IPO got suspended last minute as Chinese regulators started tightening regulations that disqualify Ant from listing. A few days earlier, Jack Ma made remarks on the old-fashioned banking system, which was not perceived as a positive by the Chinese government and this might have been the catalyst for increased scrutiny.

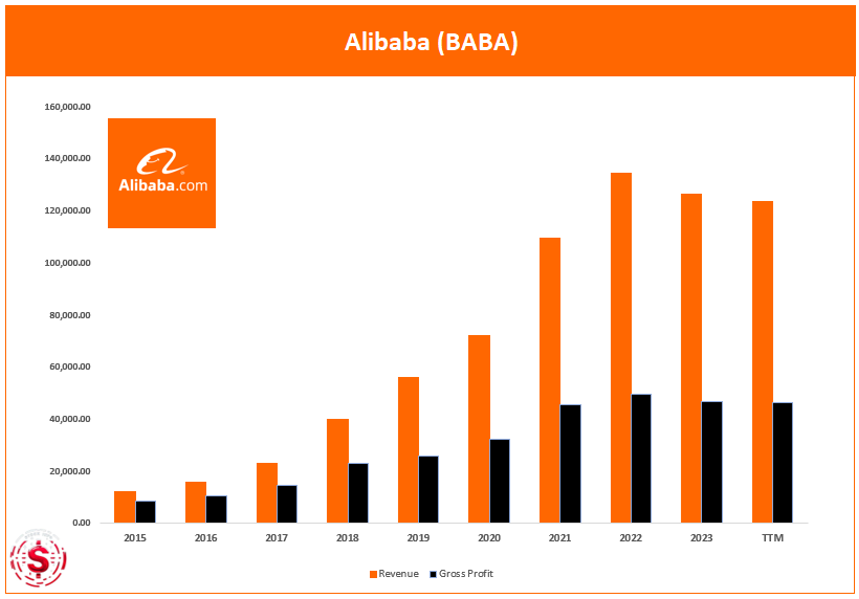

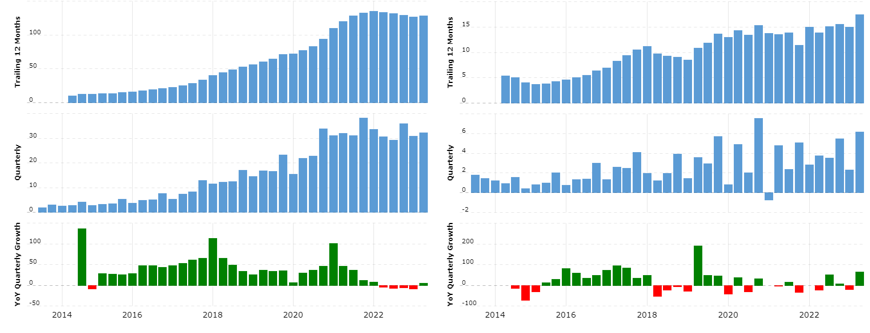

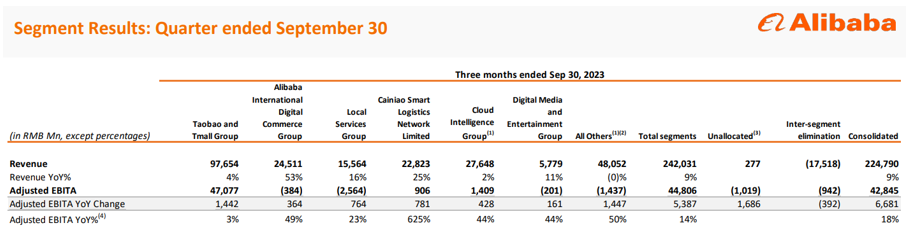

After Alibaba got hit by a $2.8 billion antitrust fine in 2021, for abusing its market dominance, the company has shifted from aggressive growth to sustainable and profitable growth. In the left illustration, it is visible that revenue growth slowed down to a standstill. However, in the right illustration we can see EDITDA has kept growing at a steady pace. This occurrence will also be reflected in the latest results.

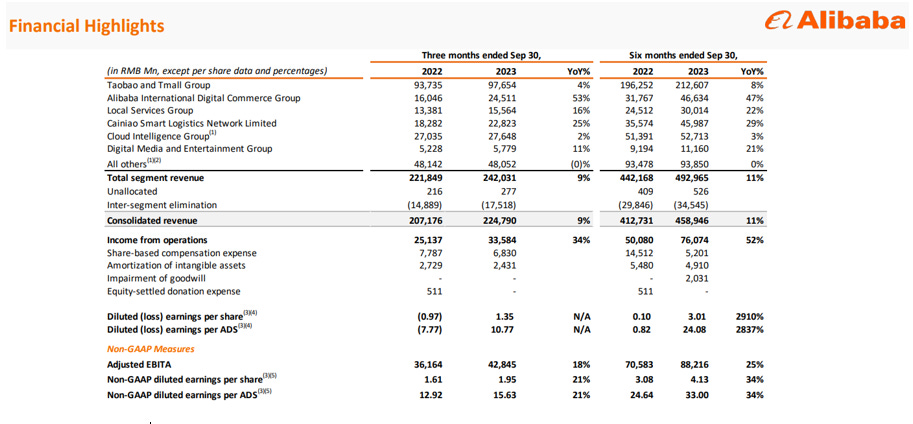

In September, Alibaba reported earnings with a solid revenue growth of 9%. Of course, we need to take this in perspective and compare it to the slow growth of 2022, which might make the 9% less significant. Nonetheless, income from operations grew by 34%, adjusted EBITA increased 18% and non-GAAP EPS by 21%. This showcases the focus on efficiencies and sustainability inside of the gigantic ecosystem.

Despite a lack luster quarter for the China commerce segment and the cloud intelligence group (also mainly China), international digital commerce did perform very well with growth of 53%. Another positive is the fact that Alibaba’s revenue mix is spreading out more globally and therefore the geographic risk of a mainly Chinese business is decreasing.

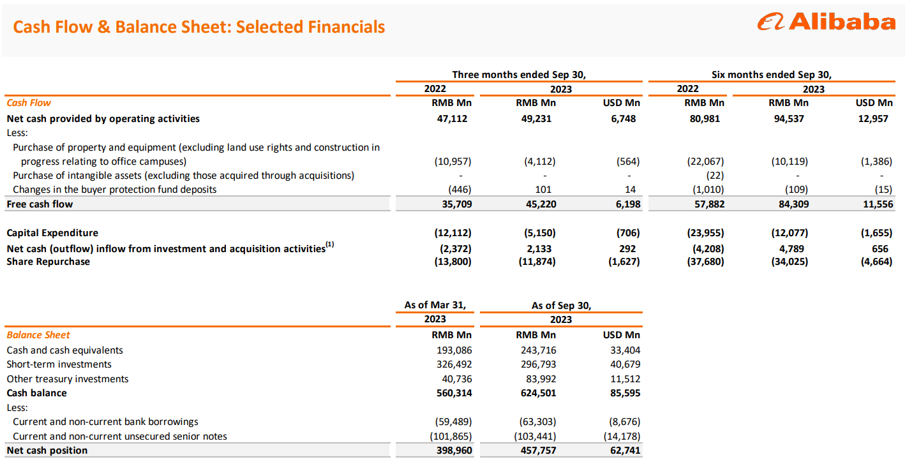

More importantly, free cash flow outpaced EPS and EBITA growth, and increased by 26.6%. Free cash flow is everything the company generates that turns into cash after paying the expenses for operating and maintaining its assets. The free cash flow can be used to re-invest into the business, pay down debt, buy back shares or pay out a dividend. We will later discuss how Alibaba can optimize their capital allocation to unluck value.

In addition, Alibaba’s balance sheet is growing at a significant pace. Although the company had to pay fines and donated a lot of money and supplies worldwide to help fight the COVID-19 outbreak, it didn’t effect the balance sheet in any shape or form. As of September 2023, Alibaba holds $85.6 billion in cash and short term investments, which accounts for 45% of the market capitalization. If we exclude the short term borrowings, the net cash position is equal to $62.7 billion or 33.3% of the market cap. And that is really impressive.

As we already know, the efficiency of profitability increased, but it is great to have an overview of the performance of the separate segments. The fact that there will soon be five segments contributing to the bottom line is exciting. The International commerce group increased EBITA 49%, and I expect the business to be profitable for the first time in the last quarter of 2023. Further, the digital media and entertainment group is also nearing the breakeven point. Alibaba’s logistics arm has been optimized the most in terms of profitability and is now the third largest contributor to the bottom line.

While the cloud revenue growth did not cheer up investors, the EBITA improvements are not irrelevant either. We know that Alibaba has been struggling to get their hands on the latest Nvidia chip technology, which will result in fierce competition outside of China. In the latest earnings report, management mentioned:

“In October 2023, the United States expanded its export control rules to further restrict the export to China of advanced computing chips and semiconductor manufacturing equipment. We believe that these new restrictions may materially and adversely affect Cloud Intelligence Group’s ability to offer products and services and to perform under existing contracts, thereby negatively affecting our results of operations and financial condition. These new restrictions may also affect our businesses more generally by limiting our ability to upgrade our technological capabilities.”

Therefore, the IPO of the cloud unit is also temporarily halted. Important to note is that the cloud market in China is still increasing at a fast pace and is likely running behind the United States. So, I would not write Alibaba’s cloud unit off just yet. Alibaba cloud is China’s main cloud player and is likely to get more demand sooner or later as China’s economy is back in full gears.

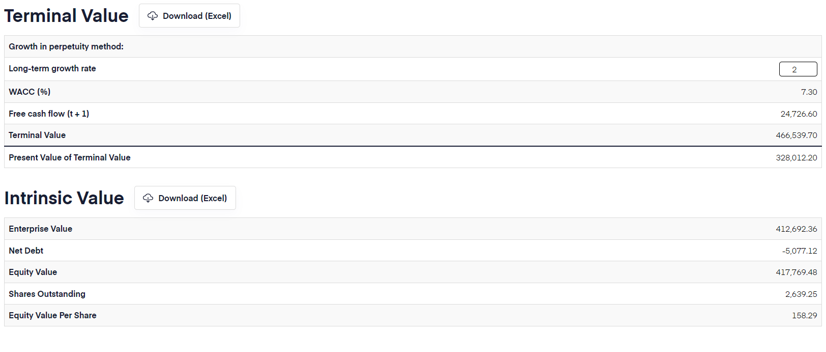

Discounted Free Cash Flow Model

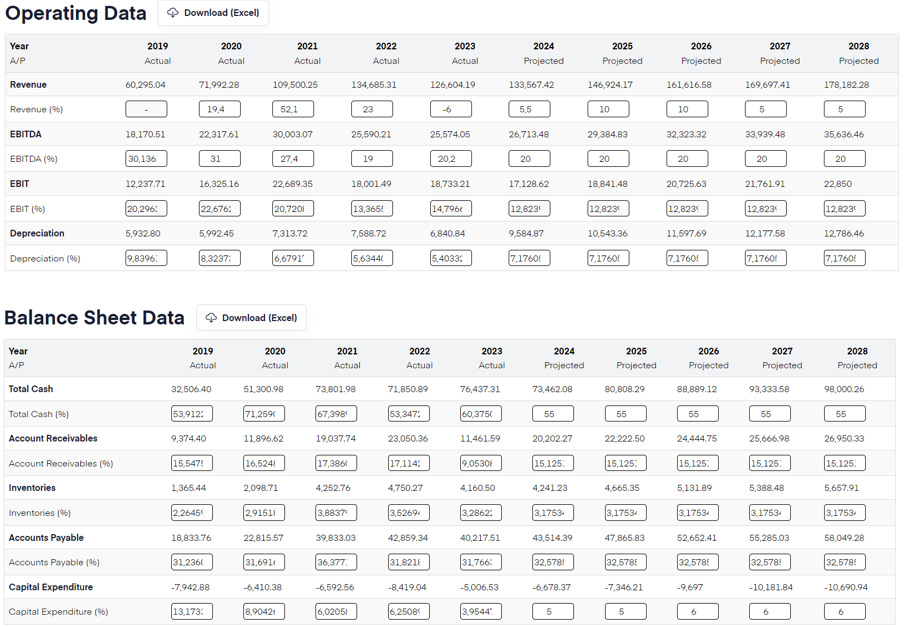

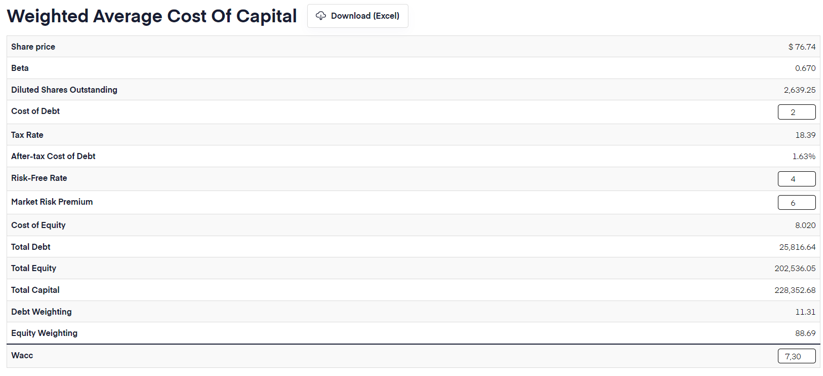

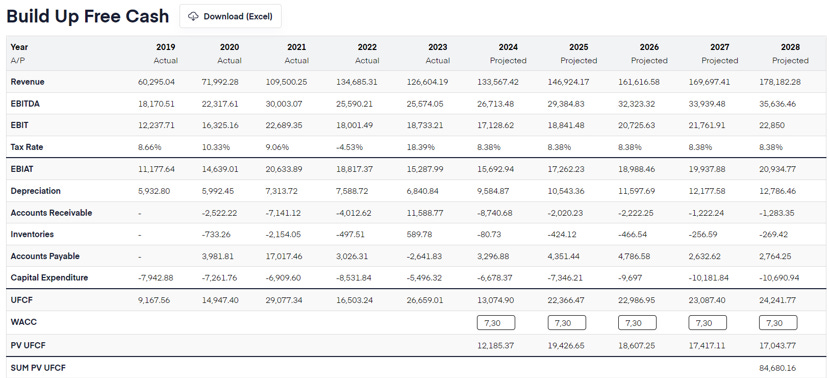

To showcase Alibaba intrinsic value, I ran a discounted cash flow model. Even though I used relatively conservative assumptions, the upside potential is incredible. The assumptions I used for the revenue growth were the analyst estimates for 2024, 10% growth for 2025-2026, 5% growth for 2027-2028 and a terminal growth rate of 2% (equal to average inflation). To discount the future cash flows into the present, I used a WACC of 7.3%, with an expected return for shareholders of 10% annually. If you want to try out your own assumptions, you can use the financial modeling prep website.

Assumptions:

1. Revenue growth:

Used analyst estimated revenue for 2024

Years 2-3 10% growth

Years 4-5 5% growth

Terminal Growth Rate 2%

2. Discount Rate (WACC):

Cost of debt 2%

Risk free rate 4%

Market risk premium 6%

WACC of 7.3%

Given that the current price of Alibaba is $74, the market is valuing the company at a significant discount to its intrinsic value. This suggests that there may be an opportunity for investors to buy Alibaba shares at a price below its intrinsic value. If investors believe that Alibaba's long-term growth rate will be higher than 2% or that its WACC will be lower than 7.3%, then the company's terminal value would be higher, and its shares could be even more undervalued. Nevertheless, we are still dealing with a Chinese company listed in the United States, therefore investors should remain conservative in their assumptions. The estimated upside on Alibaba shares, if the assumptions are right, is 114%.

Deep Value and How To Unlock It

The key factor for investors is obviously making money. Yet, that has not been an easy task since the stock is trading below its IPO price. Investors could have sold their shares for 3x their money in 2021, but that would still not have reflected the fundamental improvement. There are three important ways to receive value from a stock. Stock price appreciation, share buybacks (which will lead to forced price appreciation) and dividends (cash payout). A fourth way to unluck value is by spinning off parts of the business.

Clearly, stock price appreciation caused by the buying of investors itself is not working. And there is one main reason. Not just geopolitical reasons. Alibaba’s largest investor, Softbank, has been selling shares repeatedly in the last two years. Softbank is going from a 24% stake to 3.8% if all the prepaid forward contracts expire. The good news is that this can’t keep going forever and is likely to end in 2024.

The second way to push up the share price is by buying back shares. The company will decrease the shares outstanding, and this will result in more value per share. The best time to repurchase shares is when they are undervalued, because it will be less expensive, more shares can be bought back and will lead to less dividend that has to be paid out, the company can indirectly increase their EPS, and it is a tax-efficient way to return value to shareholders.

Considering that Alibaba is currently priced as one of the cheapest e-commerce businesses worldwide, it seems like a great time to be buying back shares. Also, good to notice is that not all Chinese stocks are treated equally, for example Pinduoduo is surprisingly trading like an American technology business, regardless of the same geopolitical risks.

Alibaba is actively reducing shares outstanding and repurchased $1.7 billion in shares (0.9% of market cap). Under the current share buyback program, $14.6 billion is left for repurchases (7.8% of market cap). A lot of people have been saying that buybacks are ineffective. This is partly correct if there is also a massive seller involved also known as Softbank.

In the last quarter, Alibaba reported a dividend for the first time ever. It is not a one-time only dividend, but it will rather be reviewed on an annual basis. The current dividend is $1 per ADS and represents a 1.35% dividend yield at $74 a share. This is a great initiative to reward shareholders that have been patient in the last two years. Of course, the focus should remain on the buybacks as we are definitely trading below the intrinsic value demonstrated by the DCF model and the basic valuation metrics.

Alibaba is also undertaking the last option to create value: spinning off parts of the business. The logistic business Cainiao is the first to be spun off and has applied for an initial public offering in Hong Kong. But since the initial value of the business is important to shareholders, management must be careful in which market environment they want to do the transaction. Brokers not offering the Hong Kong exchange will need to give cash to shareholders. Therefore, the Freshippo and Cloud Intelligence group spin offs have been temporarily halted, as management want investors to get the value they deserve.

Lastly, the Ant group IPO is likely to still go through after all the restructuring the company has done in the past years. The valuation moved down to $78.54 billion, but it is hard to tell what the business will be worth when the IPO will happen. Since Alibaba still owns 33% of Ant group, the stake is valued at $26 billion or 14% of Alibaba’s value. However, I am confident that we will see a higher valuation than $78.54 billion, because Alipay is one of the largest payment platforms in the world, in comparison Mastercard and Visa are valued between $300-530 billion.

Delisting Risk

However, investors need to keep in mind that Alibaba has been identified by the SEC under the Holding Foreign Companies Accountable Act. This means the company will be delisted by 2024, if they do not show the right auditing under the rules of the United States.

In the annual report of Alibaba, you can find the following positive statement:

“Following that, on December 15, 2022, the PCAOB announced that it was able to secure complete access to inspect and investigate PCAOB-registered public accounting firms headquartered in Chinese mainland and Hong Kong in 2022. The PCAOB vacated its previous 2021 determinations that the PCAOB was unable to inspect or investigate completely registered public accounting firms headquartered in Chinese mainland and Hong Kong. For this reason, we do not expect to be identified as a Commission Identified Issuer following the filing of this annual report.”

The dual listing in Hong Kong lowers the risk of losing money must a delisting ever were to happen. Your shares could be converted into Hong Kong listed shares or you can re-buy your shares at the Hong Kong exchange yourself for a similar price, because the dual listing trades around the same price on the New York and Hong Kong exchange.

Takeaway

Alibaba is a battleground stock with a lot of polarized opinions. Even so, it is almost undeniable that there is a lot of value present in Alibaba. The valuation metrics and the DCF model both reflect that the stock is undervalued. The argument that Chinese stocks will never trade at fair value seems incorrect because Pinduoduo’s valuation tells a different story, more so the stock price is nearing all-time highs.

Alibaba is using all possible methods to increase shareholder value. Although Softbank selling shares is a temporary heavy weight on the stock price, eventually the tide will turn. Once Softbank is done selling, the buybacks will show effect on the stock price and the dividend is great to be paid while waiting.

Alibaba will have more struggles ahead to keep competition at bay, re-accelerate China commerce and the cloud business. Still, the restructuring is going to help streamline the different segments and improve focus on individual challenges.

Analyst downgrades have created more downward pressure in the last weeks and are highly irrelevant. Investors need to keep in mind the incentives of banking analysts and that is buying shares extremely cheap and selling shares extremely high. As a result, they will push prices up or down for their own benefit. Analysts were also saying to sell Meta at $90, Intel at $25, Alphabet at $90 and so on. Focus on your investing process, valuation, and research. That should be your main thesis to buy or sell.

Stock Info: Another great write-up from Friso, I hope you enjoyed it. Make sure to give him a follow on X, he has been posting a lot of great content on there lately.

For more articles regarding thestock market make sure to check us out on Seeking Alpha.

Disclosure: I/we have a beneficial long position in the shares of BABA either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Stock Info). I have no business relationship with any company whose stock is mentioned in this article. I am not a financial advisor. Investing is your own responsibility. I am not accountable for any of your losses.