AbraSilver a must have silver exploration company in a commodity bull cycle

AbraSilver a must have silver exploration company in a commodity bull cycle

"In The Spotlight" Mining Series: AbraSilver Resource Corp.

AbraSilver Resource Corp (TSX.V: ABRA) is one of the biggest undeveloped silver projects in the world. $ABBRF has exploration projects in Argentina and Chile. Their main asset is the 100% owned Diablillos silver and gold project in the Salta province in Argentina. The Company has projects at various stages of exploration, from drill-ready to PEA stage. Furthermore, $ABRA.v is also involved in gold and copper exploration alongside silver.

Intro

Diablillos is a stellar open pit silver project with lots of potential

$ABRA has a strong balance sheet compared to peers

Diablillos has great torque, which provides a lot of upside in an environment with rising silver prices

AbraSilver has a strong and supportive shareholder base with Eric Sprott as biggest shareholder

AbraSilver has projects in fairly safe jurisdictions

Underwhelming performance of the underlying commodities has put pressure on the underlying stocks

Mining costs are rising due to increasing natural gas prices

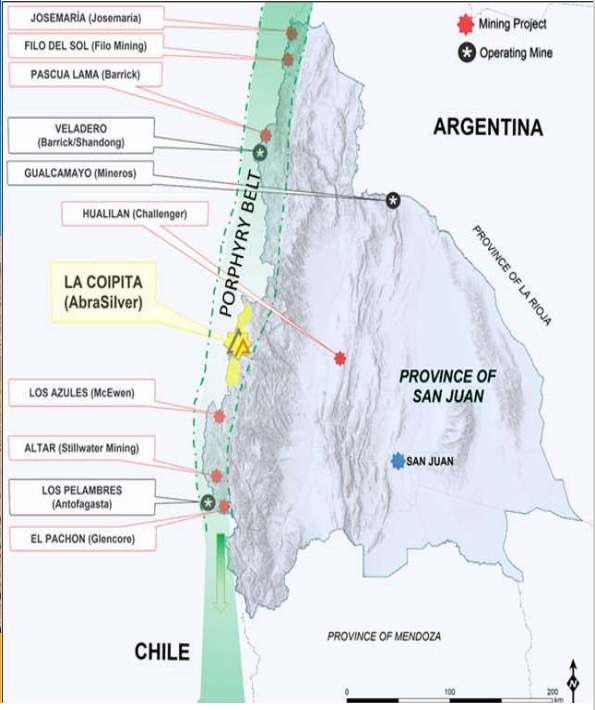

La Coipita in San Juan provides another great opportunity for ABRA.v

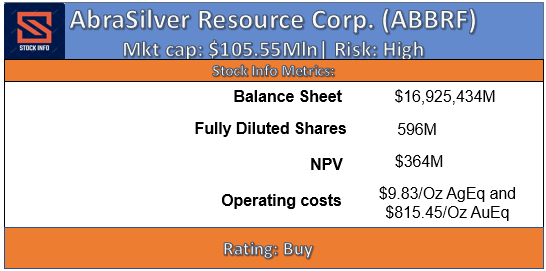

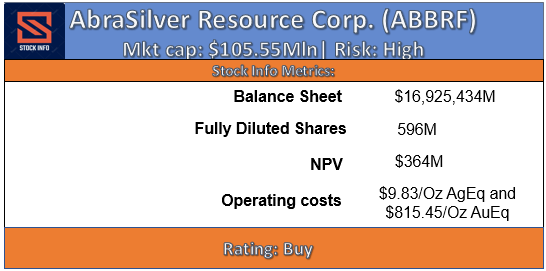

The Numbers

ABRA has a strong balance sheet, which will last them for at least 12 months.

Diablillos provides 90Moz+ of silver and around 1Moz of gold. Including some high-grade already measured ounces.

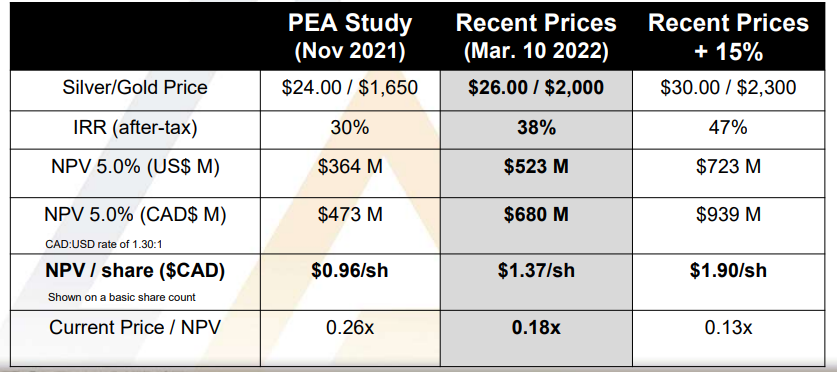

Excellent torque, ABRA’s NPV at a discount rate of 5% increases by C$75m with a $1 increase in silver.

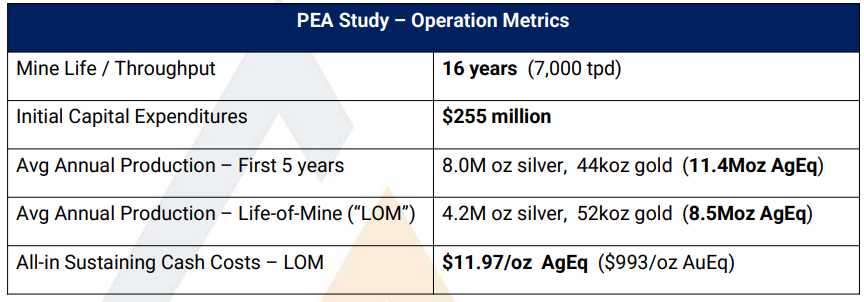

Diablillos has a solid mine life expectancy of 16 years with an excellent NPV

Operating costs per ounce are fairly low at $9.83/Oz AgEq and $815.45/Oz AuEq

La Coipita is an interesting project, which lays in San Juan close to projects like Filo del Sol and there are other majors in the region

La Coipita is a new Cu-Au Porphyry Discovery, which looks very promising

Economics are based on $24.00/oz Ag and $1,650/oz Au. These might seem fairly high currently, but if the bull cycle awakens again, we could see significantly higher prices. NPV is based on a 5% rate.

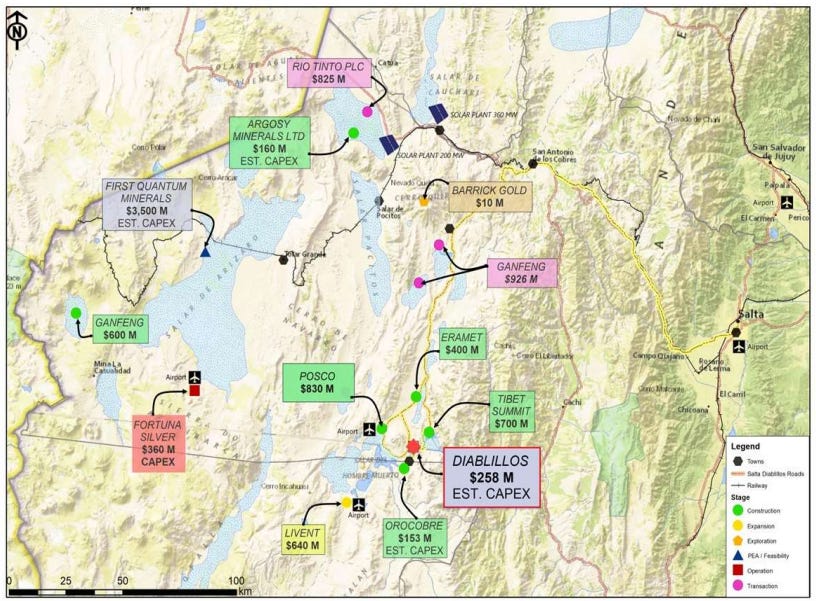

Diablillos

The Diablillos Project is located 160 kilometers southwest of Salta City along the border of Salta and Catamarca. Salta is the home of some of the largest mining companies in the world, including Barrick ( GOLD 0.00%↑ ), Rio Tinto ( RIO 0.00%↑), Fortuna Silver Mines ( FSM 0.00%↑) and much more. It is ranked #1 for investment attractiveness.

After a Preliminary Economic Assessment [PEA] was completed, the following results were found.

First of all, we would like to point out that we believe $ABRA.v is a world class project, which provides a lot of potential upside if silver starts moving higher again.

Average annual production in the first five years is expected to be around 11.4Moz AgEq. In addition, an average grade in the first five years of 175 g/t AgEq (130 g/t silver & 0.65 g/t gold) is expected. This shows the potential of this project. Furthermore, an average EBITDA in the first five years of $180M per year with a peak of $245M in year 2 can be expected.

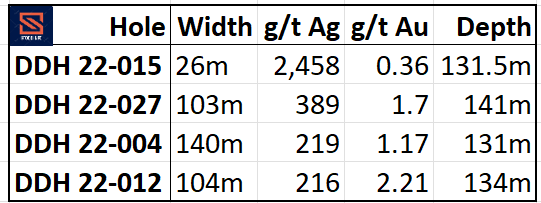

Due to the consistent high-grade results AbraSilver keeps pumping out they have a discovery cost of $0.13/oz silver-equivalent. All of Abra’s drilling holes are located near-surface in oxides. The following discoveries have been made.

Phase 2 of drilling will focus on adding more high value ounces. This will be done by following the next objectives:

Expand the shallow gold zone

Expand high-grade ‘measured’ resources in the Tesoro Zone

Expand resources beyond open pit margin in Northeast Zone

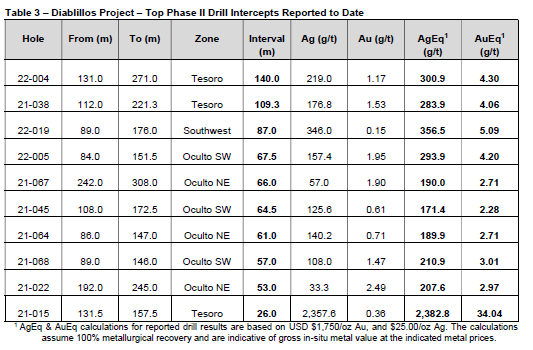

Above, you can see the most recent table provided by ABRA, this was released on the day we initially planned on releasing this article. The company came out with another excellent drilling result. This table clearly shows the significance of the current drill results, which shows the potential AbraSilver has. Note that this table talks about multiple zones like Tesoro, Oculto Southwest, Ocutlo Northeast, and the recent discovery in the new Southwest zone.

AbraSilver has multiple opportunities to further increase the potential upside.

Ongoing exploration, which is focused on expanding. This gives the possibility for some more high-grade intercepts.

Throughput expansion, ABRA is currently doing optimization studies to find the optimum throughput level. Furthermore, ABRA found through initial analysis a higher NAV and IRR can be achieved with a higher throughput.

Metallurgy, at the moment, test work is ongoing which is focused on improving the silver recoveries so this can be done in the most efficient way possible.

Strip ratio improvement, we believe further improvements are expected after the current drilling campaign is done. In addition, they are looking to reduce mining costs of shallow material, which at the moment of writing is unlikely to require blasting according to ABRA. Blasting is a chemical and physical process that occurs through the firing of explosives, it does break mineral-bearing materials. This is the reason most companies don’t like blasting.

Torque

If we take a look at the following table given by ABRA, we can just see how big this torque is. Keep in mind that this could become even better when taking new discoveries and improved grades into the calculation. This calculation only takes into consideration the current resource and does not include any value of the phase 2 drill results as these are not yet available. ABRA will release these and a new calculation as soon as they got them themselves.

As mentioned above, NPV (when using a discount rate of 5%) increases by C$75m for every change of US$1/oz Ag & US$100/oz Au.

Our conclusion on Diablillos

Diablillos clearly provides significant upside potential. This project is one of the lowest cost silver development projects in the world. Additionally, it is currently trading at a significant discount. Furthermore, Diablillos is one of the largest high grade oxide projects in a fairly safe jurisdiction.

We also like the fact that $ABRA seems to be focusing on increasing shareholder value. They give updates on their projects fairly often. In addition, they don’t do unnecessary dilutions, which other companies in this industry seem to do quite often. This shows that AbraSilver definitely isn’t a so called “lifestyle company” for the management.

La Coipita

La Coipita is an interesting copper project in San Juan, Argentina. The La Coipita project lays in a very interesting are close to companies like Filo del Sol ($FILO.v ) and other majors in the mining space like Barrick Gold ( GOLD 0.00%↑). ABRA has an option to acquire a 100% stake in this 70,000+ ha project in one of the hottest mining areas in the world. This Cu-Au belt is one with great potential, which has been proven by the recent succes of FILO.v.

In addition, ABRA has come out with some very promising assays from this project. Hole DDHC 22-002 intersected a continuous copper porphyry zone of 226m of 0.43% CuEq, which was a new discovery on the project. This project is very promising and further drilling will be done on this project. We aren’t going to much in depth here as this project is very well still in development. We would like to see some more assays here before making a conclusion. We do believe this project has a lot of potential and could be a game changer in the future.

Furthermore, we would like to address that the CEO himself says this project is of significant size and believes this could be a separate company on its own. This would mean that in the future a spin-off of this project is likely, which would benefit ABRA shareholders. On the other hand, there is also a possibility that this project remains under AbraSilver and that they will develop this further with a major player, which we believe wouldn’t be hard to find given the significant presence of majors in this area.

Management

First of all, we would like to state that the management of AbraSilver seems to be full of experienced people with a solid track record in the industry. President and CEO John Miniotis by example has 17+ years of experience in the industry including working for Barrick and Lundin Mining. Furthermore, he is a specialist in the M&A space and corporate finance. This is important as mergers and acquisitions are common in the mining industry.

In addition, we got David O’Connor, who is the chief geologist. Mr. O’Connor has 40+ years of experience in acquiring, exploring and developing mineral projects in South America. Furthermore, he has executive experience, which is something geologists often lack.

The rest of the management team consists of highly experienced people within the mining industry and in particular in Latin American jurisdictions. We believe this management should be capable to generate significant shareholder return in the future.

Shareholders and Share Structure

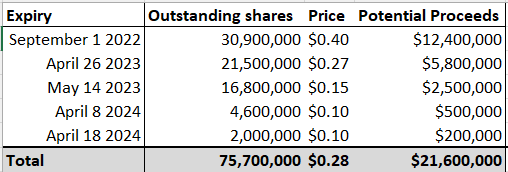

Let’s get straight to the numbers. At the moment of writing, ABRA has 495 million shares outstanding. In addition, there are currently 76 million warrants outstanding, with an average strike at $0.28 per share. Furthermore, there are 25 million options outstanding with an average exercise price at $0.20 per share. This gives an amount of 596 million fully diluted shares. As you can see in the table below.

The total options on the other hand consist of 25,200,000 outstanding at a strike price of $0.20, which would give Potential proceeds of $5,000,000. These options are exercisable until February 2027.

The management and the board of ABRA holds around 3%, but the outstanding options and warrants could increase this further. We would have preferred a higher stock position from the management and the board as this would provide more incentive to create significant value for shareholders, but management has proven that creating value is the number one objective for them. As such, we believe the small 3% stake isn’t an issue.

Furthermore, one of the biggest names in the mining industry owns quite a significant stake as well. Eric Sprott owns 13% of the company. Eric Sprott has a great track record and recently made headlines once again through his Uranium funds. URNM 0.00%↑ and $SRUUF

The Charts

As can be seen in the chart below, ABRA saw a significant rise in price recently. ABRA unjustifiably sold off due to weakness in silver price. In the meanwhile, ABRA continued to provide excellent drill results. In our opinion ABRA as a company significantly improved compared to the summer of last year when the share price was as high as $0.82 per share. Currently, ABRA is overbought based on the RSI. This is partially due to recent results and improving sentiment within the industry.

The chart below shows us a longer-term trend for ABRA. As can be seen below, the company has been in a downward trend ever since the ATH in 2021. We believe the company should be bottoming out fairly soon if it hasn’t already happened. The green trendline support is something we are watching currently. We believe the horizontal green trendlines are out of the question for ABRA. This seems only possible if the paper silver price goes down significantly further into the low to mid-teens. Even then we believe ABRA is position quite well, as it is one of the largest potential resources in the world. We believe ABRA could reach $1+ fairly soon if momentum and sentiment in the precious metal markets improves.

Conclusion

We believe AbraSilver is in a great position to profit from a potential commodities super cycle. In particular, the world class assets and the continuous reports of great assays gives us confidence in the project. La Coipita is a nice extra, which could give an additional boost to the share price if it fulfills its potential.

Unfortunately, rising energy prices and underperformance of Silver and Copper could put pressure on the stock price. We believe you shouldn’t invest in a junior mining company in the first place if you don’t believe in appreciation of the underlying value (in this case the precious metals). If you have read this far, you are probably a believer of a commodities super cycle. If this is the case, we believe ABRA is a stock to consider to add to your portfolio. Keep in mind that junior mining is a risky investment.

Thanks for reading this in the Spotlight! We hope you enjoyed it. Feel free to leave a comment below or contact us. Make sure to check out our twitter account by clicking HERE, that way you won’t miss out when we release a new article.

Disclosure: I/we have a stock, option or similar derivative position in the company mentioned.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. This article shouldn’t be seen as investment advice as I/we are no financial advisors. I/we have no business relationship with any company whose stock is mentioned in this article.

Thanks for reading Stock Info Letter! Subscribe for free to receive new posts and support my work.